Inside HelloFresh: The Meal Kit Monopoly

In a world increasingly moving online, HelloFresh stands out as a dominant force in the global meal kit industry. With a blend of operational excellence and a keen understanding of consumer preferences, HelloFresh has secured roughly 75% of the meal kit market in the US and Europe. Join us as we explore the intricacies of HelloFresh's strategy, including its business model, potential risks for disruption, and its competitive landscape and advantages.

HelloFresh: a founder-led monopoly

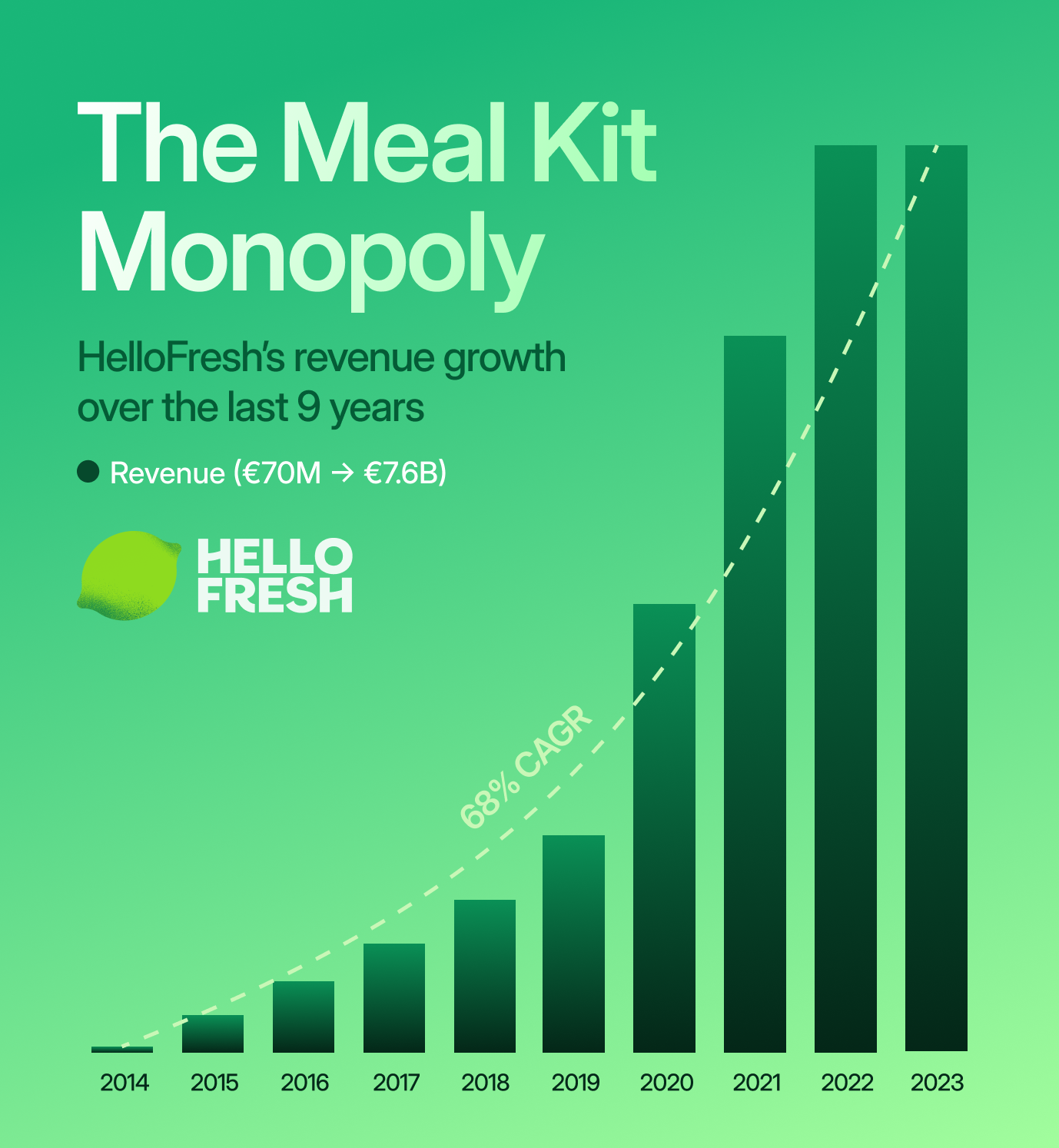

HelloFresh holds a monopoly in the global meal kit industry with its ~75% market share. The company's technology-driven strategy has not only significantly increased its market share but has also been successfully replicated across various markets. Over the past decade, HelloFresh has demonstrated superior execution, emerging as the only profitable entity in the meal kit industry at scale.

HelloFresh is likely to further solidify its advantages through countercyclical capital investments aimed at expanding capacity to meet demand comfortably. During the peak of COVID, when profit margins were around 15%, the company increased its capacity and reduced marketing expenses to strengthen its cash position, which can now be leveraged for buybacks.

Under the stewardship of its co-founders, Dominik Richter and Thomas Griesel, who have remained deeply committed since the company's inception in 2011, HelloFresh continues to thrive. Their significant equity stakes and strategic decisions underscore their dedication to long-term value creation. Notably, insiders own roughly 7% of the company.

At its core, HelloFresh is not just a meal kit provider but a direct-to-consumer technology company that excels in product innovation, supply chain optimization, and brand development. It has effectively monopolized each market it enters, driven by a product offering that expertly balances quality, value, and convenience. This, combined with HelloFresh's scale and diminishing competition, suggests that future growth will be accompanied by improved unit economics and higher incremental cash flow margins.

Business model

HelloFresh employs a direct-to-consumer e-commerce business model, focusing on a solution for home-cooked dinners. The company offers flexible meal kit plans for couples and families of four, with subscriptions allowing for 4-24 meals per week. While the term "subscription" might evoke thoughts of a software-as-a-service (SaaS) model with over 90% annual recurring revenue, HelloFresh operates differently. The model caters to a diverse customer base, including seasonal, occasional, or frequent users. Customers often integrate meal kits with other dining solutions, valuing HelloFresh for its convenience and reasonable pricing that fits their lifestyles. Thus, it's more accurate to describe HelloFresh as a direct-to-consumer e-commerce entity with some subscription model characteristics.

