)

)

)

Company research3 Apr 2023

12 Boring Businesses With Strong Track Records

To get great or stable returns, you don't necessarily need to be on the hunt for the "next big thing."

When ants overrun the kitchen or a restaurant faces pests that could shut its doors overnight, both turn to a name they recognize. For more than a century, the name has often been Orkin, or one of the many local brands now integrated into the Rollins portfolio. This is the story of how a rat-poison salesman, two brothers from the Appalachian foothills, and a century of disciplined deal-making produced one of the most consistent businesses in America.

Wayne Rollins, born in 1912, and his younger brother John, born in 1916, were raised near Ringgold, Georgia, a small town in the Appalachian foothills not far from Chattanooga. Their father ran a small farm, and when a stroke disabled him in 1928, the boys took on much of the work.

But neither stayed in agriculture for long. Wayne went to work at a local textile mill in Chattanooga and later at a munitions factory during the Second World War. The years left him with an aversion to debt and waste, and a habit of reading every set of monthly financials line by line, something he would carry with him for the rest of his life.

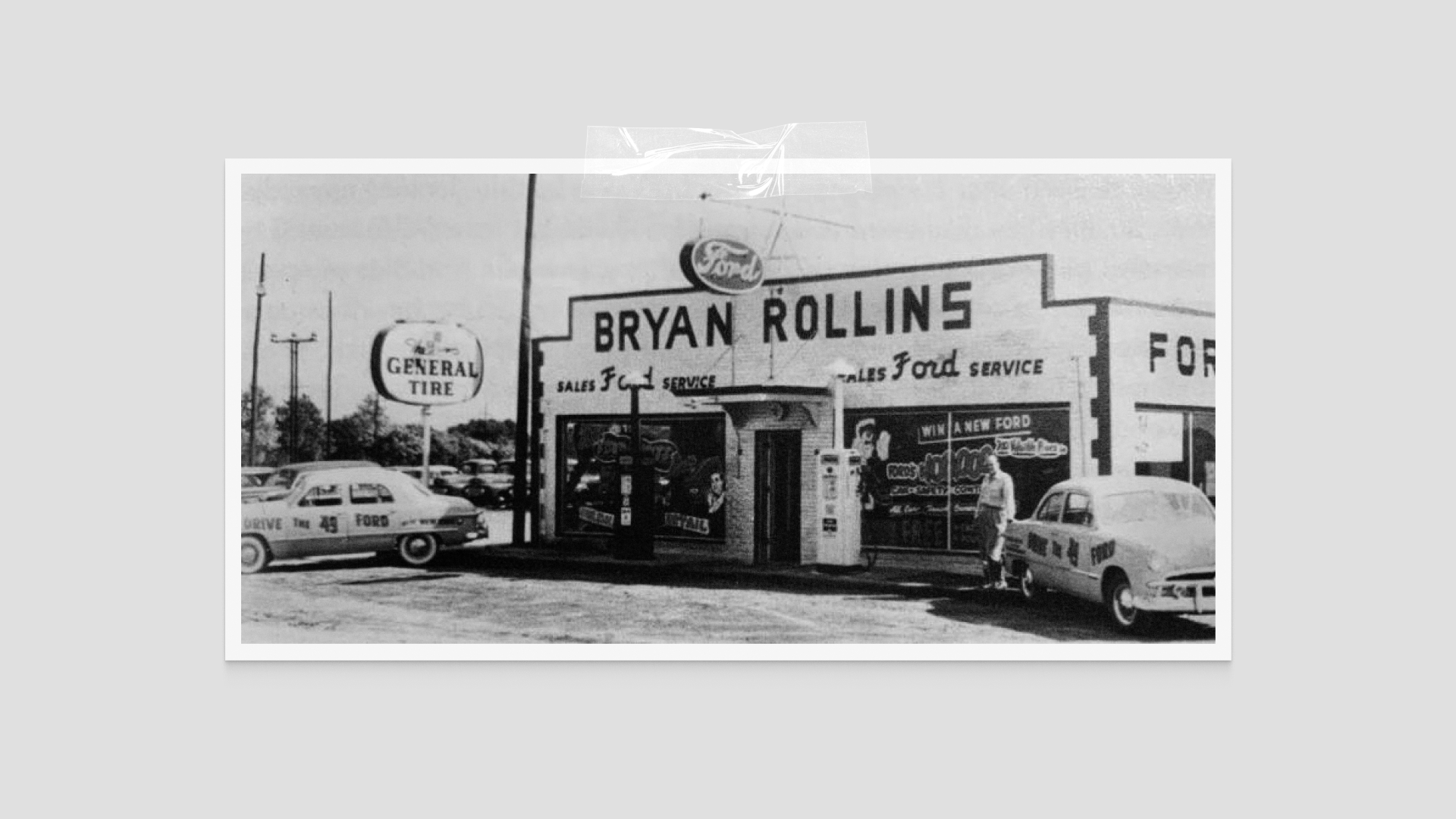

John was the more outgoing of the two. Where Wayne was cautious, John didn't mind taking on risk and trying something new. Having moved to Delaware, he opened a Ford dealership together with his friend Dory Bryan that, thanks to his talent for car sales, quickly expanded beyond the state into Maryland and Virginia.

In 1947, Wayne moved to Delaware to join the dealership business. Selling cars paid well, but advertising the dealerships was expensive, and Wayne saw a way to bring those costly operations in-house. In 1948, the brothers bought WRAD, a radio station in Radford, Virginia, for a small sum by broadcasting industry standards. The logic was simple: John's dealerships generated the cash, the station ran their ads at low cost, and any revenue from outside advertisers was profit on top. They called the parent partnership Rollins Broadcasting.

