)

)

)

)

Business philosophy14 May 2024

The Brunello Cucinelli Story: Combining Elegance and Ethics

Explore the success of Brunello Cucinelli's unique blend of luxury craftsmanship and ethical business.

Moncler was born from the practical demands of work and everyday life in the French Alps. Founded to supply utilitarian clothing for those working in sub-zero temperatures at altitude, it has evolved into one of the most recognizable luxury brands in the world. Our story will take us from a small Alpine village outside Grenoble to some of the most prestigious runways in the world. Today, you are far more likely to see its iconic puffer jackets on the outdoor seating at a cafe in Paris or Milan than to meet an alpine worker with a Moncler Badge on their left arm. This is the story of the rise, fall, and resurgence of Moncler and how the brand's explosion onto the luxury scene was all orchestrated by one man: Remo Ruffini.

Moncler's story starts in 1952 in Monestier-de-Clermont, a picturesque mountain village nestled in a valley and surrounded by alps near Grenoble in southeastern France. Founded by René Ramillon and André Vincent, Moncler was established not as a fashion label but as a supplier of clothing and equipment with which people would entrust their lives.

Ramillon was an entrepreneur with a background in manufacturing mountaineering equipment. Before Moncler, he had already built a reputation through his company, which specialized in technical gear for outdoor use. Vincent, his business partner, contributed marketing and strategic knowledge, something that would prove to come in handy sooner rather than later.

In the beginning, the young company manufactured quilted sleeping bags, camping tents with external covering, and padded garments intended for workers exposed to the elements in the mountains surrounding Monestier-de-Clermont. The name of Ramillon and Vincent's company is, as you may already have deduced, a portmanteau of the town's name. While the Moncler of today hosts massive fashion shows in the world's most exclusive ski resorts, the focus in the early days was strictly on function over form.

Their initial product line focused on practicality and was strictly utilitarian. The products were not luxury goods, nor were they widely marketed. Instead, they were designed to serve a specific and limited audience of alpinists, mountain workers, and outdoorsmen - and to do it extremely well.

When you're conducting maintenance on critical infrastructure halfway up the mountain and it starts to snow, you care very little for the look of what you're wearing. What matters is that you're warm and that the clothing allows you to continue your work while staving off hypothermia.

The puffer jackets Moncler would later become famous for were, in fact, a byproduct of the company's need to protect its own workers. To shield the laborers assembling tents in the company's small mountain factory in sub-zero conditions, the founders developed padded jackets made from nylon and stuffed with down. These were simple, robust garments and were not intended for public sale, but rather to ensure that the products they did sell could be manufactured without the company's workers freezing to death.

The first jackets that Moncler provided to its workers had been manufactured using the same technique and, more importantly, material as their sleeping bags and tents: goose down. It was lightweight, compressible, and provided excellent insulation and warmth. The jackets made for the employees in the factory worked so well that it wasn't long before their utility caught the attention of serious mountaineers. Word quickly spread about Moncler's jackets, and soon the brand found itself being approached by climbers.

One of the most consequential figures in Moncler's early history was Lionel Terray, a French mountaineer whose role in shaping the brand's technical capabilities cannot be overstated. Terray was a highly respected figure in the climbing world by the early 1950s, having taken part in several challenging expeditions, including first ascents in the Andes and the Alps. All in all, Terray was what can only be described as a rockstar in the mountaineering community.

Needless to say, this meant that Ramillion and Vincent were more than happy to work with him, and perhaps as proof that they were on to something big, Terray came to them first. The collaboration between one of the most famous mountaineers of his time and a small manufacturer from Monestier-de-Clermont began not as a sponsorship or endorsement but with practical problem-solving. Terray needed the best possible equipment, and he saw the massive potential in the padded jackets Moncler was producing for its workers.

Together, they began to refine Moncler's jacket design – modifying stitching patterns to reduce cold spots, adjusting insulation distribution, and incorporating wind-resistant materials. Terrey proved to be the perfect advisor, as he had first-hand experience of what truly mattered in some of the most hostile environments on earth.

He would wear the jacket for an expedition, come back, and tell the pair what worked well and what could be improved. In many ways, Terray's involvement nudged Moncler away from being a gear manufacturer toward becoming a technical outfitter for elite mountaineers.

In 1954, Moncler introduced the Karako, its first true down jacket for commercial use. The Karako marked a shift in Moncler's product identity and propelled the company into a new phase. It featured a thick layer of down insulation, a high neck for added protection, and a robust exterior shell.

Despite the pivot and the release of the Karako, Moncler was still a small operation during the early years. Its reputation spread largely through word of mouth within the tight-knit climbing and ski communities of Europe. The brand didn't aim to expand internationally and definitely had no intentions toward high fashion. It was grounded in the feedback loops between the company's technical team and the professional users of its jackets, with the main focus being to provide the best possible products.

The most important part of Moncler's early development work was its iterative design process, a continuation of the philosophy that started through the work with Terrey. While some brands would release seasonal collections, Moncler treated each garment as a work in progress.

With every new expedition or field use, jackets were returned to the workshop with notes about zippers that froze at altitude, seams that let in snow, and linings that didn't dry quickly enough. These feedback rounds led to subtle but important design changes, resulting in a product that continually improved.

On a short side note, letting the professionals try out products and improving them using their feedback is still something employed by many manufacturers of outdoor apparel. One example of this is the professional climber Alex Honnold (famous for climbing up El Capitan in Yosemite without a rope), who works with The North Face (owned by VF Corporation).

