)

)

)

)

Company research10 Jun 2024

Ken Xie: From Stanford to Fortinet

Learn how Ken Xie built Fortinet from a startup to a global cybersecurity giant, balancing cloud services and hardware innovations.

At first glance, it is easy to stereotype Jensen Huang as your archetypical big-tech CEO. He doesn't wear suits like a Wall Street chairman, instead opting to wear his now-iconic leather jackets and casual polo shirts. He can convey how his incredibly complex products work in a way that makes anyone understand, and he's seen his net worth skyrocket together with the value of the company he leads. But NVIDIA hasn't become a trillion-dollar company by selling software that is more or less infinitely scalable and deployable – the company he co-founded has grown by selling some of the most innovative computer hardware ever produced. As the world continues to change at an ever-increasing pace, NVIDIA is cementing its place as the most important company of the AI era. While the story of his company is incredibly fascinating, the life and work of its figurehead is equally captivating and has been marked by a relentless pursuit of innovation and progress.

Jensen, whose first name is actually Jen-Hsun, was born in Tainan, Taiwan, in 1963, and the first years of his life were marked by frequent moves. Interestingly, Taiwan is today the world's leading nation in advanced semiconductor manufacturing. In fact, TSMC has been manufacturing NVIDIA's most cutting-edge chips for years.

When Jensen was five years old, the Huang family left Taiwan and moved to Thailand, but his stay in the country would not be long-lived. After Huang's father had been part of a worker-training program in the U.S. with the air conditioner manufacturer Carrier, he made a promise that he would send his children to America. His father had seen the opportunities available in the U.S. and believed it would be the best place for his sons to get an education.

While giving his children the opportunity for a better life was a major driver in relocating, it wasn't the only reason. The Vietnam War had raged for several years at this point, and the entire region was unstable. Jensen's father saw no end in sight for a conflict that was becoming bloodier and more intense every week. He would unfortunately be proven right in his predictions: Nixon would order massive bombing campaigns in Cambodia in 1969 and 1970, aimed at cutting off North Vietnamese supply lines. The following year, the U.S. Air Force and artillery crews hammered southern Laos, supporting a South Vietnamese offensive. The war was creeping closer and closer to Thai borders, and the Huangs wanted their children far away from the conflict and in a country with better opportunities.

To prepare her children for a future on the other side of the world, Jensen's mother, who didn’t speak or understand any English at the time, began teaching them ahead of the move. With no money for private tutors, she picked ten words from the dictionary every day, and Jensen and his brother would learn and repeat them back to her.

Slowly but surely, Jensen and his brother became more and more comfortable with English, and when they arrived in the U.S., they could make themselves understood. In 1972, he and his brother boarded a flight to Tacoma, Washington, to live with their uncle. Their parents stayed behind, saving up money and getting the necessary paperwork to join their children and start their new lives together. Needless to say, he is incredibly thankful for his parents' sacrifices and hard work and credits them with putting him in a position to succeed.

Get curated quality company deep dives every other week.

The Huang brothers were eventually sent to Oneida, Kentucky, to attend elementary school and live in student housing. While the brothers attended a regular school, they lived in housing shared with students from a military reform academy. The years following the move were tough for the young Jensen. As an immigrant with broken English, he had trouble fitting in with the so-called “problematic students” he lived with and was relentlessly bullied.

However, former classmates of Jensen's have said that he took it all well and didn't let the incessant bullying get to him. Throughout his time in Kentucky, he did well in school and slowly but surely made friends with his peers. One of the most commonly referenced instances of this is his relationship with his illiterate 17-year-old roommate. Jensen taught him how to read, and in return, the roommate showed him how to bench press.

Even though his time in Kentucky was tough, Jensen is convinced that the experience overall helped to make him a better person. He has made several charitable donations to his old school and the academy where he lived, and he seems to only focus on the positive experiences he had.

The parents later emigrated as well, and the family made their home just outside of Portland, Oregon, where Jensen was able to settle in better. While he still had trouble connecting with his fellow high school students from time to time, he excelled in his studies and worked his first job at a local Denny's.

He still speaks fondly of his time at the diner chain and the lessons he learned. Even as the CEO of a trillion-dollar company, Huang is proud of having worked his way up from a dishwasher to a waiter. Jensen has stated that his time at Denny's shaped his approach to work and stress profoundly, helping him to perform better under pressure. He says that his heart rate actually drops and that he performs at his absolute best when the stakes are high, something he credits in part to having worked through countless rush hours in his youth.