Wayne ran the business. He was a careful manager, a believer in low fixed costs and tight cash management, and more often than not erred on the side of caution. These instincts proved well-suited to local broadcasting, where margins were thin, and discipline mattered above all else. Over the following decade, the brothers added stations one by one, before moving into television in 1956. By 1960, they owned six radio stations and three television stations spread across the eastern United States.

In 1961, Rollins Broadcasting went public on the American Stock Exchange. That same year, the brothers bought the Tribble Advertising Company of Texas, which gave them a foothold in outdoor advertising and the start of what would become a national billboard business. They also began moving into cable television in markets across the South.

The strategy, to the extent there was one, looked a lot like the conglomerate model that would become commonplace in American business during the 1960s. In broad strokes: acquire companies that generated cash, run them better than the previous owners had, and use the proceeds to fund the next. But Wayne, who set the overall direction, narrowed it to a specific kind of business. He wanted companies that were well established, likely to still be around in twenty years, and that did something so basic nobody would think to disrupt it.

In 1963, Wayne began looking at a much larger company based in Atlanta. Orkin Exterminating, the dominant pest control business in the South, was for sale. The asking price was around $62 million, nearly seven times Rollins Broadcasting's annual revenue. On paper, the deal looked impossible. Wayne wanted to do it anyway.

But why? The strategy of acquiring smaller companies and improving them at the margins had worked well so far, so why take such an uncharacteristically large bet? To answer that, we need to look at what Orkin actually was and how it had come to be for sale.

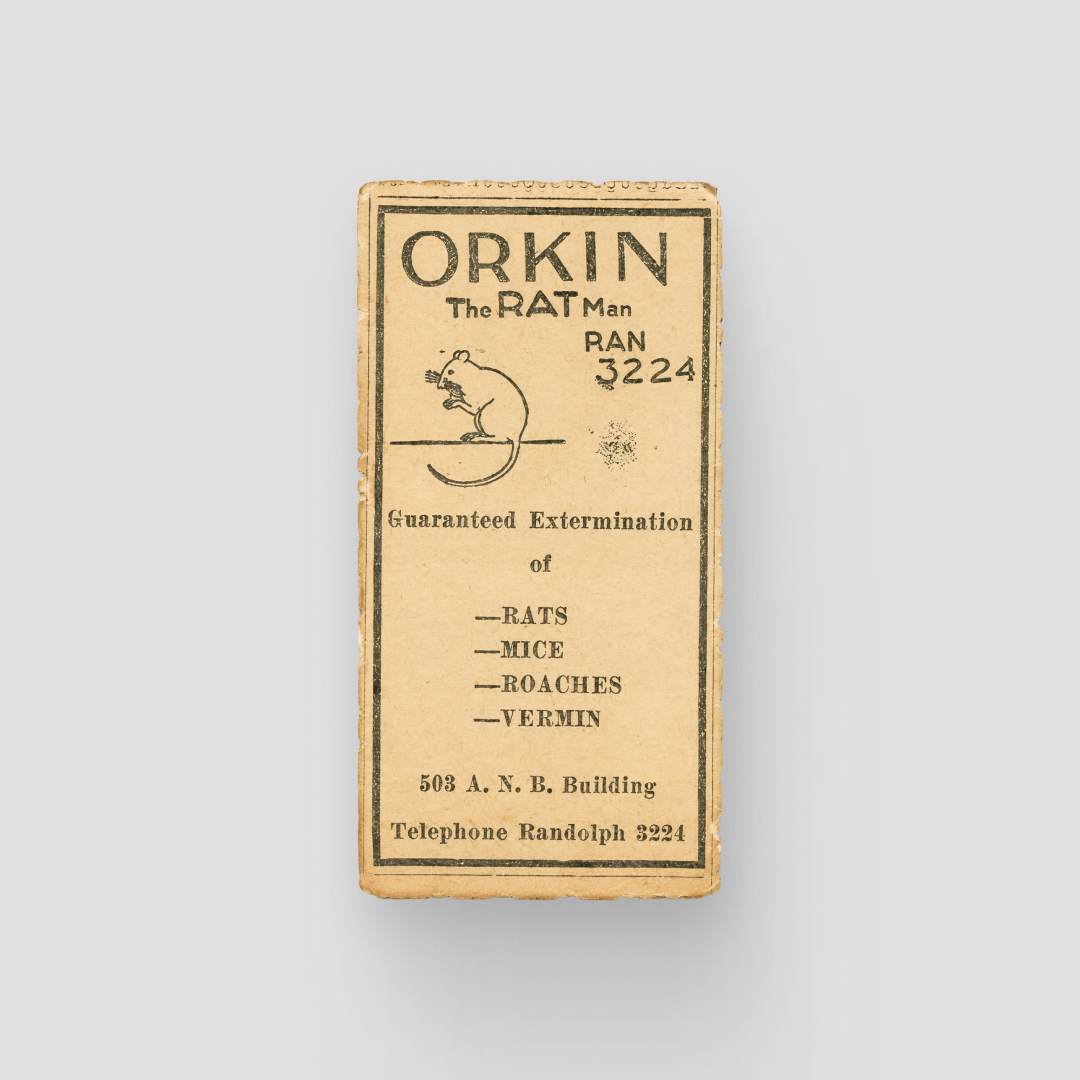

Orkin's founder, Otto Orkin, was born in 1885 in present-day Latvia, then part of the Russian Empire, to a Jewish family that immigrated to the United States when he was a small child. The Orkins settled on a farm in eastern Pennsylvania, and Otto's job as a boy was to keep rats out of the family's grain stores and away from their animals. He took to the work with obsessive focus, watching the rats for hours, noting where they nested and what they ate, and experimenting with different bait formulations.