He and other professional climbers and explorers receive prototypes of new products and test them out in harsh conditions before they're released to the public. As he put it himself: “If [the gear] survived Antarctica, it's probably good enough for Brooklyn”.

Moncler's base in the Rhône-Alpes region offered unique advantages, and the proximity to the Alps meant easy access to real-world testing grounds. The brand's workshop practically nestled into the mountains, and its founders maintained close ties with guides, rescue teams, and ski instructors, who all provided feedback on the early products.

The growing interest in Alpinism in post-war France and the rest of Europe also played a role, as the 1950s was a period of renewed national interest in the outdoors. While Moncler was still positioned at the technical end of the market, the growing visibility of winter sports began to lift interest in alpine gear across the board. Moncler, by virtue of its origin and reputation, found itself well-placed to ride this slow but steady wave.

By the early 1950s, humans had been to nearly all corners of the earth. We had set foot on both poles, and the blank spots on the world map were as good as gone. However, one thing remained for explorers looking for their shot at glory: the tallest mountains on our planet.

In 1954, Moncler would become involved in one of the biggest events in the history of mountaineering: the first successful ascent of K2. Though slightly lower than Everest, K2 is far more technically demanding and even more dangerous.

Its sheer faces, unpredictable weather, remoteness, and inherent danger had thwarted all previous attempts. In 1954, a year after the conquest of Everest, a team of Italian climbers was going to make a push for the summit – and Moncler would supply the jackets.

The Italian team arrived in Karakoram in the spring of 1954, traveling by train, truck, and mule caravan to the base of K2. Unlike some modern expeditions, which rely heavily on helicopter drops and commercial logistics, the first ascent of K2 was almost entirely manual. Supplies, including Moncler jackets, were carried up in cycles by the climbers themselves, but more importantly, roughly 500 Pakistani porters.

Despite what Moncler's current-day marketing might lead you to believe (unsurprisingly, the company still uses the expedition heavily in its heritage-based marketing), its jackets were not used for the final summit push. At that point, climbers wore specialized high-altitude suits made from layered materials designed specifically for oxygen-deprived environments.

Moncler was asked to provide down jackets that would serve as key insulating layers during acclimatization and at base camp, where temperatures could plummet and storms appear at a moment's notice.

The team spent weeks navigating the Abruzzi Spur, K2's southeast ridge, in unpredictable and brutal weather. High winds, deep snow, and the constant threat of avalanches forced endless delays and shifts in approach. But on July 31, 1954, two climbers – Achille Compagnoni and Lino Lacedelli – reached the summit of K2, planting the Italian flag at the peak.

It was a monumental achievement. Conquering K2 and coming back down alive to tell the tale was nothing short of a superhuman feat. For Moncler, the publicity surrounding the expedition offered invaluable exposure. The brand's jackets were seen on climbers in press photos and later in publications and documentaries. For a company still grounded in the technical niche, this visibility offered a bridge to broader markets.

Moncler did not immediately pivot toward lifestyle or fashion, but the success proved that its jackets could perform in the most hostile environments on Earth. In marketing materials from the late 1950s up to the present day, Moncler (rightfully so) proudly references the K2 expedition and the role it played in it.

Get curated quality company deep dives every other week.

We're soon going to introduce the main character of our story and the reason for Moncler's turnaround and pivot into luxury. While we have discussed the brand's origins and heritage, we need to provide context to what happened next with Moncler. Understanding how the brand nearly tumbled into the abyss of irrelevancy is important to understand the scale of transformation that would eventually follow under Remo Ruffini.

Throughout the 1950s and 1960s, Moncler jackets remained utilitarian. Distribution was regional, and the brand continued to operate towards a consumer group where performance was the key selling point. Yet, a slow shift was underway. Europe continued to recover from WW2, and the economic outlook continued to improve. Moncler would start to pivot due to two separate, intertwined factors: the growing popularity of skiing as a leisure activity and the expanding middle class in Western Europe.

By the late 1960s and into the 1970s, skiing had begun to attract people seeking winter holidays in the Alps. Ski resorts expanded across France, Switzerland, and Italy, and with them came new consumer demand for cold-weather apparel that was functional without completely disregarding aesthetics. Sure, staying warm and dry on the slopes was important, but consumers, surprisingly enough, didn't want to run into their colleagues or neighbors while looking like an Alpine factory worker.

Moncler, with its technical know-how, found itself in a prime position to capitalize. It began producing ski jackets designed not just for explorers and those who regularly risked their lives in the mountains but also for recreational hobbyists. This pivot was the first, somewhat stumbling, step of Moncler's long walk towards lifestyle fashion. The company proved to be able to combine form and function without needing to compromise too much on either.

In 1968, the brand was chosen to be the official supplier for the French alpine ski team at the Winter Olympic Games in Grenoble – practically in Moncler's backyard. The jackets worn by the team featured the colors of the French tricolor with slim, sporty silhouettes and brought Moncler exposure to a much wider audience.

Unlike the K2 expedition, which had captured attention in the mountaineering community, the Olympics broadcasted a different, more prestigious image of Moncler. Yes, the K2 expedition doesn't hurt, but for the average skier, it's a bit more appealing to look like an Olympian than someone ascending a mountain with ice picks in hand.

