)

)

)

Edge22 Aug 2025

The Dilemma That Brought Down Kodak

Kodak helped invent digital photography but failed to embrace it. How the innovator's dilemma turned an icon into its own most famous casualty.

If you like reading Warren Buffet’s or Jeff Bezos’ shareholder letters, we are sure you will also like Mark Leonard’s. These letters present hands-on insights into the highly successful serial acquirer – Constellation Software Inc., originally founded by Mark in 1995, coupled with an initial investment of $25 million. Today the company is a world-leading conglomerate, acquiring and holding over 600 vertical market software (VMS) businesses. Below we present every shareholder letter he’s written.

Note that Mark Leonard wrote quarterly letters up until 2010, and later went on to only publish yearly ones.

Get curated quality company deep dives every other week.

As you will read in our interim MD&A, and as you can see in the table of appended Performance Metrics, our year over year Revenue growth rate slowed in Q1 2007 to 9%, a level that concerns us. The primary reason for the low growth in Revenue was a 1% contraction in Organic Revenue compared to the same period in 2006. One of the causes of declining Organic Revenue is outside of our control: U.S. housing starts declined approximately 28% in Q1 2007 compared to the same period in 2006, and that seems to have depressed spending amongst our homebuilding, construction and building products related customers. For the most part, we are pleased with how our homebuilding and related businesses have responded to the tougher operating environment. We continue to seek acquisition prospects among software companies that service these currently depressed markets.

In addition to the downturn in the homebuilding and related sectors, I believe that our Initiative program also contributed to the current decline in Organic Revenue Growth. In 2003, we instituted a program to forecast and track many of the larger Initiatives that were embedded in our Core businesses (we define Initiatives as significant Research & Development and Sales and Marketing projects). Our Operating Groups responded by increasing the amount of investment that they categorized as Initiatives (e.g. a 3 fold increase in 2005, and almost another 50% increase during 2006). Initially the associated Organic Revenue growth was strong. Several of the Initiatives became very successful. Others languished, and many of the worst Initiatives were terminated before they consumed significant amounts of capital. Examined on a portfolio basis (and to do that we still have to use forecasts, as payback in our business generally requires a 5-7 year time frame) we believe that our Initiatives have generated reasonable internal rates of return. However the Initiative returns have not been as attractive as those generated by our acquisitions. Accordingly, many of our Operating Groups have shifted more of their efforts to growth by acquisition, and have launched increasingly fewer new Initiatives over the last couple of years.

The response of our Operating Groups is what you’d like to see: Now that they have tools for tracking Initiative IRR’s, they are optimizing capital allocation by pursuing better returns in the acquisition market. In principle, there is nothing wrong with this shift. In practice, dramatically fewer Initiatives could eventually lead to a loss of market share. The software business has significant economies of scale, so conceding market share to well run competitors could lead to deteriorating economics. I’m not yet worried about our declining investment in Initiatives because I believe that it will be self-correcting. As we make fewer investments in new Initiatives, I’m confident that our remaining Initiatives will be the pick of the litter, and that they are likely to generate better returns. That will, in turn, encourage the Operating Groups to increase their investment in Initiatives. This cycle will take a while to play out, so I do not expect to see increased new Initiative investment for several quarters or even years.

Organic Growth can also be driven or diminished by acquisitions. When we acquire a rapidly growing company we boost Organic Growth. When we acquire an underperforming company that needs to have some of its unpromising lines of business reduced or removed, Organic Growth suffers. History suggests that we generally grow our acquired businesses, frequently providing additional products for them to sell into their installed base, and bringing our increased scale and best practices to bear upon their business. Occasionally however, the reduction of an acquired business to a profitable Core will leave us with a smaller, but usually more profitable business. Q1 2007 had several instances of declining revenues relating to acquired businesses. These acquisition-related declines in Organic Growth are usually transient, generally reversing after a year or less.

In addition to Organic Growth, we also grow our businesses via acquisition. Since inception Constellation has made 57 acquisitions. Software company acquisitions are becoming increasingly popular amongst both corporate and private equity buyers. As Corum, one of the most active M&A brokers in the software sector put it in their Q1 newsletter:

“Not since the dot-com peak has a year kicked off with as much merger and acquisition activity and value as in 2007”….. “Last year, 1,726 software companies were acquired, which is the highest number since 2000.”

We are currently experiencing intense competition in the large company acquisition market and are increasingly focusing upon those opportunities that are smaller or those that may not have a strong track record of positive cash flow. During 2006, we had a 42% increase in the number of “Non-Disclosure Agreements” that we signed with acquisition prospects, when compared to 2005. These NDA’s resulted in a >200% increase in the number of “Letters of Intent” that we submitted. My interpretation of this data is that we were working harder to see and bid on more of the available market. What did this work at the front end of the acquisition process produce? We had the same number of LOI’s signed back, and we ended up making only 10 acquisitions in 2006, down from the 12 that we made in the prior year. I think two factors were at play in generating the lower close rate in 2006: first, we went further afield (both geographically and strategically) looking for potential investments and second, we ran into more aggressive competition. The same pattern is apparent when we examine the M&A activity by dollar value instead of number of transactions.

In Q1 2007 we increased our M&A activity still further, almost doubling the number of NDA’s that we signed compared with Q1 2006, and achieving a new record high for the value of closed acquisitions in a single quarter. Despite the increased competition for acquisitions, we anticipate that our increased focus and discipline around the M&A process will allow us to generate a record year for acquisitions in ’07.

While we do not provide short-term forecasts, our objective is to generate 20% average annual Revenue growth per share between January 1, 2006 and December 31, 2010 (our “Planning Period”). During 2006 we exceeded this objective, generating 23% Revenue growth per share. In Q1, we fell far short of the objective, generating only 4% Revenue growth per share. Much of the shortfall in Q1 2007 was due to the 1% decline in Organic Revenue as compared to Q1 2006. Organic Revenue Growth is an important component of our overall Revenue growth objective, and we believe that it needs to average between 5% and 10% per annum for us to both achieve our objective and to have a healthy company. Management continue to believe that the Company will achieve both the Revenue growth per share objective and the Organic Growth targets for the Planning Period.