At fourteen, he borrowed fifty cents from his parents, bought arsenic in bulk from a local apothecary, and started selling rat poison door to door. He kept careful records of which farms used his products and how they fared, refining his formula over time. By 1909, he had moved south to Richmond, Virginia, where he set up an office in a boarding house and began calling himself Otto Orkin “the Rat Man.”

The business grew through the 1910s as Orkin expanded into cockroaches, bedbugs, and termites. Along the way, he realized that the real opportunity was not in selling poison to homeowners, but in selling them service contracts. A bottle of poison was a one-time sale, and because his formulas worked, there was no follow-on revenue until the next infestation, if one ever came. Recurring annual inspections solved that problem, positioning the company for its next wave of growth throughout the 1920s.

In 1925, Otto moved the operation to Atlanta. With no major exterminator in the city at the time, the company captured much of the market almost overnight. He renamed the business Orkin Exterminating – a somewhat more professional label than "the Rat Man" – commissioned the diamond-shaped logo that the company still uses, and set about expanding across the South. By the end of the 1930s, Orkin had branches in every state in the southeastern U.S.

The outbreak of the Second World War brought a wave of military contracts for the company. Treating everything from armament factories to barracks, Orkin worked on more than 150 military installations and emerged from the war with a national footprint.

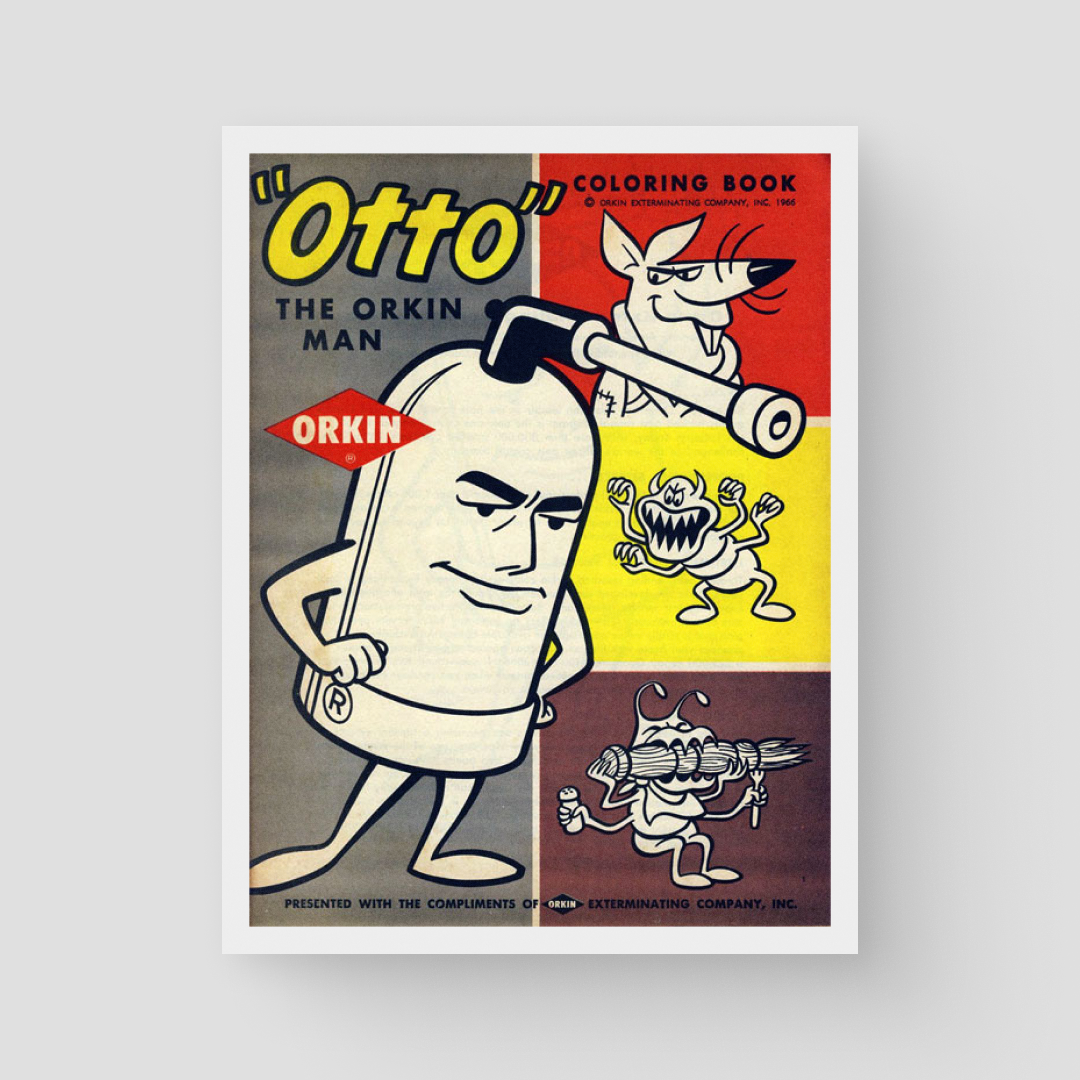

In the 1950s, Orkin became one of the first service businesses in the country to advertise heavily on television. The animated mascot introduced in those commercials, a singing spray can called Otto the Orkin Man, would later evolve into the live-action Orkin Man. By the time a homeowner discovered roaches in the kitchen, the jingle had been playing on their television for years, and they knew precisely who they were gonna call.

But despite success and its nationwide brand status, the company was by this point a family business in open conflict. Otto had handed operations to his sons, who disagreed about strategy, about money, and eventually about Otto himself. At one point, they had their father committed to a mental institution, a move he successfully challenged in court before securing his release.

The legal and personal drama dragged on for years, and by 1963, the family was ready to sell. The company was still thriving, but a sale seemed the only way to end the conflict. The asking price reflected the size and quality of the business; the willingness to sell at all reflected the exhaustion of the people running it.