After high school, Jensen set his sights on higher education. He began his university studies at Oregon State University (OSU), where he earned a bachelor's degree in electrical engineering. He excelled at OSU, and this is also where he met his future wife, Lori, who was his lab partner in an electrical engineering class. After graduating from OSU and before moving on to Stanford and the eventual founding of NVIDIA, Jensen worked at both AMD and LSI Logic.

His time at AMD was short (Jensen was at the company for a little over a year) but laid the foundation for his future success in the industry. While with AMD, he worked on the design of microprocessors, small electronic devices that perform the functions of a central processing unit of a computer on a single integrated circuit.

After departing AMD, he was hired by LSI Logic (now owned by Broadcom). This was during a very exciting time in the company's history, as LSI Logic had gone public two years earlier and was still rapidly growing and expanding. LSI Logic was a semiconductor manufacturer whose products were used to improve storage capacity and network speed in areas such as networks and data centers. During his time there, Huang held several positions within the company, including engineering, marketing, and eventually general management positions. Working in such varied roles, including management positions, would prove to be a valuable experience in the future.

During his time at LSI, he studied during evenings and weekends and earned a master's degree in electrical engineering from Stanford in 1992, a year before founding NVIDIA. The academic environment of Stanford, combined with its culture of innovation and entrepreneurship, significantly influenced Huang's perspective and approach to technology. Jensen has made several charitable contributions to both OSU and Stanford during the 2010s, donating millions of dollars to his two alma maters.

NVIDIA was founded in 1993 by Jensen Huang, Chris Malachowsky, and Curtis Priem. The two other co-founders, who brought experience from Sun Microsystems and IBM, met with Huang at a Denny's just outside of San Jose. While eating diner food and drinking cheap coffee, the trio founded NVIDIA with $40,000 in starting capital. They initially called their company NVision until they learned that the name was taken by a manufacturer of toilet paper, and swiftly changed the name to NVIDIA instead. Huang has described NVIDIA during its founding as a company with a “market challenge, a technology challenge, and an ecosystem challenge with approximately 0% chance of success,” adding that he would not have funded NVIDIA during the company's infancy.

NVIDIA had a screaming need for external capital during the early days, and thanks to connections in the tech industry, Jensen and his co-founders were put in contact with Don Valentine. Valentine was one of the most influential venture capitalists in the industry at the time and was given the blunt advice to “give this kid money and figure out if it’s going to work.” That’s exactly what he did, and as we now know, Jensen made it work.

In a talk in 2023, Jensen described a “proud moment” that happened during the previous year relating to the founding of NVIDIA. He was contacted by the CEO of Denny's, who was happy to inform him that the booth where NVIDIA was founded had received a plaque with the inscription “The NVIDIA Booth - The booth that launched a trillion-dollar company.”

Huang loved video games and hypothesized that there was a brewing market for chips capable of displaying sharper and better graphics. Innovation in this space was happening at a rapid pace, and developers were starting to use three-dimensional polygons (built out of shapes called primitives) for video game graphics. NVIDIA chose to go down a different route than its competitors, opting to use quadrilaterals instead of triangles.

This would prove to be a near-fatal mistake. Shortly after NVIDIA sent its first product to market, Microsoft announced that the software used to process graphics would only support triangles. NVIDIA was, no matter how you look at it, in serious trouble. The company had taken a high-stakes bet and lost due to factors outside of its control during a time when there was no margin for error.

They could have given up here and simply folded the company, but Huang quickly devised a plan of action. He laid off half of the workforce, roughly 50 people, and then used all of the company's remaining funds to produce a series of untested chips using the triangle approach. He and the rest of the management team were far from certain that it was going to work, but if they didn't try, NVIDIA would go out of business regardless. When the chips, called RIVA 128, became available to consumers, the situation was desperate. The company only had enough money to cover salaries for the following month. The desperate move paid off, and NVIDIA sold a million units in four months, saving the company.

Teetering so close to the abyss had a profound effect on the company as a whole. When things were at their lowest, there was only one word that could be used to describe the atmosphere at NVIDIA headquarters: desperation. During the months and weeks leading up to the release of the RIVA 128, everyone at the company knew that this was it – either they did everything in their power to make it work, or they would all be out of a job.

This desperation and the subsequent focus it brought to everyone who worked at NVIDIA was something that Huang viewed as incredibly powerful and a feeling that he tried to capture in the following years. Following the release of the RIVA 128, he would start every presentation with what is now the unofficial NVIDIA motto: “Our company is thirty days from going out of business.”