As is our practice, we have inserted below a table containing our quarterly Performance Metrics. In addition to the Organic Net Revenue Growth discussed above, the metrics that struck me were:

ROIC (Annualized) – 20%. We believe that this is an acceptable level, but would prefer to see higher levels if the low Organic Net Revenue Growth persisted.

Net Maintenance Growth (Y/Y) – 20%. We believe that (adjusted for cash and debt) maintenance revenues are the best indicator of Intrinsic Value. 20% is an acceptable increase, but any further slippage could be cause for concern.

I encourage you to study the Performance Metrics, the attrition data that we presented in the annual report, and the M&A activity data mentioned above. Don’t hesitate to pose any questions that you may have either on our quarterly conference call, or during the question period following our Annual General Meeting.

Mark Leonard, President

May 8, 2007

Q2 saw an improvement in our revenue growth rate: Organic Net Revenue growth in Q2 compared to the same period last year, recovered to 0.5%, and acquisitions accounted for the remaining 15% of year over year Net Revenue growth. Our homebuilding and building products related businesses experienced Organic Net Revenue declines. A turnaround in their growth prospects is not yet evident. Organic Net Revenue growth in a number of our other businesses more than offset those declines.

Constellation has an inherently resilient business. During Q2 Net Maintenance Revenue was $33.3 million, an increase of 24% from $26.9 million during the same period last year. Net Maintenance grew as a percent of Net Revenues, from 57% to 61%. Constellation has very low attrition rates and good margins associated with this revenue stream. We focus on growing Maintenance revenue because we believe that it is less volatile and more profitable than Professional Service and License revenues.

Constellation’s resilience is bolstered further by an employee compensation plan that insulates the company if performance lags, and rewards employees when the business is experiencing both high profits and rapid growth. Accrued bonuses (as a percentage of Net Revenues) in Q2 were 2% lower than in the comparable period last year. This accounted for a large portion of the 5% year over year increase in the EBITDA/Net Revenue margin (“EBITDA Margin”) during Q2.

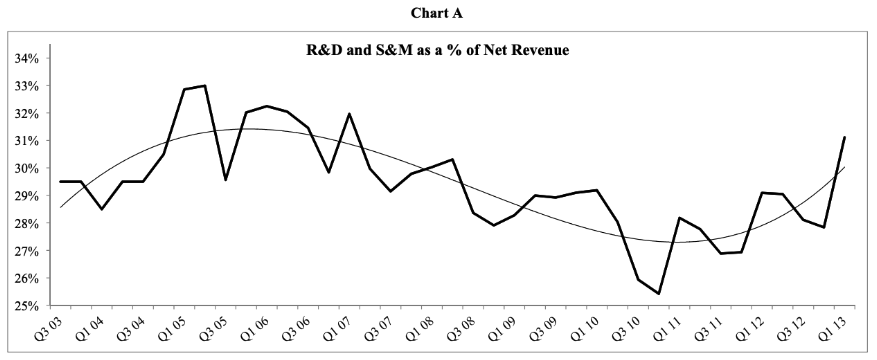

Much of the remaining increase in the Q2 EBITDA Margin was due to the decline in Research & Development and Sales & Marketing (“RDSM”) spending as a percentage of Net Revenues (29% in Q2 vs 32% in the prior comparable period). Is this decline in RDSM and the associated increase in EBITDA Margin good for long-term shareholders? Historically, a significant portion of RDSM expense has been invested in new Initiatives. We began tracking the returns from our Initiatives in 2004. Some of the Initiatives were not economic. We sought to improve our returns by culling poor Initiatives, and nurturing those that remained. My fear is that we over-reacted, causing a dearth of new Initiatives. Our challenge is to strike the right balance between Organic Revenue growth and profitability. My current preference would be to see a higher level of investment in attractive Initiatives. If we are successful at rebuilding our portfolio of Initiatives and continue to make acquisitions at the current rate, I anticipate that our EBITDA margins will trend down, but that our Organic growth will improve.

Inserted below is the table of Constellation performance metrics. In addition to the Organic growth, acquired growth, and Net Maintenance Revenue growth discussed above, the metrics that struck me this quarter were:

ROIC (Annualized) – 24%. This was a nice improvement from Q1, and was largely due to the expanding EBITDA Margin.

Tangible Net Assets (“TNA”)/ Net Revenues – (66)%. This was not a sterling performance. We pride ourselves in running negative TNA in our businesses. At minus 66% of Net Revenues, this quarter is amoung the highest levels of TNA that we have seen in the last 10 quarters. Some of the slippage stemmed from the way that our VCG investment is carried in our accounts. Some of the problem is poor management on our part. We are raising awareness of the slippage throughout the Company and are working to reduce it.

We made two small acquisitions in the second quarter, as well as a “strategic investment” in VCG Inc., a supplier of staffing and recruiting software solutions. Our preference is to acquire businesses in their entirety, and to own them forever. Occasionally, we have the opportunity to buy a piece of a good business with the prospect of eventually acquiring the rest. While that is by no means guaranteed in the case of VCG, we welcome the opportunity to get to know the business and its managers better, and hope that we will be able to increase our ownership over time.

We have an objective of generating average annual revenue growth per share and average annual EBITDA growth per share of at least 20% for the five year period ending December 31, 2010. I recently ran a screen of public companies with in excess of $50 million in revenues that met these criteria for the last 5 year period. I discovered that less than 1% of companies qualified. Picking through that list and pulling out anomalies, I was left with an even more exclusive list. We have set ourselves a very high bar.

Constellation experienced only 11% revenue growth per share during the first half of 2007. However, due to our strong revenue growth per share performance in 2006 (25%) and our continued optimism regarding acquired growth, we still believe that our five year revenue growth objective is achievable. Our performance to date against our EBITDA growth per share objective has exceeded our expectations. We continue to believe that we will be able to meet or exceed the EBITDA growth objective.