Rollins Broadcasting's revenues were a fraction of Orkin's price tag, the cash on the balance sheet was not remotely sufficient, and conventional bank financing would not stretch nearly far enough. The only way to do the deal was to borrow against Orkin's own future cash flows, which is precisely what Wayne arranged to do. Business Week would later compare the acquisition to Jonah swallowing the whale.

Working through John's connections in Delaware, the brothers secured backing from Chase Manhattan Bank and Prudential Insurance Company, negotiating a structure that was groundbreaking at the time. The lenders agreed to underwrite the bulk of the purchase price on the strength of Orkin's expected earnings rather than the assets it owned, with the Rollins family putting up a comparatively small amount of equity and retaining majority control of the combined entity. The transaction closed in 1964 at $62.4 million, generally regarded as the first leveraged buyout in American history.

For Wayne, the LBO framing mattered less than the operational opportunity it opened up. He had quietly come to believe that pest control was a better business than broadcasting. The contracts were recurring, customers rarely shopped on price, and the service was essentially impossible to substitute. Orkin had built the routes, the brand, and the dispatch infrastructure to deliver that service nationally, but it had not, in Wayne's view, been managed with much rigor. He intended to fix that.

In the months after the acquisition, Wayne sent Rollins managers into Orkin's branch offices to apply the same playbook he had developed in radio: tighter cost controls, formal advertising programs, standardized pricing, and centralized procurement. By 1966, the company was operating from roughly a thousand offices, and the residential customer base, which Wayne saw as the most critical revenue source, was on track to quadruple over the following years.

The Orkin deal also set the template for almost everything Rollins would do afterward. Look for family-owned service companies in the southern states. Pay a price that looks expensive against historical earnings but reasonable against future cash flows. Keep the existing brand and field operations more or less intact, and apply central marketing, financial controls, and route optimization.

In 1965, with the company's interests no longer reflected by the broadcasting name, Rollins Broadcasting became Rollins, Inc. Three years later, the company moved its listing from the American Stock Exchange to the New York Stock Exchange. Throughout this period, Wayne Rollins kept acquiring businesses. Some of the purchases made obvious sense alongside pest control, while others were less obvious.

Rollins entered the residential security business, bought a lawn care company, and added a maid service. It became a major operator of cable television franchises in Massachusetts and Rhode Island. It continued to expand its outdoor billboard business, and in 1973, it added a small oilfield services business that over the following decade grew into a meaningful operation in its own right.

Wayne ran all of this with his trademark southern conservatism. He flew commercial, ate at modest restaurants when traveling, and was famously suspicious of consultants. By this point, the operations had grown so large that he needed to delegate, but he still read every set of monthly financials line by line. He was also, by then, training his sons, Randall and Gary, as his successors. Randall, his oldest, took over as president in 1975 while Wayne stayed on as chairman and chief executive.

By the early 1980s, the stock market had largely fallen out of love with conglomerates, as investors shifted from rewarding diversification to favoring focus. The Rollins family had been thinking along similar lines. The company had grown so large and sprawling, with pest control and oilfield work sitting alongside everything from billboard space in Mexico City to maid services in South Carolina, that running it as a single business had become increasingly difficult.

In 1984, the company split into three separately listed entities. Rollins Communications inherited the broadcasting, billboard, and cable operations; RPC Energy Services took the oilfield assets; and Rollins, Inc. kept Orkin and the rest of the pest control portfolio, along with a few smaller residential services.

Wayne stayed at the top of Rollins, Inc. as chairman and CEO. Randall took the lead role at RPC Energy Services as chairman and CEO, while also serving as president and COO of Rollins Communications before it was sold in 1986.

The split of the three businesses received immediate validation, and increasingly, Rollins, Inc. earned the recognition the family had understood it deserved for years: a company that visited the same houses and restaurants every month, billing modest sums for an essential service, was a vehicle for compounding capital in a way few businesses in any sector could match.

Wayne Rollins died in 1991, and Randall took over as chief executive and chairman of Rollins, Inc. Gary, who had been working his way up through Orkin since the late 1960s, became president and chief operating officer, and in 2001, succeeded his brother as chief executive. He would hold the position for more than two decades.

If the first phase of the company's life had been about building a conglomerate, and the second phase about breaking one up, the third phase, which began with Gary Rollins's run as CEO, was about consistency and focus. The strategy was simple, the execution slow and calculated.

The core remained Orkin and the steady organic growth of that business, which in a fragmented industry largely meant taking market share over time. Alongside that expansion, Rollins steadily acquired smaller competitors at sensible multiples and integrated them into its platform, replicating the formula on a national scale while reinvesting the cash flow into both future acquisitions and centralized operations. None of this generated headlines or earned praise for innovation, but for Rollins, it proved enormously effective. We'll return to this in greater detail later, because this operating model remains largely intact today.

The acquisition spree was steady, and to understand its scale and velocity, it's worth pausing on a few landmark deals from the first two decades of the new millennium. One of the most consequential came in 2004 with the purchase of Western Pest Services, a regional operator based in New Jersey. It was the first major company that Rollins did not absorb into the Orkin brand. Western had strong commercial relationships in markets where Orkin was weaker, and keeping its branding intact set the precedent for what would later become a portfolio of "specialty brands" operating alongside the flagship.

The Industrial Fumigant Company, a commercial specialist in food processing facilities, came next, followed by the country's third-largest residential pest manager, HomeTeam Pest Defense. Valued at around $137 million, HomeTeam would be the largest deal in the company's history for the next ten years. Going into the 2010s, the acquisitions continued.