As a result, Moncler jackets began to appear not just on the slopes and in gondolas but also at the après-skis. They were sold in exclusive resort boutiques, worn in ski towns, and gradually acquired a reputation for being chic as well as functional. At the same time, as its reputation was shifting, Moncler set its sights on expanding distribution, particularly in Western Europe.

The 1980s marked Moncler's first true golden era as a commercial brand. With winter holidays becoming more common among the middle and upper classes, demand surged for ski apparel that worked both on the slopes and at the champagne tables. Moncler jackets fit the bill perfectly and became common in ski resorts like Courchevel, Chamonix, and Zermatt.

By the 80s, Moncler had moved decisively into the consumer market. The why is relatively self-explanatory: the total addressable market is much larger. Someone purchasing one of Moncler's expedition jackets might buy it once and keep it for as long as possible. However, someone buying the latest puffer to look good at the Aprés in Val Thorens is far more likely to be a repeat customer to keep up with the latest trends.

The jackets in the 1980s were produced in a wide variety of sizes and styles, but most importantly, colors. While some technical features remained – like the ever-present down insulation and windproof shells – many of the jackets were now designed with aesthetics taking center stage. Bright colors, glossy finishes, and branding elements began to appear more prominently and became a hallmark for the brand. Some 30 years after its founding, function took a backseat to form, and in some cities, most famously among youth in Milan, it had become part of everyday outfits.

Despite commercial success, the 1980s also marked the beginning of internal challenges. Moncler changed hands multiple times over the next two decades, and with each transition came a different strategic vision. All different management had different visions for the brands, and the frequent shift in ownership resulted in inconsistent product direction and diluted brand identity.

One of the key challenges Moncler faced was maintaining a clear identity amid rapid expansion. It was no longer purely a technical brand, but neither was it fully a fashion label. The technical performance of the jackets wasn't strong enough for professional users, and while its jackets were expensive, they weren't fully embracing the luxury strategy. In short, Moncler was drifting in between categories.

To add to the headaches, Moncler was competing in a market that was getting more and more crowded. In the 1990s, the outdoor apparel market was diversifying and expanding rapidly. The space was getting more and more crowded every year, with brands like The North Face, Patagonia, and Columbia offering technical jackets with updated, modern materials and advanced waterproofing technologies. These companies invested heavily in R&D, marketing, and innovation, while Moncler remained anchored in the aesthetics and materials of a previous era.

The rise of synthetic insulation – lighter, quicker to dry, and more often than not at a lower cost, often cheaper than down – also challenged Moncler's position. While the company had built its identity around goose down, it struggled to compete with brands embracing synthetic alternatives that offered similar warmth with better weather resistance at much cheaper prices.

By the 1990s, Moncler's identity had become increasingly fragmented. In some markets, it was still associated with ski culture and luxury outdoor gear. In others, it had begun to lose ground to more technical or trendier brands. The jackets, once iconic, were starting to be viewed as dated.

This period also saw a decline in quality control and consistency. Under new ownership, Moncler expanded its product lines, introducing items beyond outerwear. However, many of these ventures lacked cohesion and diluted the core brand values. Efforts to chase trends often led to confusion, as the brand shifted between heritage, fashion, and sport, and failed to deliver in all three areas. In short: a jack of all trades but a master of none.

Sales slowed. In several European markets, Moncler lost shelf space to younger, more dynamic brands. Retailers hesitated to stock products that felt out of touch with consumer expectations. Among younger buyers, Moncler was no longer a brand they wanted to associate with – it was something their parents had worn on ski trips in the 1980s.

The brand's position – not fully technical and no longer fashionable – left it vulnerable. To stay afloat, Moncler pursued a series of licensing agreements in the 1990s. These allowed third parties to produce clothing and accessories under the Moncler name, often with limited oversight. While these deals brought in much-needed revenue, they further fragmented the brand as products varied widely in quality, design, and positioning.

The jackets were still recognizable and came with remnants of a once-positive reputation, but the company behind them had lost its direction. By the early 2000s, Moncler had become, in many ways, a legacy brand – alive but unremarkable.

By the turn of the millennium, Moncler was at risk of becoming a thing of the past. It had heritage, but no clear future. The company lacked the innovation to compete with technical brands and the creativity to challenge high fashion labels. Its products were seen as expensive but outdated, functional but uninspired, and the financial situation can only be described as, at best, strained.

Yet, the foundation of something great still existed. The brand had a story – one rooted in mountains, expeditions, and survival. It had iconic silhouettes and a distinctive aesthetic that had once captivated consumers. What Moncler lacked was someone to bring coherence, energy, and vision to its scattered parts. Enter: Remo Ruffini.

Remo Ruffini was no stranger to the world of design and business. Born in Como, a traditional textile town, in 1961, he came from a family with experience in fashion. His grandfather ran a textile mill, while both of his parents ran their own clothing brands. Ruffini had studied in the United States, where he had also worked for his father, and had previously founded New England, a casualwear brand he eventually sold. By the early 2000s, he was looking for his next project.

Ruffini entered the picture initially as a consultant in 2000, brought in to advise on repositioning the brand. It quickly became clear to him that Moncler had unrealized potential – not because of its current business, but because of its dormant narrative. The K2 expedition, the Olympic heritage, and the original down jackets were not just history – they were assets waiting to be rediscovered, recontextualized, and exploited.

In 2003, Ruffini acquired the company outright, taking full control and assuming the role of Chairman and CEO. From the beginning, he viewed this not as a rescue operation but as a rebuild of a great brand that had lost its way.