Mark Leonard, President

Net Revenue growth for Q3 2007 was 14%. This is short of our 20% growth objective for the 2006 to 2010 period. Despite having started the period well, with 4 quarters of Net Revenue growth in excess of 20%, we have fallen short of our objective for the last 3 quarters. The primary culprit has been Organic Net Revenue growth. During Q3 2007 our Organic Net Revenue growth rate improved: it increased from -1% in Q1, to 0% in Q2, and to 2% in Q3. While Organic growth appears to be recovering, it is not yet in the 5% to 10% range that we are targeting. Our homebuilding software businesses continued to experienced Organic Net Revenue declines. A recovery in their organic growth prospects is not imminent. We are impressed, however, with the way that the homebuilding team is managing their way through difficult times, and we will invest more capital with this team and in this vertical if good opportunities can be found. Our Government sector companies also had low Organic Net Revenue growth during the quarter. The reasons were several (and are discussed in some more detail in the MD&A), but appear to me to primarily be execution issues, not sector specific issues. We still believe that the Government sector business will eventually recover into the 5% to 10% organic growth rate range.

We have publicly reiterated our revenue growth objective each quarter, and we have a bonus plan that pays for growth. Those factors create a fierce temptation to stretch a bit and make some acquisitions that aren’t quite up to par. Counterbalancing hubris and greed, we have a good board and many long-term oriented managers. I believe that we have the judgment to maintain our investment discipline, and the humility to adjust our growth objectives downwards if we don’t think that they are achievable. I’m not yet ready to concede that our Net Revenue growth objective is not achievable, but if we have a couple of more quarters of sub-20% growth, achieving the objective will become very difficult.

We have fared much better with our EBITDA growth objective, far exceeding the minimum 20% year over year growth rate in the seven quarters to date. I believe Adjusted Net Income per share is a more useful measure of profitability growth. Quarterly Adjusted Net Income has grown an average of 49% (year over year comparisons) during the last 7 quarters, and we have issued no new shares. This rate of growth in Adjusted Net Income per share is not sustainable, particularly given our exposure to the increasing Canadian dollar, but the performance has been remarkable.

During Q3 2007, Net Maintenance Revenue was $34.5 million, an increase of 23% from $28.1 million during the same period last year. Those of you who follow our company closely know that we feel (assuming our cash & debt positions are stable), that Net Maintenance growth is a good proxy for the growth in Constellation’s intrinsic value.

Another performance benchmark that we look to, is the sum of ROIC and Organic Net Revenue Growth (“ROIC+OGr”). We believe that long term shareholders will generate a return on their Constellation shares that cannot exceed the sum of long term ROIC plus Organic Net Revenue Growth. We align compensation with this belief, basing our corporate bonus plan upon ROIC and Net Revenue Growth. For Q3, ROIC+OGr was 24%, a respectable number, but not up to the 30% that we have averaged over the last 11 quarters. Achieving even 24% ROIC+OGr is non-trivial. We believe that less than 10% of public companies have been able to achieve this level of performance for an extended period. Inserted below is a table of Constellation’s performance metrics.

We’ve added a new metric to the table - Adjusted Net Income Growth. As discussed, we believe that Adjusted Net Income Growth is a better proxy for the growth in profitability that accrues to shareholders, than EBITDA growth, since it also incorporates foreign exchange, tax and debt costs.

During the quarter we engaged in an attempt to help a shareholder sell one million of their Constellation shares. We spent money on lawyers and accountants, and chewed up management time, but didn’t manage to complete the offering. Our stock priced dropped by more than 10% after we announced the offering, but has since recovered somewhat. I believe that the intrinsic value of the business continued to increase at an attractive pace, despite the volatility in the stock price.

One of the useful things that we discovered during the marketing of the secondary offering, was that many of our existing shareholders wanted to speak with us. As we have mentioned previously, we would be pleased to meet with any Constellation shareholder at our offices. Please call me or John Billowits, our Chief Financial Officer, if you would like to arrange an appointment.

Mark Leonard, President

Net Revenue growth in Q4 2007 was 24% compared with the same period last year. This was a welcome increase after three consecutive quarters of sub-20% growth. While acquisitions played a huge part in our Net Revenue improvement, Organic growth also improved to 3% for the quarter. As you can see in the Table on the next page, Organic Net Revenue growth bottomed out in Q1 2007, and has been gradually increasing since then. During the quarter, the Organic growth varied dramatically between our private sector (-2%) and public sector (+7%) segments.

The conditions for our housing, building products, and construction related software businesses were the worst that we have experienced since we entered these markets. We see no imminent turnaround in view. While these businesses aren’t making as much money as during the prior year, they won customers at the expense of their competitors during 2007, and are bolstering their portfolio of add-on products. We continue to be confident in their long-term prospects.

Our public sector segment had a great quarter, with 28% Net Revenue Growth (of which 7% was Organic), and a handsome return on Invested Capital (25%). The public sector segment now constitutes approximately two thirds of our invested capital and revenues.

Net Maintenance revenue was a record $37.8 million during the quarter, up 28% from the comparable period in 2006. We have the preliminary data in from our annual attrition survey, and we were pleased that over half of the growth in Maintenance revenue was Organic last year. The details of the attrition survey will be in our annual report.

EBITA and EBITDA were down slightly in Q4 vs Q3. Despite that, they both saw significant growth (29% and 26% respectively) vs the same period last year. EBITA margin as a percentage of Net Revenues dropped to 16% in Q4 vs 19% in Q3. Factoring in how our bonus plan works, I believe that a 15% EBITA margin is a more realistic objective if we are generating 20% plus Net Revenue growth.

Our favourite single metric for measuring our corporate performance is the sum of ROIC and Organic Net Revenue Growth (“ROIC+OGr”). For Q4, ROIC+OGr was 25%.

Inserted below is a table of Constellation’s performance metrics. We’ve modified one of the metrics slightly – Tangible Net Assets / Net Revenues. Upon reflection, we decided that non-coupon carrying holdbacks (a form of acquisition financing even though they carry no explicit coupon) and Future Income Tax Assets (an intangible by any other name) were not appropriate to include in the Tangible Net Assets calculation. The table uses the new formula for all of the prior periods. While our performance with Tangible Net Assets continued to be acceptable, we could have done a better job of managing cash (which is excluded from the TNA / Net Revenues ratio) during the quarter. We believe that we had an excess of approximately $10 million of float in our operating entities during Q4. We have modified some incentives and encouraged the operating groups to send more of their cash to head office.