Sign up for Edge

Get curated quality company deep dives every other week.

Founded in 2011 to innovate within the stagnant home cooking industry, HelloFresh offers: (i) variety, with around 50 rotating meal options weekly; (ii) convenience, delivering fresh, pre-portioned ingredients for meals under 40 minutes; (iii) simplicity, providing easy-to-follow recipes; (iv) reliability, serving over 1 billion meals annually; and (v) value, with meal prices ranging from $6 to $13. Now serving 8.0 million active customers in 15 countries, HelloFresh aims to be a leading integrated food solutions group, offering a more customizable and flexible selection. Beyond meal kits, the company has expanded into ready-to-eat meals (Factor) and an ingredient marketplace.

HelloFresh's success over competitors is attributed to its technology-driven approach to decision-making since inception. The company entices new customers with initial promotions, understanding the high likelihood of churn post-promotion. Over the past decade, this strategy has enabled HelloFresh to amass extensive customer data, continually refining its offerings and growing its customer base at a 50% CAGR from 2016 to 2022. Remarkably, as previously mentioned, HelloFresh stands out as the only profitable meal kit provider in the industry at scale, under various economic conditions, and as the sole international success story within this space.

Unit economics in the meal kit industry

The meal kit industry is characterized by its capital-intensive nature and high barriers to entry, which often result in a winner-take-all or winner-take-most scenario for companies that achieve scale. For newcomers, procurement and fulfillment costs typically account for about 80% of sales – 40% each. Procurement involves sourcing fresh ingredients from local suppliers, while fulfillment encompasses processing, assembling, and delivering meals to customers. Establishing a brand that can attain the necessary scale for success usually means allocating around 25% of sales to marketing, with general and administrative expenses (G&A) making up about 5-10% of sales, and depreciation and amortization (D&A) between 2-3%. The question then arises: How can profitability be achieved in the meal kit sector?