Ruffini's first steps were decisive. He immediately set out to simplify and centralize the brand. One of the first changes came in the form of canceling nearly all of Moncler's licensing agreements. At the time, the brand had licenses across various product categories and geographic markets. These arrangements generated some revenue but eroded the consistency and control Ruffini believed were necessary to reposition Moncler at the high end of the market.

This move came with short-term financial risk as it meant less immediate cash flow and fewer retail partners – but Ruffini was playing a long game. His goal was not to sustain Moncler's presence in fragmented markets and to keep the company afloat – it was to redefine what the brand was and who it was for.

One of the first things he did was to relocate the company's headquarters to Milan, the heart of Italy's fashion industry. Although the brand will always be associated with France, Ruffini believed Milan offered the creative infrastructure and global access that the brand needed to scale.

With licensing contracts terminated, Ruffini brought product development, design, and manufacturing back under central control. He believed that Moncler needed to have a single voice – one aesthetic and one narrative. From now on, every jacket, every store, every campaign would be part of a cohesive vision.

One of Ruffini's core ideas was deceptively simple: elevate the down jacket from utilitarian gear to a luxury item. This wasn't about adding logos or changing fabric colors – it was about redefining the cultural meaning of the jacket itself. As you might understand, not as straightforward as it sounds.

He worked closely with designers to refine the silhouette of the classic Moncler coat. The puffiness was streamlined, materials were upgraded, and small but deliberate details – chrome zippers, fine lining, embossed branding – were introduced. The jackets were still recognizable as Moncler, but they felt more modern, more tailored, and more intentional.

Instead of butting heads with technical brands like The North Face or Patagonia, which were well-established and incredibly tough to compete against, Ruffini positioned Moncler in the luxury apparel segment at a price point far above the aforementioned brands. This meant pricing jackets in similar price tiers to brands like Prada and Louis Vuitton, not sportswear companies.

It also meant reimagining where and how Moncler would be sold. Ruffini understood that luxury was not just about price and quality – it was about selling an experience and a feeling. One of the most critical elements of his strategy was a dramatic tightening of Moncler's distribution.

Previously, the brand's products were available through a wide array of third-party retailers, including ski shops, department stores, and sportswear chains. While these retail channels are effective for mass market brands, it doesn't exactly reek of exclusivity.

Therefore, Ruffini reversed course. He began withdrawing Moncler products from stores that didn't align with his vision (which was more or less all of them). He focused instead on high-end department stores and boutiques, negotiating better placement and tighter control over presentation. He also initiated the process of opening Moncler's own branded stores in key locations across the globe.

These stores weren't just places to buy jackets. They were built and designed in the same spirit as more traditional luxury brands with subdued lighting, strong branding, and a sense of exclusivity. The goal was to create an experience that helped to justify the price while reinforcing Moncler's new identity.

Ruffini was acutely aware that heritage alone was not enough. Having a captivating history is one thing, and Moncler had plenty to go around, but the crux was turning that history into a compelling narrative. The direction he chose was, unsurprisingly, to lean into Moncler's alpine past as a platform for storytelling. It sounds simple enough, but it needs to be executed well to work.

He reframed Moncler's origin story – mountain village roots, outfitting for extreme conditions, the K2 expedition – as a kind of brand myth. This narrative became central to everything: product names, in-store visuals, advertising campaigns.

The brand's logo was given a more central role in design, and the jackets were given names that harkened back to mountains and exploration – Himalaya, Everest, and Karakorum. In this way, each piece of clothing became part of a broader narrative arc and helped to build the modern image of Moncler. Consumers weren't just buying a high-quality coat – they were buying into a story of survival, resilience, and sophistication.

As we went over previously, Moncler had strayed away from function, sacrificing it to focus on form, falling short in both categories. For the entire pivot and rebuild of the brand's image to work, aesthetics had to be balanced with high performance.

He introduced seasonal collections that kept pace with fashion calendars and followed the traditional strategy of fall/winter drops, new colorways, and capsule collections. At the same time, he ensured that each product maintained technical credibility. The jackets were still filled with high-quality down, still constructed with wind and water-resistant materials, and made so that they would perform the most basic function of a jacket (keeping the wearer warm) very well.

Ruffini's strategy for the rebuild can be summarized in several interlocking components:

Control: Cancel licensing, centralize design, and oversee production.

Focus: Concentrate on a single iconic product – the down jacket.

Elevation: Position Moncler in the luxury space, not the sportswear sector.

Narrative: Leverage the brand's history for modern storytelling.

Visibility: Invest in PR, celebrity placements, and curated retail experiences.

Balance: Maintain technical performance even as the brand embraces aesthetics.

All in all, it was a systemic change. Every layer of the business was rethought, every detail scrutinized, and the brand wasn't re-invented completely, but it was salvaged and elevated far above what it had ever been before.

We're going to get more into both the company and the brand as a whole in a moment, but when looking at the Moncler of today, it's apparent that the core strategy hasn't changed much from the rebuild plan. Ruffini had a vision, executed it extremely well, and Moncler is now in the extremely enviable position to continue to capitalize on the foundation that was laid during this period.

By 2013, Moncler was no longer simply a functional skiwear maker. Under Ruffini's direction, the company embraced a unique mix of heritage, performance, and high fashion. It began collaborating with designers, expanding into year-round collections, and curating a tightly controlled retail footprint in key global cities. The strategy had started to pay off: revenues were growing rapidly, margins were healthy, and brand equity had never been higher.