One of the areas where generally accepted accounting principles (“GAAP”) do a poor job of reflecting economic reality, is with goodwill and intangibles accounting. As managers we are at least partly to blame in that we tend to ignore these “expenses”, focusing on EBITA or EBITDA or “Adjusted” Net Income (which excludes Amortisation). The implicit assumption when you ignore Amortisation, is that the economic life of the asset is perpetual. In many instances (for our business) that assumption is correct. We are constantly “renovating” our software, adding to and replacing portions of it, and we provide the maintained product to our clients under perpetual support programs that we generally term “Software for Life”. Some of our products (and markets) won’t be as durable, and will gradually start to lose economic viability. I don’t think GAAP comes anywhere close to reflecting this spectrum and timing of outcomes. We do, however, have a couple of tools that we use in-house that can highlight the businesses that are 2 aging vs. those that continue to be revitalised. One crude indicator is a quarterly IRR calculation that we do on all acquisitions that we completed since 2004. IRR by its very nature requires forecasts, and hence is going to have subjectivity. Nevertheless, we try to beat the unwarranted optimism out of the forecasts, and as time passes, we can increasingly cross-reference history with forecasts. Right now, we only have one of those acquisitions (purchase price $1.2 million) that shows a less than 10% after tax IRR on the original investment, and one other (purchase price <$1 million), with an IRR between 10% and 20% after tax. All others exceed a 20% IRR.

The other mechanism that we use to potentially spot the “aging” assets is attrition. As I mentioned before we do a detailed review of attrition each year in the annual report, and in the upcoming one, we’ll try to give you some more comfort regarding the robustness of our portfolio of intangible economic assets.

I have no easy fix for GAAP, but we will try to highlight “impairments” as they become apparent, even if they have already been written off for GAAP purposes.

Recently there was a report of a massive (>30%) short position in our shares. Initially I was more amused than annoyed, thinking that an error had been made in the short report that would soon be corrected. Nevertheless, I touched base with our major shareholders, who told me that they knew nothing of such a short, and I did some math – soon determining that the reported short position exceeded the number of shares that had traded in our entire history as a public company. We probed some more, and found out that the short was reportedly due to a large off-exchange trade that failed to complete. We still are not to the bottom of the issue, but will provide a press release when we have more information.

On a more positive note, we are about to pay an $0.18 per share dividend, a 20% increase from the $0.15 per share paid last year.

The employee stock purchases for the Bonus program will commence in April. The anticipated volume of purchases will be approximately the same ($4.4 million) as last year, and may extend over several months.

When we took Constellation public we communicated management’s 5 year performance objectives for the company: i.e. to exceed 20% average annual Net Revenue and EBITDA growth per share for the period January 1, 2006 to December 31, 2010. During 2007, Net Revenues grew 16%, after having grown 27% in the prior year. 2007 saw wonderful but unsustainable EBITDA growth of 33%, after a terrific 31% growth year in 2006. With the first two years of the five year objectives under our belt, we continue to believe that the 5 year objectives are going to be challenging, but achievable.

Mark Leonard, President

March 5, 2008

I recently flew to the UK for business using an economy ticket. For those of you who have seen me (I’m 6’5”, and tip the non-metric scale at 280 lbs.) you know that this is a bit of a hardship. I can personally afford to fly business class, and I could probably justify having Constellation buy me a business class ticket, but I nearly always fly economy. I do this because there are several hundred Constellation employees flying every week, and we expect them to fly economy when they are spending Constellation’s money. The implication that I hope you are drawing, is that the standard we use when we spend our shareholders’ money is even more stringent than that which we use when we are spending our own.

This “Annual Report” is an example of that standard at work. Public companies are required by securities regulators to produce a variety of documents (Management Information Circular, Annual Information Form, Proxy, Quarterly MD&A, etc.) the contents of which are often formulaic and obscure but capture most of the key information that shareholders require. Companies nearly always augment these documents with attractive, multi-coloured annual reports replete with charts that demonstrate that their favourite metrics have performed well over the prior N periods. Most annual reports strike me as expensive yet superficial. In reducing our annual report to this “Letter to Shareholders”, I’m hoping that we’ll deliver a lot more bang for our shareholders’ buck. In it we will review our annual attrition data, expand upon “Amortisation” (a topic which we raised in the Q4 Letter to Shareholders), discuss Constellation’s evolving capital structure, and provide a few of the requisite charts of our favourite metrics.

Annual Attrition Survey: We believe that attrition is one of the most important measures of a software company’s health. If attrition is high, then customers are either moving to competitive products or are going out of business, neither of which bode well for the company. Each year we survey our operating groups, often on a product by product basis, to determine attrition. The data isn’t perfect, but we do reconcile it to our GAAP maintenance revenues, and we use it internally to judge the progress of our businesses. Despite its imperfections, we believe that this information provides shareholders with insight into our long-term prospects.

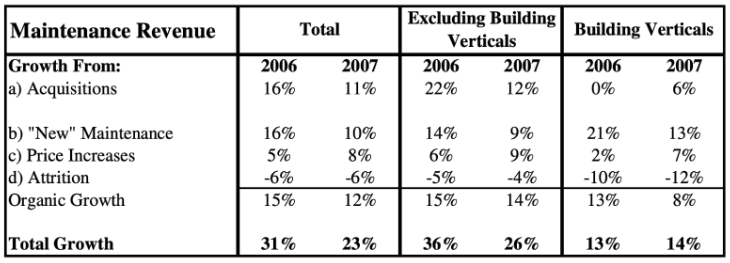

Attrition in 2007 was approximately 6%, the same as in 2006. This came as a bit of a surprise to me… I was expecting worse due to the downturn in the Homebuilding and Building Products related verticals (jointly “Building” verticals). As you can see in the table below, the attrition in the Building verticals accelerated from 10% in 2006 to 12% in 2007, while in the non-Building

verticals attrition decreased from 5% in 2006 to 4% in 2007. With or without the Building verticals included, we believe that Constellation’s attrition is low by software industry standards and reflects well upon our employees, our managers and our strategy.

