)

)

)

Business philosophy6 Jul 2023

The Rise and Fall of Ivar Kreuger and Swedish Match

On November 7, 2022 it became clear that a subsidiary of the American tobacco giant Philip Morris would become the majority owner of Swedish Match.

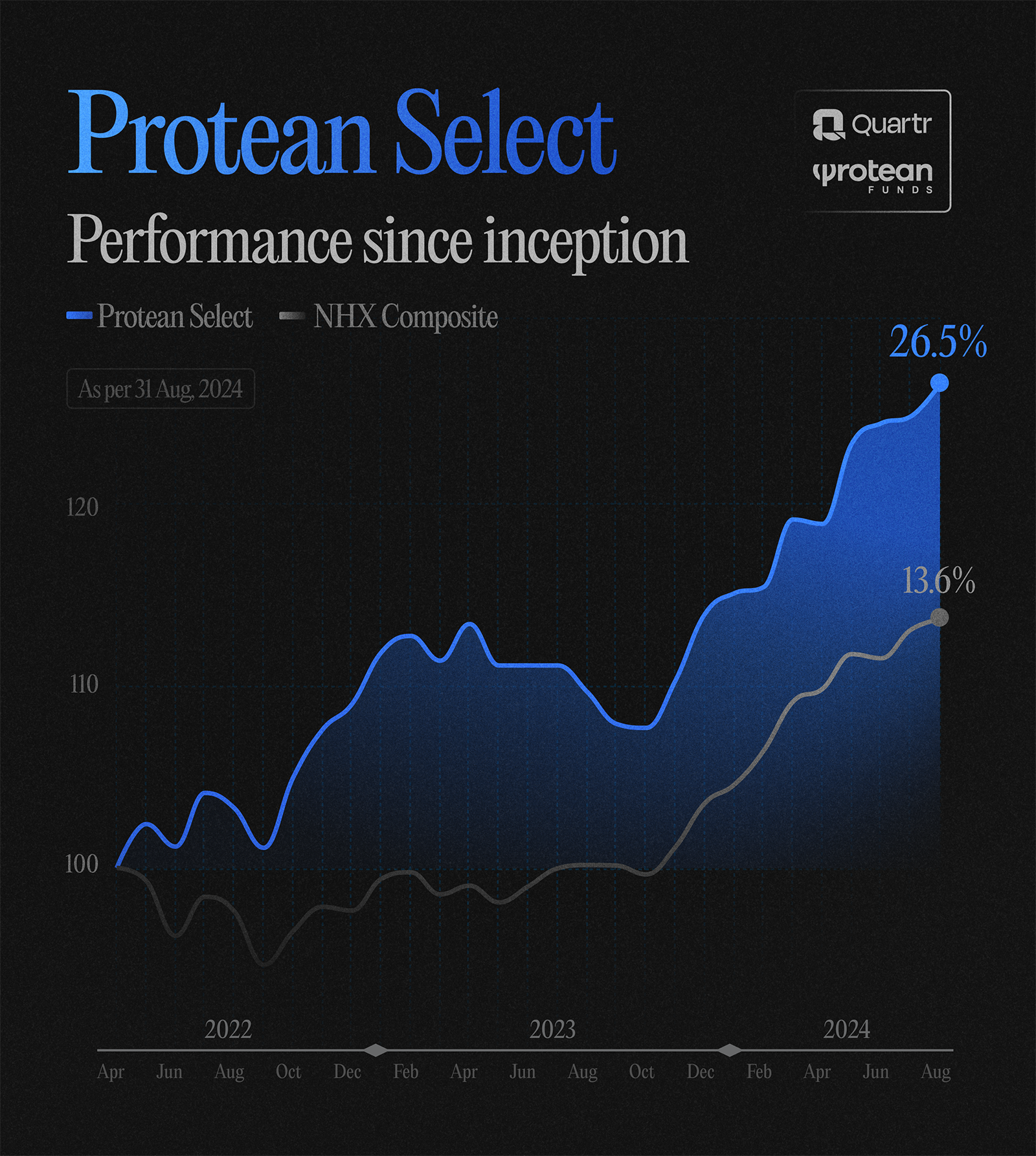

After a two-decade career in finance, Pontus Dackmo co-founded Protean Funds Scandinavia in 2022, where he now serves as CEO and Investment Manager. We had a chance to sit down with Pontus to discuss two of his current holdings, the most common misconceptions in the stock market, usual mistakes portfolio managers make, and his best tips for becoming a better investor.