Huang is also convinced that company culture is built when things are at their bleakest. According to him, it's impossible to create culture and core values during great times for a company. It is when a company faces adversity that culture is built. He argues that resilience is key to success, and in order to build resilience, one must suffer to a reasonable degree.

He explained his reasoning to students at Stanford in March 2024: You want greatness out of them (the employees), and greatness is not intelligence; greatness comes from character, and character isn't formed out of smart people. It's formed out of people who suffered."

NVIDIA was founded during a time when PCs were just gaining momentum, and the industry was just beginning to grasp the impact the Central Processing Unit (CPU) was going to have. NVIDIA’s founding team was convinced that CPUs weren't going to be the solution to all computational problems and envisioned a future of accelerated computing. They figured that if this vision came to life, the world would need specialized purpose-built hardware.

The product they built to capture this burgeoning market was the Graphics Processing Unit (GPU). Jensen describes a GPU as putting a specialist next to a generalist. In this analogy, the CPU acts as the jack of all trades, while the GPU solves more complex problems that the CPU cannot handle efficiently. However, success was far from certain. Huang has described the idea of GPUs as an “unfundable idea” due to how outlandish it sounded at the time.

In essence, NVIDIA was trying to build a completely new type of product without an existing application on the market, requiring massive R&D expenditure at a time when all eyes and venture capital were focused on CPUs. Wanting to build a product that complemented CPUs, with the primary application being 3D video games, seemed like a surefire way to fail.

Once again, Jensen believed in his vision. The GeForce line, as it would come to be called, was released in 1999, the same year that NVIDIA went public. The first product, the GeForce 256, was aimed at gamers who weren't particularly price-sensitive and were looking for the very best, with future models covering all spectrums of the market. The GeForce products ultimately became NVIDIA's flagship, and up until the AI boom, the company was most known for its GPUs aimed at video game enthusiasts.

CUDA, or Compute Unified Device Architecture, is a parallel computing platform and API created by NVIDIA and introduced in 2007. It enables developers to use the company's GPUs for general-purpose processing tasks, moving beyond their traditional role in graphics rendering. This shift to general-purpose computing on GPUs (GPGPU) allows for significant performance improvements in various computational tasks compared to conventional CPUs.

CUDA simplifies GPU programming by providing an abstraction layer that extends standard programming languages. In plain English, this means the following: CUDA enabled developers to use NVIDIA GPUs for a wide range of computational tasks, including scientific research, engineering, financial modeling, and, most importantly, artificial intelligence. The release of CUDA was met with mild enthusiasm, but a few years after it went live, it would prove to be a transformative product for the company.

When looking at the meteoric rise of AI and the impact of ChatGPT, it's easy to think that NVIDIA just happened to be in the right place, with the right products, at the right time. While this is true, it's not by accident, as made evident by initiatives like CUDA. The success that NVIDIA is currently enjoying through selling advanced hardware that makes programs like ChatGPT possible is the result of a focus on AI that has been a priority for the company for almost a decade.

At the beginning of the 2010s, AI was far from where it is today. The field was unpopular amongst computer scientists, and while some progress was being made, it was slow and quite frankly, unmotivating to work with. However, there was a breakthrough.

Neural nets, which had for a long time been disregarded, suddenly started making significant progress. A neural net, or neural network, is a computational model inspired by the way biological neural networks in the human brain process information. It consists of layers of interconnected nodes, or "neurons," which can learn to recognize patterns and make decisions based on input data. Using NVIDIA’s GPUs modified with CUDA, these neural networks could be trained up to 100 times faster than with traditional CPUs.

Following this breakthrough, Huang and his engineers moved quickly. He was convinced that neural networks would completely revolutionize society, and once again, he went all-in. Almost overnight, NVIDIA shifted from a graphics business to focusing on hardware for AI applications. While graphics cards for video games were still being developed and released under the GeForce line, the company's main objective was now to provide the most sophisticated hardware for AI applications.

The bulk of the company's time, effort, and money was now completely focused on AI, with the head of the AI research department able to pick and choose whoever he liked from NVIDIA’s current employees to join his team. By the mid-2010s, NVIDIA had pivoted completely and was no longer just a graphics company – it was an AI company.

In 2016, Huang personally delivered the first AI supercomputer to OpenAI, and in 2017, researchers began the work on what would eventually become ChatGPT. Following the program's release to the public, the interest in NVIDIA hardware has been enormous. At the time of writing this article, the company has had backorders for months, and due to being first on the scene, they have a massive head start on the competition.