Throughout the decade, Rollins picked up regional operators that deepened its presence in California, the Southeast, and Western Australia, along with wildlife-removal specialists that opened up an entirely new service line. The deals also grew larger over time. Northwest Exterminating, a Georgia-based operator acquired in 2017, became the biggest purchase since HomeTeam. In 2019, Rollins acquired one of the largest independent pest control companies in the country, Clark Pest Control, for more than $400 million. This was then followed by Fox Pest Control in 2023 at $350 million, a door-to-door operator with more than $120 million in annual revenue.

While none of these deals transformed the business as Orkin had done half a century earlier, taken together, they redrew the map of the North American pest control industry.

By the time Gary Rollins stepped down as CEO in 2022, the company had posted revenue growth in every year of his tenure, including through the 2008 financial crisis and the 2020 pandemic. When he passed the reins to his successor, Jerry E. Gahlhoff Jr., Rollins held roughly 24% of the North American market, the largest share of any operator in the industry.

The company is well positioned financially and operationally. We have a proven management team, leading brands and a very strong culture. I'm extremely confident in the future of Rollins.— Gary Rollins, 2022

Put yourself in the position of a homeowner who finds a wasp nest in the attic, or a restaurant owner facing the constant reality of an unexpected visit from a health inspector. In both cases, the choice of who to turn to often lands in a brand you recognize and trust.

That simple and universal need is the foundation on which Rollins has built one of the most consistent and resilient businesses in American services. While few consumers recognize the Rollins name itself, many know the pest and termite control brands within its portfolio, or at least have seen their trucks on neighborhood streets.

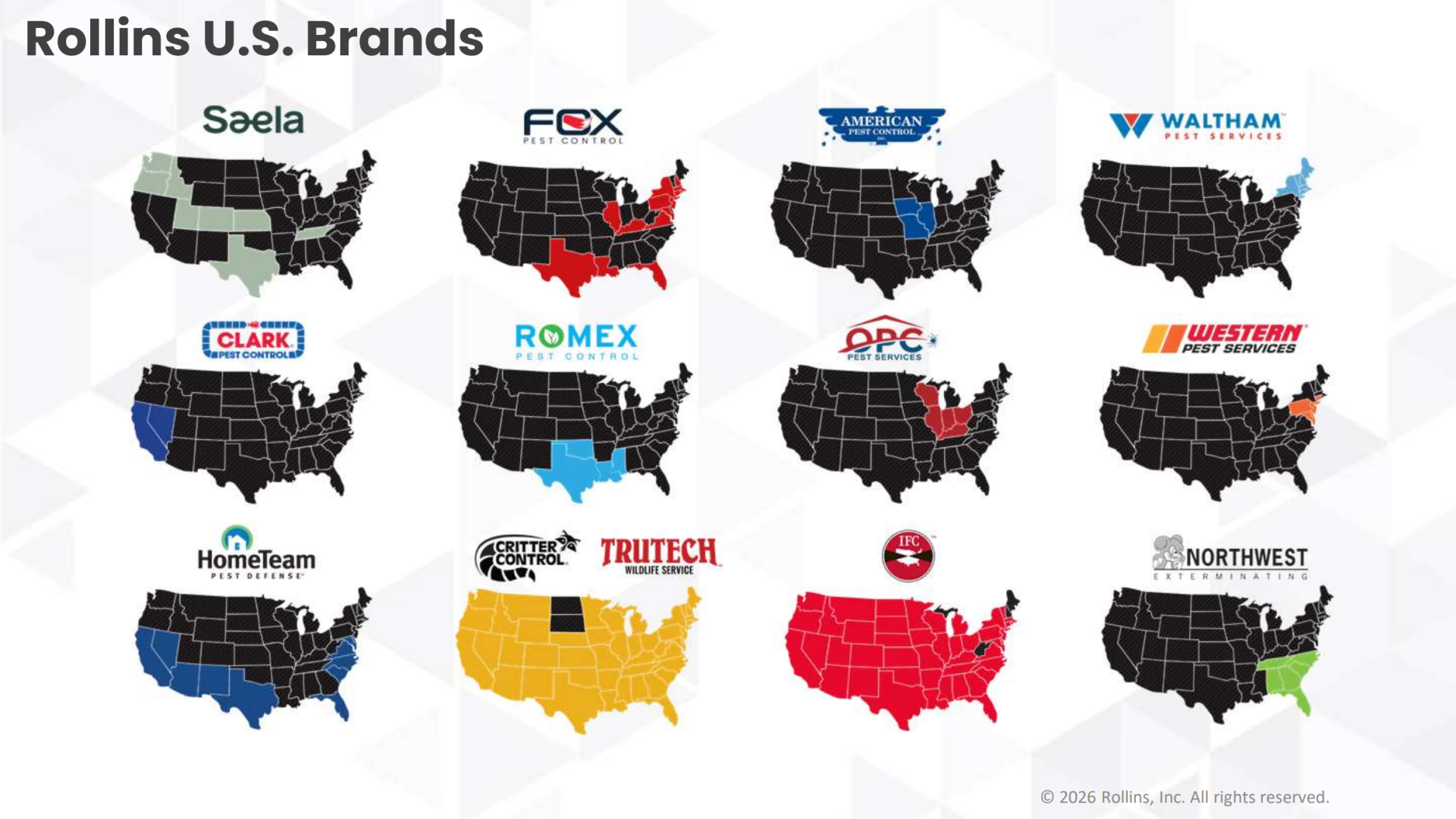

As of 2025, Rollins serves more than two million residential and commercial customers through over 800 company-owned and franchised locations across roughly 70 countries. At the center of the portfolio sits Orkin, still the company's flagship and best-known brand. Around it is a broad collection of regional businesses, with deep roots in their local markets, built through decades of acquisitions.

The industry they operate in is large, fragmented, and favorable to scaled operators. Pest control requires relatively little capital to start, which keeps barriers to entry low and has led to tens of thousands of small operators across the U.S., most of them family-owned and deeply local. Rollins' major competitors with nationwide operations include Rentokil, which operates across a much broader service footprint beyond pest control, along with Anticimex and Ecolab.