At this point, the luxury sector as a whole was undergoing a post-recession resurgence as a whole (LVMH and Kering stocks had both returned 4-5x since lows in 2009). In December that year, MONCLER was listed on the Milan Stock Exchange in an IPO that was packed with action. Approximately 28% of the company's shares were made available to the public, and the interest from investors was sky-high.

The IPO was oversubscribed 31-fold, with institutional investors alone placing orders for over €20 billion. When the bell rang on the trading floor in Milan, Moncler had a market cap of 2.55 billion. When the markets closed later that day, it had risen by 40%.

The IPO had, like many other things for Moncler over the previous 10 years, been a massive success. Moncler had arrived on the luxury market in earnest, and it had no plans of slowing down. But don't just take our word for it. This visual highlights the spectacular growth that the company has had following its IPO:

But this is yet another opportunity to sing Ruffini's praises, and to highlight just how remarkable the turnaround was. When he acquired Moncler in 2003, its revenue was roughly €55 million. That number had grown to €3.1 billion by 2024. A remarkable 22.6% CAGR over 21 years.

After Moncler's IPO in December 2013, the brand continued to step on the gas. Remo Ruffini approached this new phase with the same blend of pragmatism and vision that had guided Moncler's revival a decade earlier. Having successfully repositioned the brand as a luxury name without severing its ties to performance wear, Ruffini now turned to scaling that vision globally without compromising what made Moncler distinctive in the first place.

The years after the IPO were marked by methodical expansion. Moncler didn't rush into every market or open stores at breakneck speed. Instead, the company opted for a more considered, direct-to-consumer strategy. This meant focusing on flagship locations in key cities – places where the brand could control the full customer experience from entry to purchase and where the surroundings matched the luxury feel of the product.

But brand strategy wasn't only about where to sell; it was also about what to sell and how to evolve. In 2018, it launched what would become a defining concept for the brand going forward: Moncler Genius. This initiative was based on the idea of frequent collaboration – not just with a single creative director, but with multiple designers, each invited to reinterpret the Moncler identity in their own way.

Genius was more than just a marketing experiment; it was a structural shift in how the brand approached product development and seasonal fashion cycles. Instead of relying on the traditional rhythm of fall/winter and spring/summer shows, Moncler started releasing Genius drops throughout the year. This has allowed the brand to stay in the conversation more consistently and connect with consumers used to the fast pace of digital culture.

We're now entering the modern-day era of the Moncler Group, and there is plenty to uncover in order to understand the company as a whole. As you may have noticed, we, for the first time, referred to the Moncler Group. This is because Ruffini just brought another brand into the fold.

In December 2020, Moncler announced its acquisition of the Italian brand Stone Island for €1.15 billion. While the move was somewhat unexpected, it made a lot of strategic sense. Stone Island, with deep roots in technical apparel, had built a strong and incredibly loyal following over the decades, particularly among younger male consumers.

Initially popular amongst streetwear enthusiasts in Milan and English football fans, the brand has since spread across the continent and reached what in many circles can only be described as cult-status.

Where Moncler is focused on the language of luxury and heritage, Stone Island shares some similarities but with a whole different approach to fashion. As a stark counterpoint to Moncler, Stone Island is a brand that constantly re-invents itself and its clothes, always looking for new ways to utilize fabrics and colors while keeping the iconic patch featuring a compass logo as a common theme throughout its designs.

The deal was structured to preserve Stone Island's creative and operational independence, something that is central to its DNA. Ruffini described the move as a way to continue to expand into “New Luxury.” Make note of this expression “New Luxury”, as we'll expand on the subject in just a minute.

Even when talking about a different luxury company, it's impossible not to mention the largest luxury conglomorate in the world: LVMH. Bernard Arnault and his luxury conglomerate are always looking to increase their reach within the sector, and in September 2024, they made an indirect investment in the Moncler Group. LVMH acquired a 10% stake in Double R, the holding company controlled by Remo Ruffini. Double R currently holds around 16.9 % of Moncler's shares, which in turn means that LVMH's indirect exposure to Moncler is about 1.7%.

Interestingly enough, a partnership agreement has also been signed, which allows Double R to increase its stake in Moncler by 18.5% over the following 18 months, with funding from LVMH. LVMH has also been given the opportunity to purchase more shares in Double R, up to 22%. However, under the framework of this partnership, should both parties choose to increase their stakes, the indirect investment in Moncler for LVMH would still be less than 5%.

As part of the agreement between the two, Alexandre Arnault, the middle child of 5, is set to join the board at Moncler. However, it's important to keep in mind that this (so far) is not an attempt at a takeover. Instead, the two companies are looking to cooperate and find synergies that they can exploit. However, if Ruffini ever decides to sell his shares, LVMH is in pole position to increase its ownership.

We've now arrived at the present day, and with that, it's time to go over the numbers and the most important geographies for the group. Before, it's important to have an understanding of how the company operates on the business side of things and its position in the wider luxury sector. First things first: Moncler has a market cap of roughly €14.6 billion, making it the 7th largest luxury company in the world.

As per the FY2024 report, group revenues were slightly above €3.1 billion with, as Ruffini called it, “a resilient EBIT margin” of 29.5%. He's not overstating things – over the last 4 years, the company has maintained an EBIT margin of over 28%. When compared to other luxury companies, this is incredibly strong. In 2024 Richemont and LVMH both posted EBIT-margins at roughly 23%, with Kering and Brunello Cucinelli reported 16.5% and 14.8% respectively.