The answer lies in achieving substantial scale. HelloFresh, serving over 1 billion meals annually, leverages its significant bargaining power to secure increasingly favorable terms from suppliers, reducing procurement costs from 40% to 34% of sales over five years. Furthermore, HelloFresh operates with negative net working capital (-5% of sales), as it pays suppliers after collecting payments from customers.

In marketing, HelloFresh has attained approximately 80% brand awareness in key markets and has significantly reduced its marketing expenses from 26% of sales in 2016 to 17% in the first nine months of 2023. Prior to the COVID-19-induced demand surge, HelloFresh achieved mid-single digit operating cash flow margins – a feat unmatched by most competitors, with UK based Gousto being a notable exception. The current margin has significantly decreased, influenced by the pandemic's repercussions and the challenging economic climate for European consumers. Nonetheless, taking a broader perspective reveals that HelloFresh has convincingly demonstrated its ability to expand revenue and produce free cash flow, suggesting that the present unusual circumstances may not accurately represent the company's true profitability and potential.

At maturity, well-established meal kit companies can target a terminal EBITDA margin of around 10%, a milestone already achieved by HelloFresh in Germany. With its negative working capital and nearly 100% free cash flow conversion, the long-term unit economics for HelloFresh – and potentially for other players in the meal kit industry – appear significantly more favorable than those of many traditional e-commerce businesses.

The unit economics of a meal kit customer are determined by the cumulative contribution profit, which is the product of the average order value, variable contribution margin, order rate, and retention, minus the upfront investment in customer acquisition cost (CAC). Once a meal kit company has adequate fulfillment capacity, it typically sees a positive contribution profit from the second customer order, which tends to increase over time. However, achieving these unit economics is challenging because customer loyalty tends to waver after the initial promotional order unless the perceived value for money is exceptionally high.

The CAC can be divided into two categories: (i) net CAC and (ii) gross CAC. Net CAC appears in the profit and loss statement (P&L) as a marketing expense, estimated to be around €60-80 per new customer. On the other hand, gross CAC is not reflected in the P&L but is accounted for above the revenue line, where new customers receive discounts typically on their first four orders. The discount structure is often 50% off the first order, followed by 35% off the next two orders, and 25% off the fourth order. Considering an average order value (AOV) of $70 and applying these discounts, the gross CAC amounts to slightly over $100 per customer.

HelloFresh stands out as the sole company that has successfully developed a profitable business model in the face of customer churn. This success can be attributed to its superior customer retention and reactivation strategies, which effectively reduce CAC over time. A reactivated customer incurs an estimated net CAC of approximately €0-20 (marketing expense) and a gross CAC of €20-30 (discount on the reactivation order). It is, however, important to note that the current CAC is significantly elevated due to the surge of new customers during the pandemic, with HelloFresh quadrupling its top line since 2019. Interestingly, the revenue hasn't dropped yet since peak COVID, unlike for the majority of other e-commerce businesses.

The cash flow generated from the tens of millions of customers who have tried HelloFresh's products is reinvested into advanced data algorithms. These algorithms enhance the company's ability to optimize ingredients, recipes, and menus, thereby attracting new customers and retaining existing ones. Even if some customers cancel their subscriptions after the initial months, HelloFresh has demonstrated a robust capacity for reactivation, continually improving this customer cohort.

The likelihood of smaller meal kit operators capturing market share and achieving sustainable profitability is slim. This is particularly evident in the US where HelloFresh commands approximately 75% of the market share and is still expanding. Competitors are caught in a dilemma: they must either enhance their Lifetime Value to Customer Acquisition Cost (LTV/CAC) ratio on a relatively small customer base or aggressively invest in brand growth and scaling.