I've always been a bit uncomfortable with this, but I guess the most important part is that I have an unhealthy interest in Nordic equities. Other than that, I'm just an average middle-aged guy with three kids, a dog, and a loving wife. I'm not a specialist in anything, really. If I had become a medical doctor – which was the plan for a while – I would have been a general practitioner. I have a double major in Economics and Political Science because I could never make up my mind about what was most interesting. I love buying books and have expanded the bookshelves at home a few more times than the family finds reasonable. Today, I am the CEO and Investment Manager at Protean Funds Scandinavia, a Nordic equity-focused investment firm.

I would love to say I started early, "mesmerized by stock quotes in the paper," but that would be a lie. I was far more interested in sports and politics (and girls). It wasn't until university that I caught the bug, thanks to the developing dot-com bubble. My tiny capital quadrupled in a year or two before promptly evaporating – a great learning experience!

While picking a subject for my Economics thesis, I stumbled upon the behavioral economics work of Kahneman and Tversky, and ended up testing their theories on actual stock market data. After that, I was pretty much hooked – but not from a pure economics perspective. I fell in love with crowd psychology, which has shaped my investment philosophy to this day. Behavioral inflection points and narrative changes are crucial triggers for share prices and are a key part of our idea generation process, combined with a more qualitative approach.

Get curated quality company deep dives every other week.

"Making money in the stock market is hard enough as it is – why make it even harder by introducing limitations that restrict how you can make money?"

Starting as a junior institutional sales representative in London in 2005, I had very little knowledge of financial analysis or the companies and industries we were analyzing and trading. I don't think I got the job because I was a great stock picker but because I had the makings of a decent salesperson. I could probably have just as easily sold washing machines. One of my few advantages is that I read quickly and have a knack for identifying what's important – a very handy skill as a stockbroker when you sometimes have to act quickly and deal with clients with limited attention spans.

If being an institutional salesperson to some of the largest and most qualified institutions in the world teaches you one thing, it's that there are more styles, investment philosophies, and opinions than you can shake a stick at. Serving as an advisor and broker to both long-term pension funds, deliberate risk-arbitrage funds, aggressive prop traders, and short-term hedge funds ingrains – apart from humility – that there are countless ways to invest. To be useful, you need to understand the rationale behind every investment firm and professional you serve.

This experience shaped my investment style in a meaningful way. I believe in being versatile, in not dismissing an opportunity just because it has the wrong label. Heck, the name of our investment firm, Protean, means just that: versatile. I understand why some funds focus on one thing, but it has always struck me as unnecessary to limit oneself. Making money in the stock market is hard enough as it is – why make it even harder by introducing limitations that restrict how you can make money?

To be frank, the driving force for starting the firm was that I was fed up with just being an adviser. I had been in the market long enough to have a decent idea of what works – or so I thought. I had also always invested alongside my work and had achieved a very respectable CAGR over 15 years, which gave me the financial security to strike out on my own. What began as a small family office in 2021 quickly evolved into a fund as several wealthy acquaintances and former clients expressed interest in investing with us.

I'm also a firm believer in the idea that the one who turns over the most stones will find more interesting ideas – and find them earlier – than everyone else. This is why we are so keen on data. We try to consume as much first-party data as possible. By that, I mean data directly from the companies, without going through the filter of research analysts who often interpret reports through their own (often biased) lens. We listen to many calls, read transcripts, and scroll through numerous slide decks.

I'm permanently surprised that so many people follow me. Most of what I tweet about are grumpy observations about strange things in the stock market – how can that be interesting to so many people?

Of course, there are several benefits, not least of which is that I can ask my followers anything and almost be guaranteed a handful of expert replies. I have direct message contact with several industry veterans across various fields who are incredibly helpful in assisting me in understanding their businesses. It's like having a private expert network of sorts.