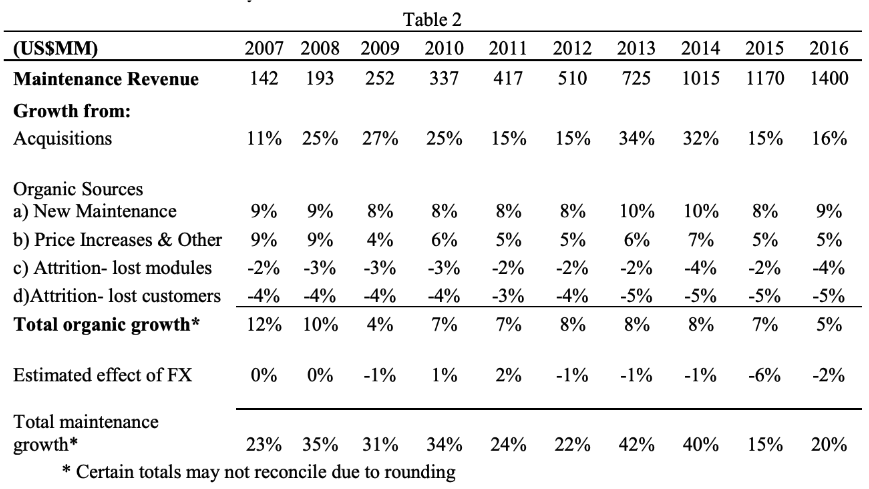

The table also demonstrates that Organic growth in maintenance has remained strong (at 12% in 2007), while acquired growth (11% during the year) was much lower than in 2006. We made a number of acquisitions at the end of 2007, so we expect acquired maintenance growth to rebound during 2008.

In total, maintenance revenues grew 23% to $142 million during 2007. They constituted 59% of our total revenues, up from 55% in 2006.

Amortisation: In the fourth quarter Letter to Shareholders we pointed out that the amortisation of acquired intangibles is the major difference between Adjusted Net Income and GAAP Net Income. Investors often ignore the GAAP amortisation of intangibles due to an implicit assumption that purchased software assets/businesses do not experience economic deterioration. This assumption is consistent with our strategy, but there are instances where it does not hold.

Of the more than 45 acquisitions that we have made in the last four years, we flagged two small acquisitions (jointly comprising intangible assets at the time of investment of less than $2.5 million) in the Q4 letter where we felt that purchased intangibles had suffered some economic impairment. The tool that we used to identify these impaired assets was the internal rate of return (“IRR”) that we are forecasting/experiencing for these acquisitions.

Another tool for identifying impairment is Organic maintenance revenue contraction. When maintenance revenue contraction has occurred, then there has almost certainly been impairment in the underlying intangible asset. At this time, we have two Building related acquisitions, with an aggregate original intangible value of approximately $6 million, that are experiencing significant organic contraction in their maintenance revenues. We believe that this is a temporary impairment – i.e. as the Building markets recover, so will their maintenance revenues. Time will tell, and we will update you if we believe that these intangible assets have suffered permanent impairment.

Neither acceptable forecast IRR’s nor Organic maintenance revenue growth alone are proof of unimpaired intangible assets: A business must have both an acceptable forecast IRR and Organic maintenance revenue growth to clearly have unimpaired intangible assets. It is worth wading through a couple of examples and how they would each measure economic earnings.

IRR can be high while maintenance contraction is also high if a business with a poor strategic position and/or a deteriorating market is being “milked out” (i.e. run to generate very rapid payback of the original investment). This would likely be the right strategy to pursue with such an asset. However, the right economic accounting to pursue, would be to amortise the goodwill against the income of the business over the relatively short economic life of that asset. You should not use “Adjusted Net Income” (i.e. Net Income plus Amortisation) when judging the economic earnings of a business such as this.

Similarly, IRR can be low while Organic maintenance is growing rapidly if a company is either investing irrationally in organic growth, or paying too much for acquisitions with high organic growth. At the margin, we would argue that the majority of multi-product software businesses over-invest in their Organic growth initiatives. This doesn’t give rise to misleading Net Income figures unless the companies are also capitalising R&D – which we do not do. If too high a price is paid for a growing acquisition, then there is going to be intangible asset impairment. GAAP often allows this impairment to be averaged out against a broader intangibles pool, or quickly amortised before the impairment is apparent (at which point GAAP ceases to care, since it has already been written off).

If it becomes evident that any of our Operating Groups are milking out a business, or have overpaid for acquisitions, we will provide Constellation’s shareholders with the historical cost of the intangibles that we purchased with that business, and we will reduce the Average Invested Capital that we report. For competitive reasons, we will not advertise the names of the businesses where impairment has occurred.

Capital Structure: Private Equity firms are finding it both more difficult and more expensive to raise debt capital. A year ago, when we competed for a good software business, private equity firms might have outbid us by 40%. Now, they are increasingly paying prices that we find attractive. Stock price multiples are also coming down, so “cheap equity” is no longer as commonly available to public acquirors. While strategic acquirors with good balance sheets are still active, they seem to be straying less into our markets. We believe that this is an attractive time for Constellation to be making acquisitions. Since the end of Q3 of 2007, we have invested approximately $45 million in new acquisitions, more than double our historical investment rate. Given the attractive valuations that we are seeing, we would like to continue to be able to invest at a rate that exceeds our ability to internally generate cash. We are negotiating with a syndicate of banks to increase our revolving line of credit to accommodate this. The Constellation board believes that using a prudent amount of debt is justified based upon our consistent record of revenue and earnings growth.

Our financial objective is to generate in excess of 20% average annual revenue and EBITDA growth per share for the period January 1, 2006 through December 31, 2010. The “per share” component of these objectives makes us very sensitive about issuing new equity. We would consider an equity issue if it gives us competitive advantage when we are buying a business: e.g. we occasionally offer long-term shareholders of good businesses the opportunity to “roll-over” their shares on a tax free basis for shares of Constellation. As Constellation becomes larger and more diversified, and if our track record of growth and profits continue, I can foresee some entrepreneurs opting for this type of transaction.

Our capital structure is evolving from the minimal use of debt to the consistent modest use of debt. This is due primarily to the current attractive environment for acquisitions rather than to a permanent commitment by either the board or management to maintain debt as a significant portion of our capital structure.

And, as promised, a few graphs are appended that illustrate our growing revenues, invested capital and earnings per share over the last few years. After looking them over, I hope you’ll join me in thanking the Constellation employees for producing another great year for shareholders.