Opting to improve the LTV/CAC ratio might yield short-term gains, but the industry's generally low customer retention rates, combined with a lack of scale, could hinder sustained investment in product offerings to maintain customer loyalty. Conversely, while substantial marketing investment might boost brand visibility and attract customers, the complex nature of meal kit operations means that any scale-related missteps could significantly damage the brand.

As the landscape of smaller, loss-making competitors decreases in an era of financial restraint, particularly within the food delivery and food tech sectors, larger firms may find opportunities for consolidation or market share expansion. Thus, HelloFresh's operational leverage is poised to increase both the cumulative customer contribution profit and reduce customer acquisition costs. Looking ahead over the next 5-10 years, there is a plausible scenario in which HelloFresh could sustain a free cash flow margin of 10-15%. The HelloFresh business model flywheel:

How is the meal kit industry structured?

The meal kit industry occupies a specialized niche within the online food consumption sector, which remains significantly underpenetrated compared to other consumer markets. Meal kits vie for consumers' at-home dining expenditures, competing directly with supermarkets and food delivery services.

The competition focuses on three key aspects: price, quality, and convenience. Generally, supermarkets are known for their convenience and competitive pricing, whereas the food delivery sector is associated with convenience and quality. Despite supermarkets' efforts to expand into online grocery services to challenge meal kits, various limitations inherent to their business model and financial status prevent them from effectively competing in the same niche. When these factors are taken into account, it becomes evident that meal kits have successfully carved out their own distinct segment within the vast food industry.

Industry growth and cyclicality

The meal kit industry has been experiencing healthy growth and is expected to continue this trend over the next decade. YipitData reports a 27% compound annual growth rate (CAGR) from 2017 to 2022, and a 21% CAGR over the three years starting from January 2017. The industry was undoubtedly a significant beneficiary of the COVID-19 pandemic, yet it still possesses considerable potential for expansion.

Both the category's market penetration and online food penetration broadly remain low compared to other online consumer goods. Given the food industry's magnitude and the escalating demand for meal kits, a modest shift in customer spending towards online platforms could sustain robust double-digit growth annually for meal kits. Despite the waning of pandemic-related benefits, the global meal kit market is projected to expand at a 17.4% CAGR through 2030, according to Statista (2022), with the US market expected to grow at a 14% CAGR in the coming years, as per Coresight Research (2021).

Furthermore, the increasing trend toward remote work is likely to support meal kit industry growth, as more individuals cook at home. Although the peak of remote working has passed, the shift toward such arrangements began before the pandemic and is anticipated to continue. Between 2015 and 2019, the number of US employees working from home rose from 3.9 million to 4.7 million, as reported by Global Workplace Analytics (2021).

The pandemic demonstrated that businesses could operate remotely for prolonged periods without significant performance drops. Additionally, a 2019 study by Global Workplace Analytics found that employers saved an average of $11,000 per part-time remote worker. Employees now place a higher value on remote work opportunities, which, in the current tight labor market, can serve as a negotiation point with employers. This is illustrated by the record 4.5 million US employees who resigned in November 2021, a phenomenon known as "The Great Resignation," partly driven by a demand for improved remote work policies (CNBC, 2022).

To what extent is the meal kit industry at risk of disruption?

Online vs. offline

The trajectory of the food industry in developed economies is increasingly leaning towards online platforms, mirroring trends in other consumer goods sectors. This shift is largely driven by the growing consumer preference for convenience. While changing consumer habits is a gradual process, the COVID-19 pandemic has significantly accelerated the transition to online food purchasing, demonstrating its viability in competing with traditional offline options. Although offline channels, such as supermarkets, will continue to serve home cooking needs, consumer expectations around value, quality, and convenience are evolving, necessitating that food solutions adapt accordingly to retain relevance and market share.