Together, they represent the only operators with scale comparable to Rollins. But the industry's long tail of regional and local players ensures fragmentation remains its defining structural feature and opportunity.

The pest control industry runs on two fundamentally different types of demand: residential and commercial. On the residential side, a homeowner calls because ants have taken over the kitchen or because mosquitoes make the backyard intolerable during summer.

The triggers vary, but the underlying need is consistent and rarely resolves itself. Compared with commercial pest control, residential demand is more evenly split between one-time jobs and recurring services, but remains a constant in everyday life across geographies, income levels, and economic cycles.

Commercial pest control operates differently. Hotels, restaurants, healthcare facilities, and food processors all depend on meeting health and safety standards, and those standards depend on passing inspections. Pest control is therefore not discretionary spending, but an operational requirement. The consequences of failure extend far beyond a fine, as a documented pest issue damages a brand's reputation, disrupts operations, and in some cases can threaten the business itself.

Together, these customer dynamics help explain the industry's resilience. Rats, termites, cockroaches, and other pests don't disappear during recessions or periods of weaker consumer spending. For Rollins, roughly 75% of revenue comes from recurring services, while much of the remainder is still highly predictable.

The fragmented nature of the industry, combined with steady demand, creates an advantage for the brands customers already know and trust. When a homeowner searches for pest control, they are usually looking for a company they recognize, one they believe will show up on time, solve the problem properly, and stand behind the work if something goes wrong. A reputation built over decades often matters more than aggressive marketing spend and justifies the premium pricing.

For commercial customers, where the stakes are higher, credibility becomes even more important. With 125 years of operating history, Orkin is the clearest example of this at a national scale, with its status as one of the most recognized names in residential services in the U.S. That position was not built through low prices, but through decades of consistent service, reinforcing customer trust over time.

The same dynamic exists throughout the broader Rollins portfolio at the regional and local level. Rollins recognized early that trust in pest control is often highly local, and as we've been over, its acquisition strategy has long reflected that understanding.

A regional brand that has operated under the same name for decades can hold the same kind of trust within its market that Orkin holds nationally. When a homeowner in suburban Atlanta calls Northwest Exterminating, it is often because a neighbor used Northwest before them, or because they have noticed its trucks parked around city streets for years. That trust is built slowly through consistent service and is difficult for a new entrant to replicate, regardless of price.

Rollins has spent decades assembling a portfolio of these local brands. Many of the acquired businesses keep the names, relationships, and reputations that made them successful, while Rollins provides the shared infrastructure behind them: technology, finance, purchasing, training, and regulatory support. That combination of local trust and centralized scale sits at the core of the company's strategy.

What we bring to the table that maybe some others don't bring to the table is the opportunity to keep their people intact, take care of their people and take care of their brand.— Kenneth Krause, Rollins CFO

In an industry this fragmented, acquisitions have become a permanent part of Rollins' operating model. The company targets roughly 2-3% annual revenue growth from acquisitions, a goal it has consistently exceeded through a steady stream of deals. While most of its acquisitions are small tuck-ins, adding local operators acquired for a few million dollars and folded into an existing branch network, others are more substantial.

Over the past decade, Rollins has completed an average of 32 acquisitions per year, ranging from 23 to 44 depending on the size and nature of the transactions. To exemplify, in 2025, Rollins completed 26 acquisitions. While this was below its historical average, the year included the $200 million acquisition of Saela Pest Control, the 23rd-largest pest management company in the U.S. Altogether, those 26 deals added $139 million in revenue, compared with $96 million from the 44 acquisitions completed the year before.

)

The opportunity stems directly from the structure of the industry itself. Many pest control businesses in this fragmented industry are family-owned and have been built over decades. As founders approach retirement and face succession questions, Rollins has spent years positioning itself as the buyer those owners want to sell to. Rollins CFO Kenneth Krause explained the company's positioning at the Stifel 2024 Cross Sector Insight Conference:

"The thing that we do different at Rollins that maybe you don't see as often at other companies is the relationships that we have across the industry. [...] We're seeing opportunities flow from the ground up. So [our managers] know these businesses, and they've known these businesses for a long period of time and they know how they're built."

Many sellers approach Rollins directly because of the company's reputation as an acquirer. Krause continued:

"It hasn't been difficult for us to find those opportunities. And oftentimes, people come to us because they know our reputation for acquiring. We take care of people, we take care of brands, where there's a value in the brand, we're going to make sure that brand stays intact. And so people sell to us because they know they can still live in that community. Because the people that they employed previously are being taken care of."

That credibility has been built over decades. Many members of Rollins' leadership team joined the company through acquisitions themselves, having previously worked at businesses Rollins acquired earlier in their careers. Having experienced the process from both sides shapes how the company approaches sellers, communicates its intentions, and maintains a steady pipeline of opportunities across the industry.

Beyond culture and strategic fit, Rollins applies strict financial criteria to acquisitions. Deals must support organic growth and meet benchmarks for customer retention metrics, which the company treats as a key indicator of business quality. Acquired businesses are also expected to support margin expansion, contribute to earnings in year one, and maintain or improve Rollins' strong free cash flow profile.

The highest hurdle is return on invested capital, where acquisitions are expected to generate ROIC above the company's cost of capital within three years. That expectation across 30-plus deals annually requires both buying at the right prices and integration execution. Rollins has spent decades building the infrastructure to do both consistently.