DTC channels for both Moncler and Stone Island posted double-digit growth. But we're going to zoom in on the retail channels as they are a key part of the company's strategy.

2024 marked the opening of 14 new "mono-brand" stores by Moncler, which, as made clear by the name, are retail locations that only sell one particular brand. Since 2020, the number of these stores has increased by 60 new openings, and Moncler today operates 286 retail locations. While this might not sound like much when compared to a company like AutoZone, it's important to remember that these are luxury channels, with all that entails. Stone Island? After the acquisition, the number of stores has increased from 30 to 90 in just four years.

As for the brand split? Moncler stood for 87% of revenues, with Stone Island accounting for the rest. We've visualized this below, with the inclusion of the geographical split:

When taking a look at the largest luxury companies in the world, almost all of them have Asia as their biggest market, with Europe coming in second place. This is, in other words, not something which is unique to Moncler. Asia is the biggest luxury market in the world, and more importantly, the one with the largest potential for growth.

However, when taking a look at the full report, one spots something very interesting: Stone Island does not have its biggest market in Asia. In 2024, 67% of its revenues were generated from EMEA, with only 26% coming from Asia. This was up 4% from 2023, and given the importance of the market and that the group is placing a lot of emphasis on growth in the region, revenue from Asia is expected to continue to increase.

Today, Moncler is no longer just a single brand – it's a group, and one with a clear sense of purpose. The company has managed to scale while retaining its essence and exploiting what makes it special. When you compare it to the Moncler of the 1950s, some common denominators remain, but it is more or less unrecognizable. However, with Ruffini at the helm, it has been incredibly skilled at highlighting its heritage while evolving to remain relevant and modern.

It would be incorrect to describe the company primarily as a skiing outfitter. In pretty much every sense of the word, the Moncler of today is a fashion brand. This is not something that Moncler tries to hide from by creating ads only showing people in skilifts, and they are acutely aware that it’s far more likely to be worn in a city than on the slopes.

A motto often found throughout marketing material and other communication is “Born in the mountains, but living in the city”. The Moncler of today aims to target those living in urban environments and is constantly visible at some of the most prestigious runways and fashion shows in the world. But the company still utilizes its heritage in creative ways. Instead of hosting big fashion shows and events in its operational hometown of Milan, it instead opts to hold the reveals of new collections in prestigious ski towns.

But the products have also evolved, and the portfolio has expanded dramatically. Moncler is still best known for its puffers, of which it sells a wide array of different models. But in order to stay relevant and ensure that consumers can dress themselves in Moncler even during warmer months, its product catalog now also includes everything from t-shirts and sweatshirts to jeans.

You might remember that one of the first courses of action that Ruffini took when acquiring Moncler was to end all licensing agreements. Now, over 20 years later, the company has slowly but surely started to dip its toes back into licensing its IP to other manufacturers. Most notably, EssilorLuxotica today produces branded sunglasses on license, and Interparfums sells Moncler-branded perfumes for both men and women.

All in all, both brands under the Moncler Group have a relatively diverse portfolio of products, but one of its main strengths is in its brands. Both Moncler and Stone Island are incredibly recognizable and carry with them a sense of exclusivity and prestige. This, in turn, also translates into pricing power.

Yes, the clothes are of high quality, but if you want to wear the badge, either the Moncler M or the Stone Island compass, you have to be ready to pay the premium to do so. This is oftentimes referred to as brand equity, of which both Moncler and Stone Island have no shortage. Both have a very high flexibility in how they price their products, much in part due to the strength of their individual brands.

In contrast to some acquisitions in the luxury sector, the acquisition of Stone Island was not meant as a consolidating move. While some similarities can be drawn between Moncler and Stone Island as brands, their target demographics and thought processes are wildly different. While Moncler had built a strong foundation in the premium outerwear segment, Stone Island gave it access to a broader and younger demographic – consumers who might not buy a €2,000 puffer but who were still willing to dish out hundreds for a jacket from Stone Island.

Stone Island, in many ways, acts more as a diversification and complement rather than a competitor that's been brought under the control of Moncler. The goal was to create synergies that could benefit both brands while maintaining their separate and distinct brand identities:

“As you know, we received a lot of order to buy some company in the near future in the last 2, 3 years, but we always refuse because we never found the right company, the right position and the right idea of what we have in mind to develop this world for the near future. Having said that, when we start talking with Stone Island, we soon realized that it was very, very similar to our mentality to our culture. It was very similar, was Moncler like more or less 10 years ago, the company is very wholesale. They just start the retail. The real experience is in wholesale, for sure. I think the culture they have in the company is very strong in terms of product, in terms of production.”

– Moncler CEO Remo Ruffini, at the Q4 2020 earnings call (sourced through Quartr Pro).

But, as Ruffini makes clear, he also saw an opportunity to apply the same playbook that has made Moncler so successful to Stone Island. But there was one advantage when comparing the situation to the one Moncler was in during the early 2000s: Stone Island was in a much better position from the get-go. Today, many of the strategies employed by Moncler are more or less mirrored by Stone Island, even if some minor differences in approach remain.

As a brand, Stone Island more or less remains the same as it was before the acquisition. It's still aimed at the same type of consumers, its design language hasn't changed dramatically, and its loyal following remains.