We will be hosting the annual general meeting in early May. A number of our directors and officers will also be in attendance. We are all looking forward to answering any questions that you may have. I hope to see you there.

Mark Leonard, President

April 8, 2008

Q1 2008 benefited from a very weak comparable Q1 in 2007. Revenue increased 32%, Organic Net Revenue growth was 6%, Net Maintenance growth was 34%, and Adjusted Net Income growth was 62%. On a sequential basis (Q4 2007 vs Q1 2008) growth was more modest but still encouraging (revenue increased 11% and Adjusted Net Income increased 19%). Please note that we have changed the definition of Adjusted Net Income (see MD&A) in a way that has reduced the Adjusted Net Income for this quarter by $1.3 million vs what it would have been using the former definition. We believe the current definition provides a closer approximation of after tax cash profits.

Organic growth continued to improve despite deteriorating performance in our building related verticals. This was the fourth consecutive quarter of improving Organic Net Revenue growth. A table containing our quarterly Performance Metrics is appended. Our favourite single metric for measuring shareholder returns combines profitability and growth (ROIC + Organic Net Revenue growth). The combined metric was 32% (annualised) in Q1, a very handsome return for a business with such a low Tangible Net Asset (“TNA”) requirement. TNA/Net Revenue remained stable at -58% (-57% in Q1 of 2007). We were disappointed that we did not see more improvement in this metric, despite considerable efforts throughout the year. Building related verticals are exhibiting longer receivables, and some long-dated receivables that came along with recent acquisitions (against which we have provisions in the acquisition agreements, should they prove uncollectable) are the primary culprits.

We completed 3 acquisitions in Q1, but only a modest ($2.7 million) amount of capital was invested. Shortly after the end of the quarter, 3 further acquisitions were made for a total net cash investment of $11.4 million. This continues to be one of the best acquisition markets that we have seen in many years. In 2007 we signed 50% more Non Disclosure Agreements than we signed in 2006. These resulted in a 52% increase in the value of Letters of Intent that we issued, and a 65% increase in the value of the Letters of Intent that were signed back to us. 2008 promises to be an equally busy year. As you may have seen in our recent press release, we have increased our revolving line of credit to $105 million, so that we are in a position to take advantage of attractive acquisition opportunities when they are available.

I am often asked why Constellation takes minority interests in other public software companies. The answer is simple (value!), but it can be complicated by our investment horizon and by our requirement that the company have competent ownership.

Constellation’s objective is to be a perpetual owner of inherently attractive software businesses. Part of a perpetual owner’s job, is to make sure that energetic, intelligent and ethical general managers (“GM”) are running their businesses and that the GM’s are incented to enhance shareholder value over the very long term. It is trivial for an experienced GM to run a software company to generate high profitability and shrinking revenues. Far more challenging, is generating reasonable short term profits while continuing to grow revenues, in an industry where investment cycles often exceed 10 years. Understanding a GM’s performance as they make these long term trade-offs is the most difficult part of a perpetual owner’s job.

We have bought more than 70 private software businesses outright. On ten occasions, however, we have also participated in the purchase of significant minority positions in public software businesses. Usually these minority interests were purchased for less than their intrinsic value, and for far less per share than we would have had to pay for the entire business. While these purchases tend to be at the “value” end of our investment spectrum, they often carry incremental risk because we lack access to information concerning the long term trade-offs that the businesses are making. Even excellent managers of public companies are initially uncomfortable allowing us to join their boards to get access to this information, suspecting us of dire motives or a short-term orientation. We have the same objective when we buy a piece of a business as when we buy 100%, i.e. we want to be a great perpetual owner of an inherently attractive asset. If we are allowed to join a public company’s board, we offer to sign an agreement that will limit our ability to make an unsolicited take-over bid. This allows existing long-term shareholders of our public investees to continue to enjoy the benefits of ownership. For shareholders with similar objectives to ours, we believe that we are an exceptional coinvestor.

When boards reject our request for representation, we may resort to “shareholder democracy”, i.e. we may approach other shareholders to request that they support our quest for a board seat. Only as a last resort will we make an unsolicited bid for a company.

Our financial objective is to generate in excess of 20% average annual revenue and EBITDA growth per share for the period January 1, 2006 through December 31, 2010. We continue to believe that these objectives are attainable.

Mark Leonard, President

May 7th, 2008

Q2 was a good quarter for Constellation, particularly in light of the difficult economic environment. We achieved record levels of Adjusted EBITDA ($14 million) and Adjusted Net Income ($12 million), and 5% Organic Net Revenue growth.

In Q2 of 2006, Constellation became a public company. Net Revenue during that quarter was $47 million. Net Revenue in Q2 of this year was $71 million – a 23% compound annual growth rate since the IPO. While some of this growth was organic, the majority of it was acquired. We issued no new shares during the IPO nor have we issued any since then, so the intervening acquisitions were financed from our earnings (~$73 million), and borrowings/cash reductions (~$26 million).

Until recently, we had avoided using significant amounts of debt. Circumstances, however, may dictate a change in our capital structure. The economy is slow, credit and equity markets are in rough shape, and buyers for vertical market software businesses are increasingly scarce. Concurrently, and for some of the same reasons, quite a number of vertical market software businesses are for sale at attractive prices. We may not be the successful bidders for these assets, but if we are, we will almost certainly be increasing Constellation’s financial leverage. In support of our acquisition pursuits, we negotiated an increase in our revolving bank line to $105 million during Q2 and are currently in discussions with our lenders to further increase the size of this facility. We are also examining other financing alternatives.

Rapid acquired growth is not an imperative, it is a choice. For most of the last decade we struggled to find enough attractive acquisitions to consume our operating cash flows. We believe that the situation has now reversed, and we are sorely tempted to buy as many attractive vertical market software businesses as and while we can.