Additionally, and this probably shouldn't be underestimated, it has helped with branding and asset raising for the firm. Having a broad following doesn't hurt either in the few instances where we've gone soft activist in a company, like our opposition to the bid for Swedish Match or our call for management change at the mining company Boliden.

My partner Carl Gustafsson and I have both worked with Nordic equities for about 20 years. We've known most companies, management teams, analysts, and investors in this region for quite some time. This is why we don't limit ourselves by sectors, styles, or sizes. Scandinavia is not the largest universe, and opportunities can arise from anywhere.

When someone presents a coherent and simple investment philosophy, I shake my head and see it as more of a marketing gimmick. No style works all the time. You can have decades when a style is out of fashion (just ask value investors!). Since an important feature of our funds is that we have skin in the game, investing 100% of our own savings, we believe in adapting when the market changes. That's why our philosophy is "be versatile."

That said, we believe there are several fundamental truths. Most money is made by owning small companies that grow into large ones. This requires holding smaller companies for a long (long) time, allowing for volatility. You cannot optimize these opportunities on a quarterly or even yearly basis. Another truth is that sizing is more important than timing. Being risk-averse, we run a very diversified portfolio and always consider liquidity and risk/reward. We also have a contrarian approach, believing that risk/reward is often best when something durable is out of fashion – but it must be timed relatively well.

A final important point is that we firmly believe being a small fund is almost a prerequisite for sustained outperformance. Funds often falter because they either become too convinced of their own brilliance and run an overly concentrated portfolio, or they grow too large and can't remain active without having an outsized market impact. To counter this, we cap both of our funds at a relatively small size.

"Drawdowns are kryptonite for CAGR, which is why we hate losing our investors' (and our own) money."

This is a difficult question since we are open to deploying almost any investment style. The common denominator is always risk/reward: what are the likely outcomes, and how much do we lose if we are wrong?

A reasonably strong opinion that things are improving for a large-cap stock that's been around for 50 years is sized differently than an ever-so-strong conviction in a loss-making 5-year-old small-cap that could potentially see accelerating growth in the next few years. Drawdowns are kryptonite for CAGR, which is why we hate losing our investors' (and our own) money.

We think a lot about edge. What is our edge in any given investment? Is it structural, such as running a small fund without unnecessary limits that enables more opportunities? Or informational – have we understood or discovered something others haven't? Or behavioral, exploiting time horizon arbitrage or others' biases?

We don't believe in easy answers because the game of stocks is hard. Someone likened it to playing 3-D chess, but with the rules constantly changing. I subscribe to that, and we often refer to our positions as "strong opinions, loosely held."

Sure, but keep in mind that "working day" is a bit of a misnomer since thinking about stocks and the portfolio doesn't follow regular working hours. It's a luxury to have a passion and hobby that looks a lot like work to others.

I usually get into the office before 8 a.m., and during the commute, I always listen to something – either a podcast or the latest earnings call from a company I've been curious about. I spend the first hour or two catching up on news and research, and I have a few morning calls with our brokers. Most likely, we place a few trades, trimming or adding to positions. Running a portfolio is much like steering a boat: you have to constantly make small adjustments to stay on course.

Much of the time in the office is spent digging around for ideas and incremental data points. You never know what might trigger you to dive down a new rabbit hole. If I find a promising lead, the next questions are always, "What research can I do? Who do I know that I can speak to about this?" I then arrange meetings to find out more. On average, we have one or two meetings per day, most often with listed companies but also with analysts and other experts. Preparing for these meetings takes up a significant amount of time.

One unique feature of our office is the "meditation couch." We call it that, but in reality, we take turns having a 20-minute nap in the afternoons... Breaks are important for processing all the information, whether it's a nap, a jog, or a walk with the office dog. In the evenings, I usually work out and then spend another couple of hours checking markets and news before falling asleep with a book. Many days are not "normal" though, be it reporting season, or the regular trips we make to meet with companies, or dinners and seminars. It's important to be out there, keeping a finger on the pulse.