Larger platform acquisitions with established local recognition are typically preserved and operated as standalone subsidiaries. Stanford Phillips, who leads Rollins' U.S. brands and joined Rollins when Northwest (the company his grandparents founded) was acquired, described the philosophy from personal experience at the Investor Day 2026:

“When you're the one being acquired, it's personal. So we kept asking, what will this feel like for our teammates on Monday morning? That became our North Star, and it's the same lens we use today when Rollins welcomes a new company into the family. What we learned through that process changed the way I think about acquisitions forever. The very things that we were trying to protect, culture, teammates, local reputation and the brand were the exact reasons Rollins wanted to acquire Northwest.”

Smaller tuck-in acquisitions are handled differently. Operators without meaningful standalone brands are folded into whichever Rollins subsidiary already operates in that geography, whether Orkin, Northwest, or another regional brand. Technicians move onto Rollins' systems and operating standards, with smaller operators integrated quickly and larger tuck-ins often going through a temporary co-branding period before the original name is retired.

What remains consistent across both approaches is the integration of the underlying infrastructure. Finance, IT, procurement, training, and compliance all move onto Rollins' shared services platform. Central to that process is BOSS, the company's proprietary operating system that standardizes routing, scheduling, service tracking, and payments across the portfolio. Dedicated internal teams manage each migration, allowing Rollins to integrate acquisitions with a level of consistency that few serial acquirers achieve.

A recent example of the effectiveness of its acquisition model is Northwest Exterminating. Since being acquired in 2017, the business has roughly quadrupled its revenue and completed 17 acquisitions of its own. Today, Northwest operates as a smaller version of Rollins, acquiring and integrating local operators across the Southeast using the same playbook that brought it into the company.

Rollins is fundamentally a service business. It does not manufacture the chemicals or equipment used in its treatments. Innovation happens earlier in the value chain, at the product companies and research institutions developing the solutions Rollins technicians are trained to apply.

What Rollins sells is the service itself: the labor, expertise, and reliability of solving the problem correctly and consistently. Behind that workforce sits a research and quality assurance layer of more than 200 certified entomologists, who support technicians across everything from termites and bed bugs to rodents, mosquitoes, and wildlife intrusions.

In 2025, Rollins generated $3.76 billion in revenue across three core service lines: residential, commercial, and termite & ancillary. But not every brand in the portfolio participates equally across all three. Orkin, Clark, Northwest, Fox, and Saela operate as full-service brands spanning residential, commercial, and termite work, while others focus on narrower niches. HomeTeam specializes in termite pretreatment for homebuilders, Critter Control and TruTech focus on wildlife removal, and IFC concentrates on commercial fumigation. Together, the portfolio covers nearly the full range of services the industry demands.

While the U.S. remains the clear center of the business, Rollins also operates internationally across roughly 70 countries through company-owned operations in Canada, Australia, the United Kingdom, and Singapore, as well as through the Orkin franchise program elsewhere. International operations account for approximately 7% of total revenue.

Although international growth has at times outpaced the domestic business, the U.S. operation remains the company's primary growth engine, and we'll now cover it in greater detail across its three core service offerings.

)

Residential is Rollins' largest service line, accounting for 45% of revenue and growing organically by 5% in 2025. The customer base spans both one-time treatments for specific infestations and homeowners on recurring service plans covering general pest prevention throughout the year. Of the three lines, residential is the most weather-sensitive, with pest activity peaking in spring and summer and driving higher demand for new contracts and one-time treatments during the second and third quarters.

Commercial represents 33% of revenue and grew organically by 7.6% in 2025. Beyond its strong growth, it is also the company's most resilient service offering, where customers pay to protect both their regulatory standing and brand reputation, making demand highly price-inelastic.

The customer base includes hotels, restaurants, food processors, healthcare facilities, logistics operators, and retailers, all sharing a common characteristic: pest control is an essential compliance requirement. These businesses need to pass inspections, meet health and safety standards, and avoid reputational damage.

Several of Rollins' largest commercial relationships are national accounts, where a single contract covers locations across the country. These customers are supported through InSite, a proprietary platform that gives them visibility into service history, compliance documentation, and pest activity across all sites. For these customers, the operational risk of switching providers more often than not outweighs the cost of the service itself.

Its final core service line, termite & ancillary, contributed 21% of revenue and was the fastest-growing of the three, with 9.9% organic growth in 2025. In recent years, the bundled streams of termite & ancillary's organic growth have consistently run in the low-to-mid double digits.

Termite protection operates differently from the scheduled prevention model common in residential pest control. It begins with an upfront treatment, whether a liquid barrier, baiting system, or wood application, and is followed by annual renewals that maintain warranties and monitoring systems. Those renewals carry attractive margins because the incremental cost of maintaining an existing installation is relatively low.

Ancillary services grow through a different dynamic. A technician already visiting a customer for routine pest control may notice moisture damage under the floorboards or signs of a rodent entry point in the attic. That observation becomes a conversation, leading to a standalone project: crawlspace encapsulation, insulation installation, exclusion work, or wildlife removal. These jobs are completed separately from the pest control relationship, and they tend to be significantly larger in value. The average ancillary ticket is more than ten times the annual value of a standard residential subscription.

Today, ancillary services remain concentrated primarily within the Orkin brand. That leaves much of the customer base across Northwest, Fox, Saela, and Rollins' other brands largely untapped. Rollins' target in the near term is 20% annual ancillary growth, driven primarily by expanding these services across the broader portfolio.

Across all three service offerings and throughout its portfolio of brands, Rollins is built on a resilient recurring revenue foundation shaped by decades of long-term customer relationships. Kenneth Krause explained the importance of that model at Investor Day 2026:

“75% of our business is recurring, and that creates a predictable base of revenue and the opportunity to form valuable long-term relationships with our customers. The average customer life in our residential business is 4 to 5 years. And for commercial, it's even longer. The acquisition cost of a customer is incurred once and the revenue and value is realized over many years. This combination provides exceptional returns and stability.”