While much can be said about the AI boom and what it means for the demand in hardware, a managing director at Raymond James described it perfectly in May 2023: “There's a war in AI out there, and right now, NVIDIA is the only arms dealer”.

Through decades of chip design innovation, specialized software, and a few strategic acquisitions, the company has been able to build a virtuous circle.

Huang has served as the CEO of NVIDIA since founding the company in 1993. During his time at the helm, the company has grown from three men in a booth at a local Denny's to a trillion-dollar company. One constant during this time has been his leadership.

However, Huang remains incredibly humble, and one can even get the sense that he himself has a hard time understanding how important he is to the company. Instead of talking about himself or his leadership, he deflects praise onto his teams. While Huang is quick to downplay his own importance at NVIDIA, his board members and employees have differing opinions.

He's been called everything from absolutely brilliant to completely irreplaceable and has been the most influential person in building the culture at NVIDIA. One of the clearest examples of this is his insistence on learning through failure. Whenever a product or an initiative goes terribly wrong (which it does from time to time), the immediate response is to try and learn from it. When something goes wrong, the people responsible hold so-called “failure presentations,” where they outline every single decision made during development and what led to the unsuccessful outcome.

Huang inherently dislikes hierarchies and structures. Instead of having team leads and product managers report directly to him, he prefers to have his employees send him brief emails outlining the most important things they’re working on that week.

Naturally, he still takes meetings and maintains an overarching view of the entire organization, but being informed on what is going on throughout the company is something he values deeply. He also encourages employees to work with experimental products for which there might not already be a competitor or even a market yet. Sometimes this works to great effect (CUDA once again acting as a great example), while other times it leads nowhere.

According to Huang, the most important thing is being able to choose. NVIDIA chooses to pursue things that are incredibly difficult to do for several reasons. One of the most striking aspects of this is that it discourages a lot of the competition, while also being something that is often inspiring to work on. Another factor of choosing things that are incredibly hard ties in with attracting the best of the best. By doing things that have never been done before and giving talented people the chance and patience to do what they do best, Huang states the outcome: great people go on to do great things.

Instead of working with people trying to capture a share of the market by cutting prices or making slight improvements on already established technology, Huang wants to hire people who are looking to build something groundbreaking. His goal from the start has been to create an environment in which people want to come and do their life’s work, and it's something that he has managed to do brilliantly. Despite the pressures of working for NVIDIA, the company is frequently listed as one of the best places in the tech industry to work, and its employee retention is very high.

“And one of the things that most touch me, in my 33 years doing this, one scientist said to me, Jen-Hsun, because of your work, I can do my life's work in my lifetime. And boy, if that doesn't touch you, well, you got to be a corpse.”

– Jensen Huang, at the NVIDIA GTC 2025 Keynote (sourced through Quartr Pro).

But all of this is to be done as fast as humanly possible. Huang has instilled the importance of speed across his entire organization. When planning a project, employees are instructed to first come up with the fastest possible way to do something given no limitations whatsoever. After applying the limitations, prioritizing, and finding the best way forward, the result is often being able to complete something in a shockingly short amount of time.