Meal kits vs. online alternatives

Broadly speaking, if food is delivered to your door you either must cook it yourself or it is cooked for you. Consumers prioritize different factors, such as price, quality, or convenience, which influence their purchasing decisions. Meal kits, however, cater to a broad range of consumer preferences, making the category relatively resilient against other online food alternatives. Disruption in the meal kit sector would require competitors to excel in areas such as cooking time reduction, health benefits, and variety – a formidable challenge while also maintaining profitability.

At present, online grocery shopping represents the most significant potential source of disruption for the meal kit industry. However, competing in this space is cost-intensive, requiring an industry already operating on razor-thin margins to accept suboptimal ROIC for 5-10 years to justify the investment. Even if consumers were to shift from meal kits to online groceries to reduce supermarket visits, the latter still falls short of offering the same level of convenience as meal kits.

While meal kits save consumers considerable preparation time with pre-portioned ingredients, some may prefer even quicker solutions. In this context, ready-to-eat meals are gaining popularity as time savings become a more critical factor in consumer choice than other considerations. Nonetheless, among meal kit providers, HelloFresh is exceptionally well-positioned to navigate this risk, particularly after its acquisition of Factor – a ready-to-eat meal service renowned for its taste and health benefits. Since being acquired by HelloFresh, Factor has more than tripled its sales, establishing itself as the leading brand in its category in the US.

Ready-to-Eat (RTE) meals

HelloFresh's RTE brands, Factor in the US and YouFoodz in Australia, have rapidly become the dominant players in their respective niches. For instance, in the US, Factor has significantly outperformed its main competitor, Freshly, even though the latter had a stronger customer offering according to an earlier independent customer proposition analysis.

HelloFresh's integrated technology infrastructure has enabled Factor to adopt the company's best practices in customer acquisition, engagement, and retention. These strategies allowed Factor to triple its market share within 18 months after being acquired in late 2020, reaching over 50% and securing its position as the top RTE meal brand in the US.

So just a very quick 1-minute summary. What is our strategy for 2023. Advanced markets continue to improve the customer proposition. That will improve unit economics, that will allow us to penetrate those markets more deeply as we lap and outsized Q1 2022 in the second half of this year. Underpenetrated markets, lots of TAM upside. We're going to work on closing the feature gap. It's a proven playbook. We've done many times in our advanced markets, have great confidence that we get to the same penetration levels as an advanced markets over time. RTE, huge opportunity, strong moats, strong defensibility, full focus is on unlocking additional capacity and then doubling revenues over the next 3 years. And new brands and geos will exercise very strict capital discipline. But we think the track record of all the businesses that we've launched in the last 5 years actually makes this a very compelling opportunity to also leverage a lot of the D2C capabilities that we've built in the business over the last 5 years. That's in a nutshell, the story for 2023 and beyond. After this 1-hour monologue, I think you're all looking forward to hearing from some other speakers. So I'm very happy to pass on the microphone to my colleagues, Uwe, U.S. CEO; and Joanna Hicks, our SVP Operations in the U.S.

– Dominik Richter, CEO of HelloFresh, at the company's 2023 CMD (sourced through Quartr Pro).

This success is partly due to the unique customer acquisition channels, which are digital-first, contrasting with the offline-led approaches of competitors like Nestlé and traditional supermarkets. Many consumers choose RTE meals to avoid supermarket visits, highlighting a key market advantage for HelloFresh. The company's competitors lag significantly in data accumulation, a crucial aspect of market leadership. Intriguingly, HelloFresh's Q2 2022 earnings call revealed that its RTE customers view the category as an alternative to restaurant takeout. Consequently, Factor's pricing remains significantly lower than its competitors', and without the additional platform fees or tips, this pricing strategy is likely to diminish competitive pressures over time. RTE could also become an attractive B2B offering unlike meal kits. According to HelloFresh's recent 2024 investor update, RTE is projected to growth with 50% during 2024 and constitute approximately 25% by the end of the year, offering the group a fresh narrative for further growth.