When Moncler launched its Genius project in 2018, it was a calculated strategy rooted in changing consumer behavior, and all in all, it has been a massive success. While heritage is still Moncler's foundation, Genius has been the perfect way to expand and engage with a broader, faster-moving fashion landscape while also benefiting from the marketing possibilities of working with famous designers.

At its core, Genius is about combining variety with limited availability: more designers, more perspectives, more product lines, released in tightly controlled quantities. As a complement to the standard spring/summer, fall/winter collections (which Moncler still uses), the Genius drops happen through a monthly format and are deeply integrated with digital platforms. The products increase in diversity, but each release remains exclusive and unique.

The goal isn't to overwhelm the market but to maintain interest and relevance through measured, curated scarcity. When the latest Genius drop is sold out, it's gone for good. The limited nature of each drop creates urgency, and hesitation to buy can often mean missing out. This is where scarcity is a part of Moncler's strategy. Sure, you might be able to buy a standard puffer at any time, but if you want something special from your favorite designer, you have to be quick on the trigger.

The Genius model also makes sense financially. At first glance, working with a wide range of designers and introducing more frequent collections might appear costly and operationally complex. In reality, it created a more flexible and efficient commercial structure. Each Genius collaboration acts like a mini capsule collection: limited volume, high interest, low markdown risk. The exclusivity justifies premium pricing, and the low production runs reduce the chance of overstock.

In an industry where excess inventory can erode both profits and brand value, scarcity can act as a protective measure. Rather than chasing volume, the company focuses on value, ensuring that demand consistently outpaces supply. This balance allows Moncler to maintain high sell-through rates and minimize discounts. In turn, it also supports the company's strong operating margins, which have sat at roughly 30% over the last two years.

This approach also helps Moncler maintain pricing power. In the luxury sector, pricing strength usually comes from heritage, quality, and exclusivity. Genius showed that it can also come from novelty and good old-fashioned FOMO. The garments are still high-end and of excellent quality, but much of the appeal comes from owning something from a limited collection.

Trying to define what is and what isn't a luxury brand has proven to be difficult and far from an exact science. Throughout this article, we've consistently referred to Moncler as a luxury brand, but those well-versed in the sector might object to this. In the Quartr Edge editorial team, this question also came up and led to a subsequent discussion about what luxury truly entails – and whether or not Moncler and Stone Island should be classified as such. The answer? It depends on your criteria and, perhaps more importantly, who you ask.

Sure, the clothes are expensive and sold in exclusive boutiques in prime locations. But is it true luxury? Not if you ask Jean-Noël Kapferer and Vincent Bastien, experts on luxury branding and authors of The Luxury Strategy. In this (excellent) book, the authors share their views on what truly defines a luxury brand, which partly fits well with Moncler and Stone Island: intrinsic quality, heritage, controlled distribution, and serving as symbols of status and wealth.

However, both brands lack some of the key defining features of what it means to be a “true luxury” brand. According to The Luxury Strategy, a true luxury brand does not justify its high prices with functionality, which is a key selling point for both Moncler and Stone Island.

Yes, the jackets are expensive, but they also serve a very clear purpose. While a Louis Vuitton bag is full of craftsmanship, you're also paying a very hefty premium for the fact that it has the distinctive LV pattern on it, and it won't be any better at carrying your belongings than something you pick up at a discount from some other manufacturer.

But more importantly, Moncler and Stone Island don't intentionally create scarcity to drive up exclusivity across all of their products. Creating desire and status through rarity is a key feature of the luxury strategy and is not something that either brand employs on a large scale. If you wish to purchase, for example, a Moncler puffer jacket, you are almost always able to do so either in-store or online.

This is in stark contrast to how Rolex or Hermès will make you wait on a list, often for years, before you (if you're lucky) get the chance to buy one of its most coveted products. However, they do work with scarcity in a different way: limited drops and special collections, as made evident primarily through the Genius project.

