)

)

)

Business philosophy5 May 2025

Greg Abel: Succeeding Warren Buffett at Berkshire Hathaway

After decades working with Warren Buffett and Charlie Munger, Greg Abel was named Buffett’s successor as he steps down in late 2025.

Warren Buffett is arguably the most iconic investor of all time. He’s mostly known for his long-term-oriented investment approach, with a prominent focus on businesses with strong competitive advantages, led by honest people and great capital allocators.

During the Buffett Partnership years (1957-1970), which was the predecessor to Berkshire Hathaway, Warren wrote several letters to his shareholders which contain timeless wisdom on business building, long-term thinking, incentives, investing, and more.

Get curated quality company deep dives every other week.

1960: My continual objective in managing partnership funds is to achieve a long-term performance record superior to that of the Industrial Average. I believe this Average, over a period of years, will more or less parallel the results of leading investment companies. Unless we do achieve this superior performance there is no reason for existence of the partnerships. However, I have pointed out that any superior record which we might accomplish should not be expected to be evidenced by a relatively constant advantage in performance compared to the Average. Rather it is likely that if such an advantage is achieved, it will be through better-than-average performance in stable or declining markets and average, or perhaps even poorer- than-average performance in rising markets. I would consider a year in which we declined 15% and the Average 30% to be much superior to a year when both we and the Average advanced 20%. Over a period of time there are going to be good and bad years; there is nothing to be gained by getting enthused or depressed about the sequence in which they occur. [...] One year is far too short a period to form any kind of an opinion as to investment performance, and measurements based upon six months become even more unreliable. One factor that has caused some reluctance on my part to write semi-annual letters is the fear that partners may begin to think in terms of short-term performance which can be most misleading. My own thinking is much more geared to five year performance, preferably with tests of relative results in both strong and weak markets.

1960: In the event of losses, there will be no carry back against amounts previously credited to me as general partner. Although there will be a carry-forward against future excess earnings. My wife and I will have the largest single investment in the new partnership, probably about one-sixth of total partnership assets, and thereby a greater dollar stake in losses than any other partner or family group, I am inserting a provision in the partnership agreement which will prohibit the purchase by me or my family of any marketable securities. In other words, the new partnership will represent my entire investment operation in marketable securities, so that my results will have to be directly proportional to yours, subject to the advantage I obtain if we do better than 6%.

1961: We usually have fairly large positions (5% to 10% of our total assets) in each of five or six generals, with smaller positions in another ten or fifteen. Sometimes these work out very fast; many times they take years. It is difficult at the time of purchase to know any specific reason why they should appreciate in price. However, because of this lack of glamour or anything pending which might create immediate favorable market action, they are available at very cheap prices. A lot of value can be obtained for the price paid. This substantial excess of value creates a comfortable margin of safety in each transaction. This individual margin of safety, coupled with a diversity of commitments creates a most attractive package of safety and appreciation potential. Over the years our timing of purchases has been considerably better than our timing of sales. We do not go into these generals with the idea of getting the last nickel, but are usually quite content selling out at some intermediate level between our purchase price and what we regard as fair value to a private owner.

1962: To some extent, we have converted the assets from the manufacturing business which has been a poor business, to a business which we think is a good business – securities. By buying assets at a bargain price, we don't need to pull any rabbits out of a hat to get extremely good percentage gains. This is the cornerstone of our investment philosophy. Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives good results. The better sales will be the frosting on the cake. It should be pointed out that Dempster last year was 100% an asset conversion problem and therefore, completely unaffected by the stock market and tremendously affected by our success with the assets.

[...] I am not in the business of predicting general stock market or business fluctuations. If you think I can do this, or think it is essential to an investment program, you should not be in the partnership. I cannot promise results to partners. What I can and do promise is that: a) Our investments will be chosen on the basis of value, not popularity. b) That we will attempt to bring risk of permanent capital loss (not short-term quotational loss) to an absolute minimum by obtaining a wide margin of safety in each commitment and a diversity of commitments; and c) My wife, children and I will have virtually our entire net worth invested in the partnership.

Further reading: Margin of Safety and what it means in investing.

1964: Truly conservative actions arise from intelligent hypotheses, correct facts, and sound reasoning. These qualities may lead to conventional acts, but there have been many times when they have led to unorthodoxy. In some corner of the world they are probably still holding regular meetings of the Flat Earth Society. We derive no comfort because important people, vocal people, or great numbers of people agree with us. Nor do we derive comfort if they don't. A public opinion poll is no substitute for thought. When we really sit back with a smile on our face is when we run into a situation we can understand, where the facts are ascertainable and clear, and the course of action obvious. In that case--whether conventional or unconventional – whether others agree or disagree – we feel we are progressing in a conservative manner.

1964: In the great majority of (potential stock market investments) we simply do not know enough about the industry or company to come to sensible judgments – in that situation we pass. An investment operation that depends on the ultimate buyer making a bum deal (in Wall Street they call this the "Bigger Fool Theory") is tenuous indeed. How much more satisfactory it is to buy at really bargain prices so that only an average disposition brings pleasant results.

1965: There is one thing of which I can assure you. If good performance of the fund is even a minor objective, any portfolio encompassing one hundred stocks (whether the manager is handling one thousand dollars or one billion dollars) is not being operated logically. Anyone owning such numbers of securities after presumably studying their investment merit (and I don't care how prestigious their labels) is following what I call the Noah School of Investing--two of everything. Such investors should be piloting arks. I am willing to concentrate quite heavily in what I believe to be the best investment opportunities recognizing very well that this may cause an occasional very sour year – one somewhat more sour, probably, than if I had diversified more. While this means our results will bounce around more, I think it also means that our long-term margin of superiority should be greater.