In particular, the success story of Factor stands as a testament to the management's ability to identify a new customer segment and rapidly dominate the category, leveraging shared expertise from HelloFresh's front-end (customer interactions) and back-end (fulfillment capabilities). Factor has tapped into a distinct customer demographic compared to its core customer base with huge success in a short period of time.

Supermarkets

Supermarkets are highly likely to remain the primary source for home cooking ingredients, largely due to deeply ingrained customer habits. These habits encompass preferences like physically inspecting food before purchase, opting for packaged over fresh food, and lifestyle factors that limit meal kit feasibility, such as work hours and travel commitments. Additionally, a significant segment of consumers, particularly those with limited disposable income, might not consider meal kits as a viable option.

Discount supermarkets like Aldi and Lidl, for instance, utilize their procurement scale to offer aggressively low prices, intensifying competition. While HelloFresh, even through its EveryPlate brand, doesn't target this budget-conscious demographic, the pervasive influence of discount supermarkets, especially in Europe, could potentially constrain HelloFresh's pricing flexibility.

However, in markets like Germany, where Aldi and Lidl are well-established, the discount segment has consistently held around 25% of the grocery market share. This suggests that approximately 75% of consumers prioritize factors beyond just price, indicating an area where competition might intensify.

Online grocery and competition

The rise in online grocery services may modestly heighten competition. Supermarkets across the Atlantic are progressively introducing online options, appealing to customers who prioritize avoiding supermarket visits and prefer the flexibility of creating their own recipes. Yet, only 16% of meal kit customers primarily value the reduction in shopping trips and sourcing efforts. Interestingly, the growth in online grocery, which accelerated during the COVID-19 pandemic, could inadvertently benefit HelloFresh, a company that thrives in the digital acquisition space. Even if online grocery reaches a 10% penetration rate, HelloFresh's expertise in digital channels positions it well to capitalize on this shift.

Structural challenges for supermarkets

Supermarkets face inherent structural challenges that limit their ability to compete with HelloFresh in the long term. Supermarkets rely on large-scale procurement and extensive physical stores to attract customers, a model fundamentally different from meal kits. Historical attempts to integrate meal kits into supermarkets have not succeeded, highlighting a mismatch in customer acquisition channels. People opt for meal kits to avoid the hassle of traditional grocery shopping and meal planning.

Moreover, the supermarket industry's SKU-based model contrasts sharply with that of meal kits. While a typical supermarket carries around 50,000 SKUs, HelloFresh offers approximately 300, focusing on a demand-driven model that anticipates ingredient needs in advance. In contrast, supermarkets operate on a supply-driven model, resulting in longer shelf lives and the need for preservatives, which can compromise freshness and healthiness. Meal kits offer fresher ingredients with less waste, attributes that could become increasingly attractive to consumers over time.

Also, supermarkets' financial structures, characterized by low-to-mid single-digit profit margins and significant overhead costs, constrain their ability to innovate and compete effectively in the meal kit segment. Political pressures to keep food prices low further restrict their ability to improve margins, leaving them in a position of structural disadvantage relative to specialized meal kit providers like HelloFresh.

Supermarket companies also typically feature highly conservative management teams focused on incrementally raising prices and volumes each year while distributing substantial dividends to satisfy shareholders. This culture does not prioritize restructuring the cost base to invest in new concepts, as evidenced by the industry's sluggish adoption of online grocery services.

Most supermarkets even outsource their online grocery logistics due to a lack of internal expertise, highlighting their reluctance to embrace operational changes. Given that there's no third-party solution for meal kits, it's hard to envision supermarkets successfully transitioning to the operationally demanding, just-in-time fulfillment process that meal kits require – a shift that could entail years of losses, even if executed flawlessly.

Moreover, the financial health of the sector further restricts supermarkets' ability to pivot. In the US, leading supermarket chains carry at least twice the leverage of HelloFresh, with inferior cash conversion and asset turnover. The situation is even worse in the UK. Tesco and Sainsbury are almost 5x geared with inferior cash conversion and asset turnover less than half that of HelloFresh. This financial context, marked by limited cash flow for significant innovation towards a meal kit model, underscores why the prospect of increased competition from supermarkets remains low.