Commercial is almost entirely contract-driven, built on long-term relationships with businesses whose regulatory obligations make continuous pest control non-negotiable. Additionally, while the ancillary portion of termite & ancillary is reactive by nature, the termite portion tends to be sticky, with ongoing monitoring and bond renewal programs keeping customers engaged year after year.

As of 2025, Rollins reports that recurring and ancillary services together represent over 80% of revenue, with one-time work making up the remaining share of the total. Ancillary is not broken out separately, but is implied to be a mid-single-digit percentage of the total. The 75% recurring-only figure is not broken down at the service level, but the composition can be reasonably inferred based on the above assumptions.

Working back from these, residential recurring revenue is likely higher than many would assume. While the category may appear reactive and centered around one-time calls, the core residential offering is built around scheduled subscription services that keep customers on regular treatment cycles. Based on the broader revenue mix, residential recurring likely falls somewhere in the 60-70% range.

That total recurring base reinforces Rollins' acquisition strategy. Every acquired company brings an existing customer base that immediately contributes to the broader revenue foundation. Beyond integrating infrastructure, Rollins actively shares best practices across its brands to improve retention and customer economics over time. CEO Jerry E. Gahlhoff, Jr. gave an example at the Q1 2026 earnings call:

“When we acquired Fox three years ago, their customer retention was what I would call normal-ish. They have partnered with the HomeTeam brand who has some best-in-class retention. And over the last three years have moved their residential retention by 5 percentage points. That's a big movement over a few year period of time. So that demonstrates to us that there's always room for improvement, always opportunity to get better.”

As exemplified, Fox has introduced door-to-door tactics to HomeTeam, Western is leveraging Orkin's call center tools and processes, and HomeTeam is passing qualified wildlife leads to Critter Control and TruTech. Rollins screens acquisitions explicitly to avoid diluting retention metrics across the portfolio, and where acquired brands fall short, it imports best practices from stronger performers. The aforementioned cross-selling opportunity within ancillary services beyond Orkin remains one of the clearest untapped levers across the portfolio.

We are a recession-resilient business. We have delivered 25 years of consecutive growth. We're coming up on our 100th consecutive quarter of revenue growth. Let me say that again, 100 straight quarters of revenue growth.— Kenneth Krause

The numbers that result from everything described above are, in a word, consistent. While not yet at the centurion milestone referenced by Krause, Rollins is steadily approaching it. In 2025, the company recorded its 24th consecutive year of revenue growth and, as of Q1 2026, its 98th consecutive quarter of revenue growth. Through recessions, inflation cycles, and a global pandemic, revenue has grown without interruption. Revenue reached $3.76 billion in 2025, up 11% for the year, with approximately 7% organic growth and the remainder contributed by acquisitions.

Rollins has several growth drivers that together explain the consistency of its top line. Beyond the acquisition target of 2-3% annual revenue contribution, the deeper penetration of recurring services, and the ancillary cross-sell opportunity, organic growth comes from several additional sources. One such driver is annual price increases, something the company's brand positioning and customer retention have historically made relatively straightforward to implement. Kenneth Krause explains at the Baird 55th Annual Global Industrial Conference:

“When we think about the pricing in our services, we start with the base rate. The base rate for us is consumer price inflation. And then we add a layer on top of that because we believe, and our customers tell us that this service is essential. It's highly valued, and they're willing to pay a premium for the service above the level of CPI.”

However, the larger opportunity is simply continued penetration within a market that remains far from saturated. An estimated 80% of U.S. homeowners still don't use professional pest control, leaving substantial room for growth as more households continue adopting these services over time. Commercial also remains an attractive growth area, supported by compliance-driven demand and the continued expansion of national account relationships. Importantly, none of these drivers depends on the others to work, which is part of what makes the growth profile so durable.

"We execute with great discipline, and we don't need to have any single opportunity, which puts us in a very enviable spot. We have a playbook that's working and we continue to see opportunities to execute this strategy across an expansive opportunity set."

– Kenneth Krause, Investor Day 2026 (sourced through Quartr Pro).

The capital-light nature of Rollins' service model allows revenue to translate efficiently into cash flow. Free cash flow has grown at a 15% CAGR from 2015 to 2025, and now sits at $650 million. Over the same period, FCF margin has expanded from approximately 10.6% of revenue in 2015 to 17.3% in 2025, driven by the operating leverage of the model and the company's ability to spread costs across a growing revenue base as the portfolio scales.

Management deploys that cash across three primary channels in what it describes as a balanced and disciplined framework. Dividends and M&A each account for roughly 40% of capital allocation. Although management targets acquisitions to contribute roughly 2-3% annual revenue growth, the contribution has been closer to 4% over the past three years as Rollins has used its balance sheet more actively, with flexibility from its revolving credit facility. Share repurchases make up the remainder and are deployed opportunistically.

Behind Rollins' consistency sits a detail that is easy to overlook in a company of this size: the Rollins family still owns approximately 40% of the shares. Gary Rollins led the company for decades as CEO before becoming Executive Chairman in 2020 and, as of January 2025, Executive Chairman Emeritus and board director. While Rollins has been led by an outside CEO since 2022 for the first time in its history, the family's influence continues to shape the culture and long-term orientation of the business.

Approaching 100 consecutive quarters of revenue growth is not a coincidence, but the product of a company that has been run, for most of its life, as if it intends to follow the same path for the next 25 years.

)

From Otto "the Rat Man" Orkin to a portfolio of regional brands serving more than two million customers, Rollins has spent a century proving how much can be built on a single, unglamorous idea that pests don't go away, and that customers return. Three generations of family stewardship kept the playbook intact: buy selectively, preserve the local names, and let the routes do the compounding. Nearing 100 quarters of unbroken revenue growth later, when the wasp nest appears or the inspector knocks, the answer is still a Rollins company.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)