1966: [About diversification among high-quality stocks in many mutual funds of the period] Since, over a long term, "average experience" is likely to be good experience, there is nothing wrong with the typical investor utilizing this form of investment medium. I still prefer the iceberg approach toward investment disclosure. All of our investments usually appear undervalued to me – otherwise we wouldn't own them. We don't buy and sell stocks based upon what other people think the stock market is going to do (I never have an opinion) but rather upon what we think the company is going to do. Our investments are simply not aware that it takes 365 1/4 days for the earth to make it around the sun. [...] Let me again suggest two points: (1) the future has never been clear to me (give us a call when the next few months are obvious to you--or, for that matter, the next few hours); and, (2) no one ever seems to call after the market has gone up one hundred points to focus my attention on how unclear everything is, even though the view back in February doesn't look so clear in retrospect. If we start deciding, based on guesses or emotions, whether we will or won't participate in a business where we should have some long-run edge, we're in trouble. We will not sell our interests in businesses (stocks) when they are attractively priced just because some astrologer thinks the quotations may go lower even though such forecasts are obviously going to be right some of the time.

1967: Interestingly enough, although I consider myself to be primarily in the quantitative school, the really sensational ideas I have had over the years have been heavily weighted toward the qualitative side where I have had a "high-probability insight." This is what causes the cash register to really sing. However, it is an infrequent occurrence, as insights usually are. The really big money tends to be made by investors who are right on qualitative decisions but, at least in my opinion, the more sure money tends to be made on the obvious quantitative decisions. Statistical bargains have tended to disappear over the years. This may be due to the constant combing and re-combing of investments that has occurred during the past twenty years, without an economic convulsion such as that of the '30s to create a negative bias toward equities and spawn hundreds of new bargain securities.

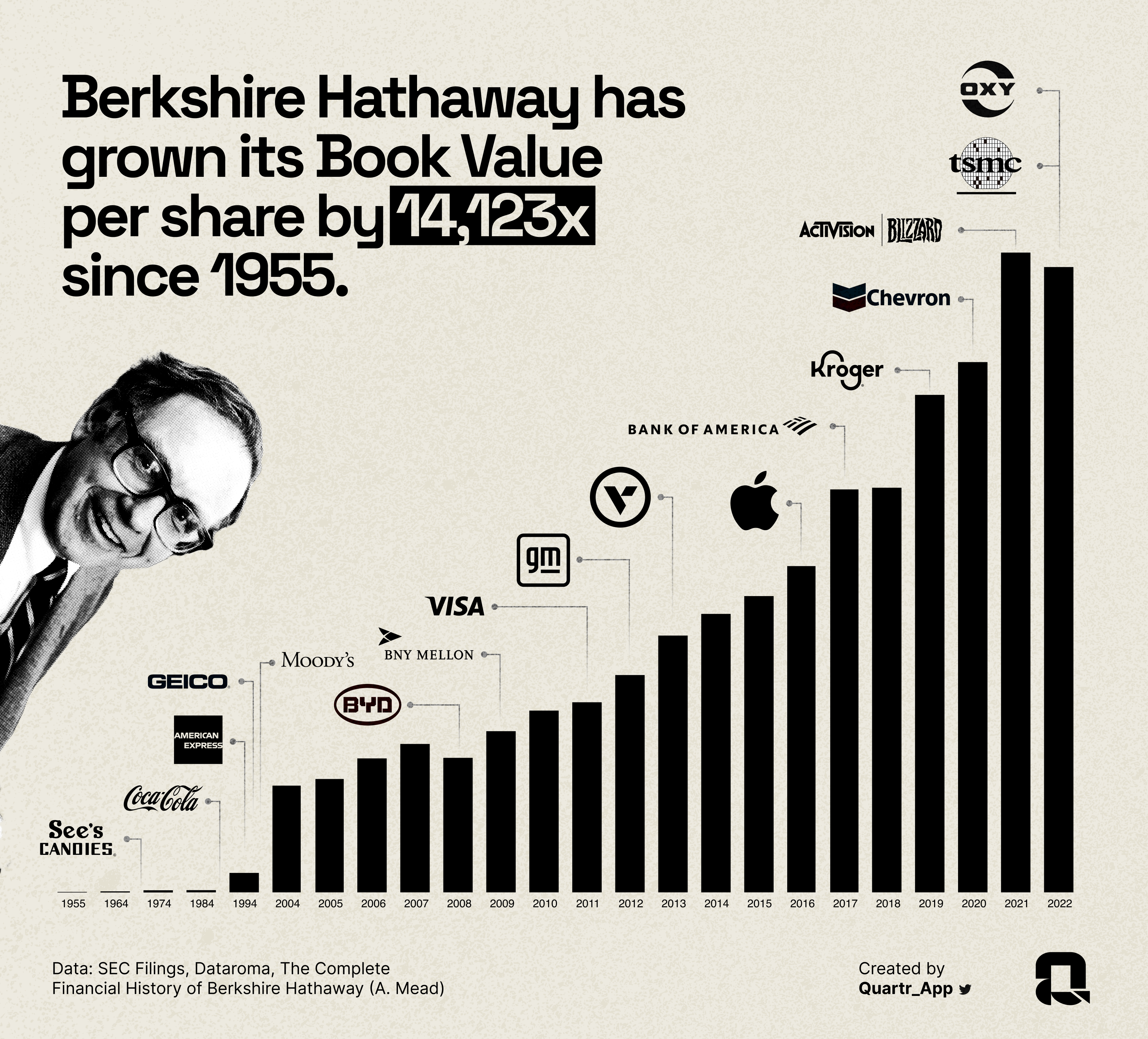

As a bonus we are adding our visual of Berkshire Hathaway’s insane compounding since 1955.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)

)