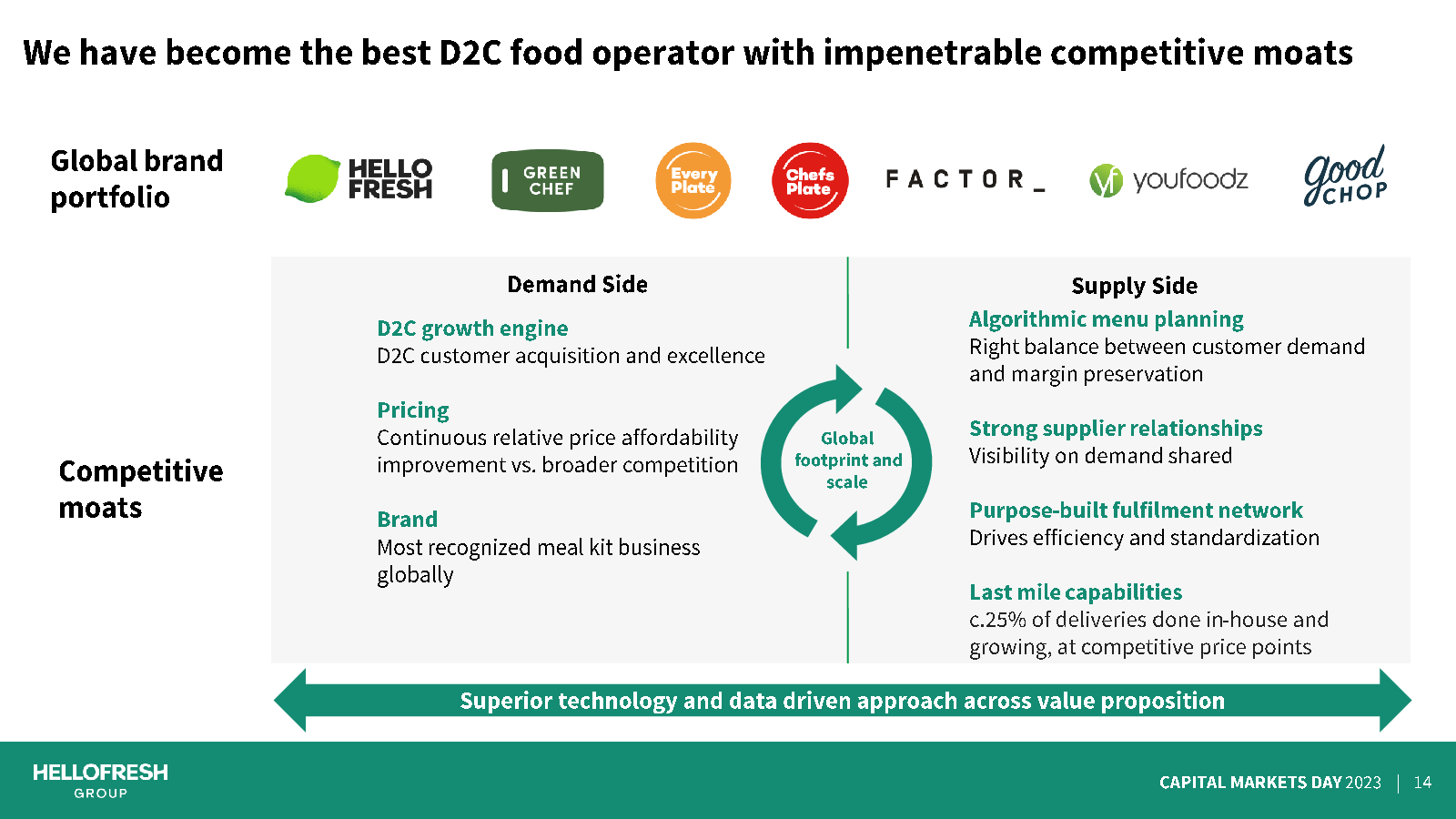

HelloFresh's competitive advantage

Source of moat: HelloFresh has built a significant competitive moat by consistently outperforming competitors for a decade in an operationally complex industry.