A table containing our quarterly Performance Metrics is appended. We have discussed the definitions and implications of the various metrics in previous letters to shareholders, and a glossary is also provided. This quarter, I was pleased with our performance across all of the metrics but wanted to draw your attention to one in particular. When economic times are tough, and bonuses are tied to financial performance, there’s a strong incentive for the managers of any business to aggressively recognise revenue. I believe that our people are largely inured to such temptations, but there’s a quick way to cross-check. Aggressive revenue recognition nearly always gives rise to an associated increase in accounts receivable and work in process. We should be able to see any such movements in our Tangible Net Assets/Net Revenue metric. In Q2 of 2008, this metric was -58%, down from -45% and -51% in Q2 of 2007 and 2006 respectively. This improvement over prior years suggests that, if anything, our businesses are being conservative about the earnings that they are reporting.

Mark Leonard, President

August 7th, 2008

In a diversified company like ours, you can usually point to some businesses that are stars and some that are not. I’m currently in the happy position of being able to commend the performance of all of our Operating Groups to shareholders. In Q3, some of our businesses recorded double digit organic growth and many of them produced record profits. Others continue to be profitable despite rending and perhaps long term change in their sectors. In aggregate, Constellation generated 7% organic Net Revenue growth in Q3, managed a further 28% acquired Net Revenue growth, produced record Adjusted EBITDA ($15.7 million) and Adjusted Net Income ($12.3 million), and invested more in acquisitions ($44 million) than in any previous quarter. You can’t judge the quality of this quarter’s acquisitions by this quarter’s profit, but after 85 acquisitions over a 13 year period, we seem to have developed a knack for acquiring fundamentally sound businesses at fair prices. While it’s comforting to revel in the Q3 results, I suspect that our Organic Growth will flag in 2009. Forecasters are calling for GNP contraction in North America. Constellation can’t hope to be immune, but we anticipate faring far better than most software companies due to our high and growing (34% growth in Q3) Net Maintenance Revenue.

Another metric worth bringing to your attention in the table below is Tangible Net Assets / Net Revenue. Our Operating Groups did an exceptional job of managing their working capital in an economic environment where many customers are trying to hang on to their cash a little bit longer. This improvement is overshadowed by the large amount of negative Tangible Net Assets that we acquired late in the quarter as a result of the Maximus acquisition. I anticipate that we will not be able to maintain the -84% Tangible Net Assets / Net Revenue ratio in the future, but we should see continued good performance on this metric. A glossary for our quarterly Performance Metrics is appended to this letter. I encourage you to refer back to previous letters for more extensive discussions of each of the metrics.

Because of the uncertainty in credit and equity markets, there are some great VMS investments to be had right now. We scooped up a big one this last quarter in the form of the Maximus assets. It consists of 3 good businesses, two of which came with very large uneconomic contracts. As we indicated when we announced the acquisition, the contingent liabilities associated with these contracts could exceed 50% of the purchase price. Contracts of this size and structure are unusual in our businesses (at least the way we run them). We factored these contracts into the price that we paid for these assets, and if we got it right, these 3 businesses will eventually generate good ROIC’s and contribute to our organic growth.

Having bought the Maximus assets and 16 other businesses this year, combined with our purchases of publicly traded shares of VMS companies and the pending takeover offer for Gladstone plc, we have deployed and committed approximately $94 million of capital. While we have also had record cash flows and profits, these commitments have largely tapped out our existing line of credit. I am leery about using short term financing for acquisitions, so we are exploring financing options: Either we slow down the pace of acquisitions and live within our cash flow from operations, or we raise long term financing, whether that be equity or debt flavoured. The capital markets are volatile right now, so I wouldn’t hazard a bet as to whether we will find the right investors. If we do, you can expect our acquisition pace in 2009 to continue… if not, it will slow. Irrespective of our acquisition prospects, I continue to be optimistic that our long term performance will be attractive.

Mark Leonard, President

November 6th, 2008

This quarter I’m using a reverse shaggy dog format for the Shareholder letter. Shaggy dog stories are wildly tangential tales that end with underwhelming and/or irrelevant punch lines. In my reverse shaggy dog story, we are going to start with the overwhelming punch line and then tell relevant tangential tales. To the extent that you take the time to follow my explanations of the impact this quarter of foreign exchange, employee bonus accruals, acquisition accounting, and organic growth, you’ll have an appropriate context in which to judge our remarkable Q4 results and make sensible assumptions about our future results.

In Q4 2008 Constellation had record Net Revenue per share and record Adjusted Net Income per share in the midst of the worst economic decline that most of us have ever seen. Compared to Q4 2007, revenue grew 49%, Net Revenue grew 47%, Adjusted EBITDA grew 111%, Adjusted Net Income grew 103%, and Net Income grew 142%. Meanwhile, the U.S. department of Commerce believes that GDP decreased at an annual rate of 6.2% in the quarter, calling out the “downturn in exports and a much larger decrease in equipment and software” for special attention. Why did Constellation do so well in such a difficult environment?

The facile answer is that we have robust businesses with inherently attractive economics run by good managers whose compensation is tightly aligned with that of shareholders. The more nuanced answer requires a deeper understanding of Constellation and its business model.

As many of you know (please refer to the 2008 annual MD&A for the details), we run Constellation with an unhedged structural currency mismatch. The vast majority of our revenues (81% in Q4 2008) are in US dollars, while a large portion of our expenses (23%) are in Canadian dollars. The Canadian dollar has appreciated in excess of 60% vs. the US dollar since early 2002, peaking above par in late 2007. Despite the adverse foreign exchange rate move during that period we maintained and grew our operating margins. Since the 2007 peak the Canadian dollar has dropped by more than 20%, settling in around an average rate of .8264 per US dollar in Q4 2008. We have benefited enormously from the recent collapse in the Canadian dollar. Some of those benefits are transient (relating to Canadian dollar liabilities on the balance sheet that have depreciated, such as accrued employee bonuses), while others could continue to help us operate with higher margins. In the future, assuming a geographical business mix and foreign exchange rates consistent with those we achieved in Q4 2008, we would expect operating margins to be approximately 3% higher than they would be if we were to operate at the average foreign exchange rates that prevailed throughout the first 9 months of 2008.