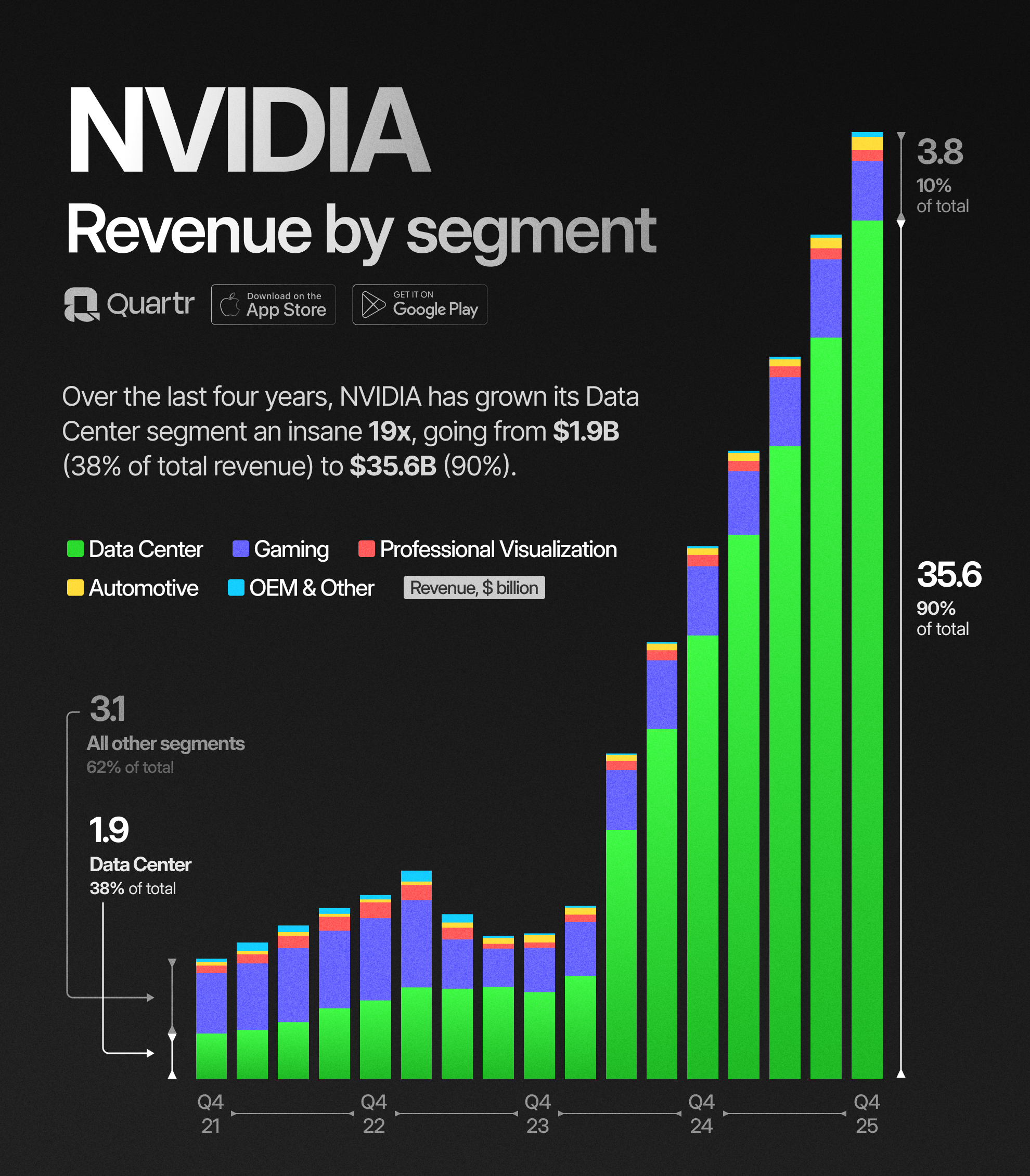

As we’ve been over numerous times in this article, NVIDIA has been perfectly positioned to both drive and take advantage of the AI boom. One of the business areas that has grown the most is its Data Center segment, and in just a few years has gone from roughly 40% of total revenue to a staggering 90%. While it's no secret that NVIDIA has grown exponentially in the last couple of years, seeing it visualized puts it all into perspective:

Jensen Huang is not someone who likes to talk too much about his personal life and family, choosing instead to keep the focus on his company. Huang is still married to Lori, his electrical engineering lab partner from OSU. He jokingly credits their relationship to his “killer” pickup line, which simply entailed offering to show her his homework. They have two children together and have collaborated on philanthropy projects.

Graphics cards and semiconductors seem to run in the family. Jensen and Lisa Su, the CEO of AMD, are related. Huang and Su are first cousins, and while this is something that is far from being a secret, the two don't appear to be very close and rarely speak of each other in anything other than professional terms. The pair are both originally from Taiwan and share family ties, but did not know each other growing up and it appears they see each other mainly as competitors rather than cousins.

The story of Jensen Huang and the founding of NVIDIA is partly one of the sacrifices made by parents to give their children a better chance at life. But it's also a story of innovation and a willingness to take risks to achieve something that has never been done before. His leadership at NVIDIA has been absolutely crucial and is one of the single most important factors in the company's success. If it weren't for his willingness to take bold risks, the company he leads and loves wouldn't be where it is today. As the age of AI continues, Jensen Huang's company will be there to deliver the hardware making it all possible, with him showing no signs of slowing down.

NVIDIA is no longer 30 days away from going out of business, but if there is trouble brewing on the horizon, Jensen Huang is ready. He himself said it best in 2010: “I waited tables. I’m prepared for adversity.”

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

Mobile

)

)

)