Leads to critical scale: This executional excellence has allowed HelloFresh to become the only meal kit company to achieve significant scale and profitability, irrespective of the macroeconomic environment. Unlike its competitors, HelloFresh's robust cash flow supports ongoing innovation and covers high fixed costs.

Leveraged to widen the moat: HelloFresh uses its extensive customer data and advanced, technology-driven algorithms to enhance the customer experience continually. This approach improves unit economics, enabling further investment to expand the competitive moat. The enhancements in HelloFresh's offerings are beginning to reflect in its unit economics and have substantial potential for future growth.

Sustained over time: HelloFresh's industry-leading operating cash flow margins, negative net working capital, net cash position, and high asset turnover position it to outcompete smaller, less focused rivals.

What is the source of HelloFresh's moat?

HelloFresh has developed and showcased its competitive moat by outperforming rivals for over a decade in a highly operationally complex industry. Delivering fresh food accurately to customers seems straightforward, but achieving this at a scale that ensures profitability is very challenging.

Success requires excellence not just in procurement, fulfillment, distribution, and shipment of high-quality ingredients but also in efficient marketing to build a strong brand or portfolio of brands. This brand must resonate with a specific customer segment, offering a personalized and consistently high-quality experience. When a company can outperform competitors by even 1-2% annually in these areas, the advantages compound over time, leading to significantly better outcomes compared to the competition.

The result is a significant competitive moat. Although switching costs for HelloFresh remain low, as meal kit usage hasn't become a mainstream habit yet, they are on the rise, thanks to the company's 'secret sauce.' This secret sauce is the technology-driven decision-making that utilizes customer data from the billions of meals served over the past decade. Over time, HelloFresh's growth flywheel (referring to figure 2) is expected to lead to improved customer unit economics, supporting sustained double-digit growth with increasing margins.

Brief management quality summary

Track record of execution: The HelloFresh management team's execution in a complex industry is exceptional. This performance has been consistent both before and during COVID-19, across the US and international divisions. The year 2024 will test the management's abilities in the most challenging operating environment since the company's IPO.

Alignment: The management team is highly aligned with the goal of long-term value creation. More than a decade after HelloFresh's launch, co-founders Dominik Richter and Thomas Griesel still occupy the top two executive positions. Together, Richter and Griesel own approximately 5% of the company, coupled with modest fixed compensation, demonstrating their commitment to the company's success.

Culture built for long-term value creation: Former employees highlight that Richter's determination to build a company that delivers long-term customer value is a defining strength of HelloFresh. Richter himself perceives insufficient innovation as the company's most significant risk. Therefore, he fosters a culture focused on consistent 1% improvements, which have compounded over time and are expected to continue doing so.

Shareholder centric: HelloFresh has 1) an active buyback program during 2024 for €150 million, demonstrating that the management prioritizes shareholder value creation (they also bought back shares during 2022), and 2) a management team that is generally focused on free cash flow per share in their investor relations communications, which is always a positive sign.

Conclusion

HelloFresh's dominance in the meal kit industry is underpinned by its technology-driven strategy, robust business model, and founder-led leadership, positioning it for sustained growth. With a substantial market share and effective scale economies, the company is poised to maintain its profitability and competitive edge. Its diversified product offerings and customer-centric approach continue to drive its success, differentiating it in a sector where others struggle to achieve profitability. As the industry evolves, HelloFresh's strategic investments and operational efficiencies are expected to further solidify its leadership position, capitalizing on the ongoing shift towards online food consumption and the increasing consumer demand for convenience, quality, and value.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

)

Desktop

)

API

)

Mobile