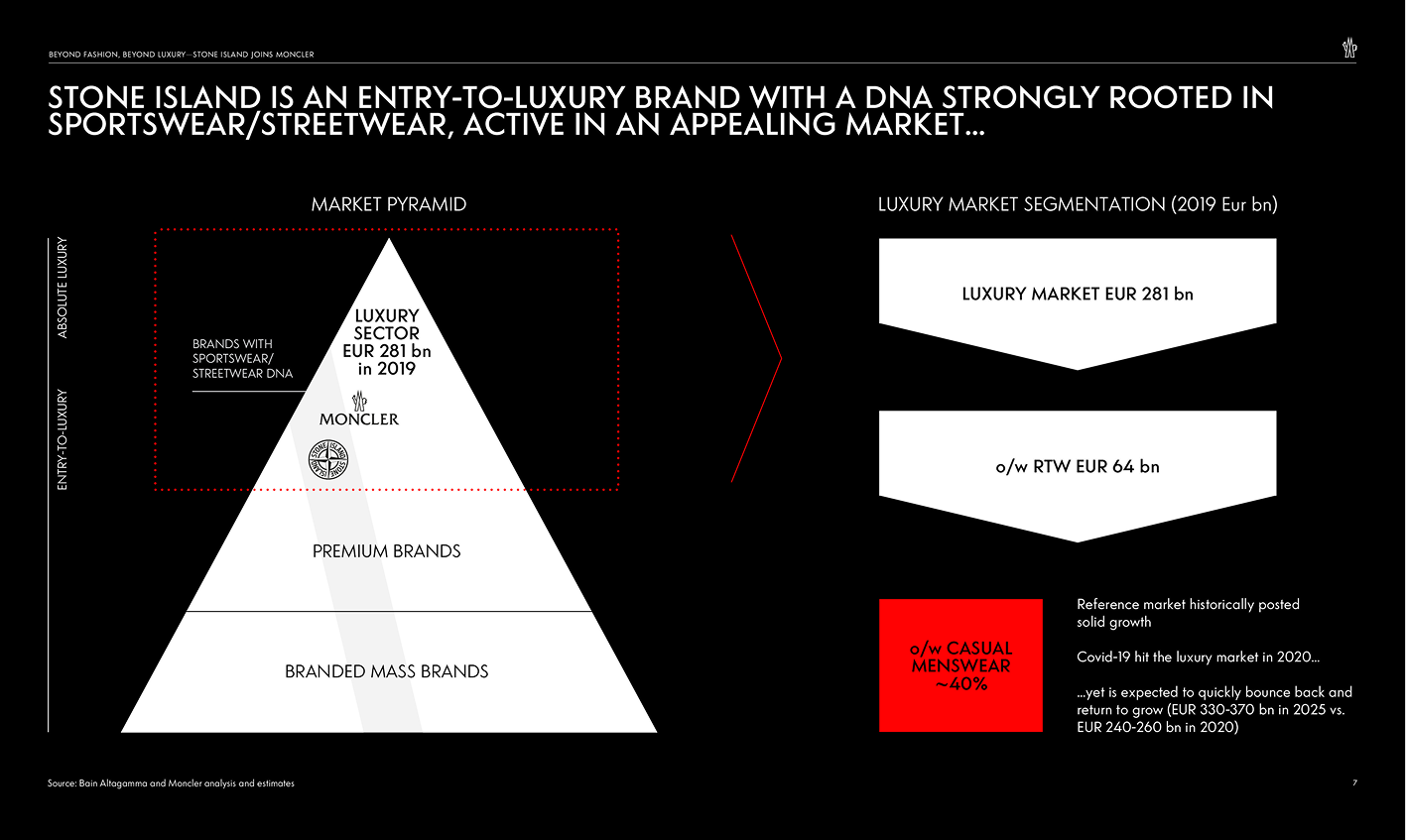

We're about to discuss “New Luxury” that was mentioned in conjunction with the acquisition, and what it entails in a minute. But due to its vagueness and the fact that it's more of a strategy mixed with marketing speech, we're going to be a bit more direct: Stone Island is what Moncler views as an entry point to luxury. Priced above, and more often than not, higher quality than premium brands, while not as expensive as other luxury brands. This slide from the M&A announcement back in 2020 illustrates very well how the two brands are positioned: as entry-level luxury.

It does get a little overly-complicated, but as you can see, Stone Island is positioned just above premium brands but far away from “absolute luxury”, with Moncler sitting just below the top of the pyramid. While this might seem overly convoluted, it's important to keep this in mind when trying to understand the two brands and how they position themselves.

But at the end of the day, luxury is subjective. It's the opinion of the writer of this article that when a T-shirt runs for €200+, or a puffer jacket or trench coat costs 3-10x more than the competition in the traditional premium segment, you're dealing with a luxury product. But is it true luxury? Perhaps not.

In recent years, Moncler has been outspoken about its desire to lead what it calls “new luxury.” At its core, it's a response to a luxury landscape that is evolving, and in which Moncler doesn't really fit. While it's not been said outright, it more than likely also has to do with the fact that it's quite happy sitting in its current spot in the market – above premium and below true luxury – and wants to employ a new definition to use when talking about itself and its strategy. But when you take away the marketing buzzwords and everything else, what does it really boil down to?

The brand believes that the luxury sector has become more fluid, more digital, and more culturally dynamic. Consumers today, especially younger ones, want more than just products. They want brands that feel relevant.

The modern consumer in Asia (the largest and most important market for the group), or anywhere else in the world, might not place a similar amount of value in regards to heritage as someone who wants to buy a Birkin because of the bag's history. Therefore, setting trends and being at the forefront of discussion has become much more important for brands like Moncler.

“New luxury” also entails meeting customers online. In the social media era, a product's appeal extends beyond its physical attributes. Storytelling, timing, and perceived uniqueness play an increasingly important role. Moncler has identified this and positioned itself to align perfectly with it.

But it wouldn't be too far of a stretch to claim that in many ways, Moncler and Stone Island are rewriting the luxury playbook. In some aspects, both brands operate by following the traditional playbook of luxury and premium companies while also doing things that are perfectly tailored to appeal to the modern consumer.

As we discussed previously, Moncler and especially Stone Island act as a sort of “Entry to Luxury” for consumers who are willing to pay large sums of money for these brands, without spending the amounts needed to wear brands like Brunello Cucinelli. Now, do you want to call it entry-level luxury or new luxury? That's up to you to decide.

Moncler is an incredibly fascinating brand and company. It has the heritage and prestige to categorize itself as a luxury brand while moving with the agility and purpose of a much smaller company. Through a strategic masterclass, Remo Ruffini has built a group that is well-positioned to continue defining its own future for decades to come. Moving slowly and with great purpose, Moncler is, in many ways, rewriting the luxury playbook and is showing that sometimes the old methods simply aren't good enough if you wish to stay relevant. Who knows if “New Luxury” is going to enter the vocabulary of other fashion brands, but one thing is certain: Moncler has found its niche and is exploiting it perfectly.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

Mobile

)

)

)