Bloomberg is our main tool for market data, trading, and communication. It's ridiculously expensive, but I have to admit it's probably worth it. For information gathering and analysis, Quartr has simplified almost all my workflows. The mobile app is my go-to source for company calls and live transcripts, and Quartr Pro is a great tool for sifting through the full suite of corporate communications.

The search functions make it much easier to find inputs on themes or ideas we're working on. When I think about how I used to access company data, it's almost laughable how much Quartr has streamlined by collecting everything in one place and in real-time.

Oh, another great and difficult question! I think most asset managers underestimate the value of being versatile. We have a relatively large number of other portfolio managers who have invested in our funds. I believe they do so because we are small and adaptable. Protean is a stark contrast to large funds with various sector, geography, investment committee, size, or ESG limitations.

Many large fund companies simply do not optimize for returns; they optimize for asset gathering (which drives profit for the fund company). We're not like that. Since we have all our money in the funds ourselves, we're happy to run a break-even business and live off the returns we hopefully create in the funds.

The idea that stocks always go up over time. Yeah, sure, if you pick the right ones! There are many cases of investors clinging to a company that once performed well, hoping it will turn around. That's both the endowment effect and sunk-cost fallacy in a harmful combination. One of the hardest challenges in portfolio management is deciding when to sell a position you've held for a long time and know intimately, but that has started to go south.

Our main goal is to generate reasonable returns with reasonable risk, for an unreasonably long time. We believe there's a place in every allocator's portfolio for a versatile Nordic specialist fund with skin in the game and experience. Many just haven't realized it yet! There's something underappreciated happening here in Scandinavia: a vibrant stock market, numerous world-leading companies, and generally good governance.

If you look at historical returns, the Nordics are overrepresented in both league tables of 100-baggers and long-term broader market returns. Nordic equities deserve more international attention, and we're working to highlight that. Most of our assets already come from investors outside our home markets, so it seems we're onto something. But in the end, we're grateful to have the opportunity to do what we love with people we like. If we can continue to do just that, we'll be happy.

We run diversified portfolios, so the differences between the biggest and smallest positions aren't that significant. We generally say very little about our holdings, as we believe publicly committing to a strong view creates unnecessary mental baggage. But there are exceptions to this rule. For instance, we always try to mention a few holdings in our monthly Partner Letter.

Last month, we wrote about the Finnish renewable diesel refiner and distributor Neste. This is a medium-sized position for us that we initiated recently, noting that expectations are very low while the capital cycle appears to be turning in the right direction, and regulatory headwinds are shifting to tailwinds. A low valuation, combined with low expectations, a narrative change, and underlying all of that, a sound business with long-term growth potential, makes for an interesting prospect.

Another relatively sizable position for us is the Swedish medtech company RaySearch Laboratories, which specializes in oncology software, primarily for various radiation therapies. They have a superior product, thanks to over 20 years of significant investment, but they never really received recognition from the stock market due to a perceived lack of focus on profitability.

We sensed a change in the company's approach and worked to help nudge them in that direction, recognizing that a credible margin target paired with continued growth could be rocket fuel for the stock. It's up 170% since we invested, and we believe there is still ample upside potential. It’s become a sizable position for us organically.

Look, there are so many ways to approach the stock market. I believe you just have to get involved and figure out what works for you. I know people who hold five stocks with an average holding period of a decade, and others who trade 20 stocks in a day and never keep a position overnight – and everything in between.

You have to find an investment strategy that suits your temperament, and that can only be done through trial and error. Unfortunately, one of the key ingredients for improvement is time, and there are very few ways to speed up that process. My advice would be to make your mistakes early because they're usually less costly then.

"A Man for All Markets" by Ed Thorpe is a great book – very inspiring, and not just on a professional level. Ed is a great example of a first principles thinker, not trying to make things complicated because it makes you sound smarter. Rather the opposite. His journey shows how learning by doing, with plenty of skin in the game, can yield pretty amazing results over time. We're desperately trying to emulate that approach at Protean.

"Behavioural Investing" by James Montier is another excellent book, exploring the intersection of psychology, institutional constraints, and economics. It’s not just a book but a companion and encyclopedia of the various effects and phenomena that all investors struggle with. Plus, Montier is a great and entertaining writer.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)

)