Employee bonuses were approximately 9.5% of Net Revenue in 2008. In Q4 2008 they amounted to only 7.9% of Net Revenue, despite the fact that both ROIC and Net Revenue Growth increased. Once again, the impact was primarily due to foreign exchange rates. The bonus accrual that was made for the first 9 months of 2008 was calculated using historical foreign exchange rates and required a multi-million dollar adjustment in Q4 2008 as a significant portion is in Canadian dollars. The Net Revenue Growth of 47% that was achieved in Q4 2008 is not sustainable. Nor is the ROIC of 35%. Hence with some confidence (and no little regret) we can predict that employee bonuses will be less than 9.5% of Net Revenues in 2009. This, however, does point out one of the attractive features of our bonus plan – when one of our businesses suffers a downturn, its costs are automatically trimmed due to lower bonuses. We saw this at the Homebuilders Operating Group in 2008: operating expenses per employee decreased 14% (mostly due to lower employee bonuses), while Adjusted EBITDA dropped 18%.

We don’t often spotlight an individual acquisition. Partly this is because we do a lot of them. In 2007 we made 17 acquisitions and in 2008 a further 21 - tracking them all publicly would be a sinecure for our auditors second only to IFRS. Partly it is because we don’t like sharing sensitive information with competitors. We were required by applicable securities laws to file a Business Acquisition Report (“BAR”) for our recent acquisition of certain assets and liabilities of Maximus Inc.’s Asset, Justice, and Education solutions businesses (“MAJES”), so the competitive reasons are less valid in this instance.

The BAR did, however, throw into question our sanity. Read literally, it suggests that we bought a business that had $72 million in revenues and lost $32 million pre tax in the year leading up to our acquisition. According to the BAR, the business also had a negative tangible net worth (excluding deferred income taxes) of $2 million. For this we paid $40 million. Clearly we had quite a different perception of these businesses than that depicted in the BAR. I’m pleased to refer you to the “selected financial information” for the MAJES businesses in our 2008 MD&A. The business generated $17 million in revenue during Q4 2008, $3 million of Adjusted EBITDA, $1 million of Net Income, and had a negative $1 million cash flow from operating activities. You need to understand the acquisition accounting to interpret this information.

The Asset Solutions business is performing well, but the Education and Justice businesses have their challenges. First and foremost among these are a number of what I have previously referred to as “uneconomic contracts”. Where we cannot reasonably estimate the effort to complete these contracts, we are using the “completed-contract” method to account for them. We have never used this accounting method before. It involves capitalising the contract revenues and expenses on the balance sheet until the contract is completed and then recognizing them in a lump sum. This tends to depress revenues vs. our normal (percent complete) revenue recognition methods, and can have a profound effect upon the bottom line. If at some stage we are able to estimate the cost to complete these contracts, and if we expect the contracts to generate losses, then we are allowed to take provisions against the estimated losses. Prior to that, we cannot recognise losses. Accounting aside, we have been able to make progress with most of the Education and Justice clients that were a source of concern. These situations may take years to resolve. We’ll keep you apprised of the financial performance of the MAJES businesses for a couple of years. You will be able to decide first-hand whether or not we effectively deployed a large chunk of capital on behalf of our shareholders.

Organic Net Revenue growth (“OGr”) came in at a 0% for Q4 2008, and 5% for 2008 as a whole. Compared to our long term objective of 5-10%, this is low. Compared to U.S. GDP, we are doing fine. There were a couple of mitigating factors. The appreciation of the US dollar vs. the Canadian dollar, the UK pound, and the Danish kroner shaved a couple of points off the OGr rate. I’m sensitive to the fact that our OGr historically benefited from currency shifts, so I don’t want to over-emphasize this point. The MAJES acquisition also took a couple of points off of our Q4 2008 OGr rate (we accounted for its run-rate revenues using the numbers in the BAR, which did not use completed-contract accounting). Incorporating these adjustments and a recent analysis we did of license bookings (which are slowing), its apparent to me that achieving organic growth in 2009 is going to be difficult. Some of our public businesses will grow, but the private sector businesses still anticipate significant organic decline.

I continue to be in the fortunate position of being able to commend the performance of all of our Operating Groups. I have confidence that their managers will protect the interests of our customers, shareholders and employees despite the distressing economic environment.

Mark Leonard, President

March 4th, 2009

Our Q1 2009 performance compared well with Q1 2008: revenue was up 32%, Adjusted EBITDA up 64%, and Adjusted Net Income up 51%. Sequential comparisons vs Q4 2008 along with a bit of digging reveal a less rosy picture: revenue down 1%, Adjusted EBITDA down 7%, and Adjusted Net Income down 11%. The drivers of this performance that strike me as worthy of highlighting include our Organic Net Revenue Growth rate (-5%), the Maximus Asset, Justice and Education (“MAJES”) acquisition which was completed in Q3 2008, our increased tax payments, and lastly, the Canadian dollar.

Organic Net Revenue Growth

Some of our businesses are more subject than others to a downturn in the economy. In Q1 2009, our Private Sector segment Net Revenue contracted 15% organically vs Q1 of 2008, while our Public Sector segment Net Revenue fared better (1% organic growth vs Q1 of 2008) for a combined Organic Net Revenue Growth of -5%. This is the worst Organic Net Revenue Growth that we have produced since we started keeping such records in 2001. Despite the occasional encouraging press release from real estate brokers, bankers and homebuilders to the contrary, we have yet to see any clear signs of a recovery in our private sector businesses. There is also little direct evidence of government stimulus spending trickling down to our public sector clients.

MAJES Acquisition

GAAP and even our own “Adjusted EBITDA” measure do a poor job of reflecting the current economics of the MAJES acquisition. In an investor’s shoes, I’d look at the cash purchase price ($35 million disbursed to date) and compare it with the cash produced ($1 million in the 6 months that we’ve owned the business). Not bad, but certainly not up to our long term expectations, and nowhere near as good as the reported six month Adjusted EBITDA ($8 million) and Net Income ($3 million) for these businesses would lead you to believe. There are several large contracts within MAJES that are cash flow negative, and until they are either completed or terminated by the customers, we don’t expect attractive returns from the acquisition. The MAJES acquisition also “helped” our TNA/Net Revenue ratio, contributing to a significant drop in the ratio in Q3 2008 and beyond. MAJES came with significant contract related liabilities but my sense is that the asset intensity of this business will eventually be similar to our other businesses. Excluding the MAJES acquisition, the TNA/Net Revenue ratio was down vs Q1 2008, which suggests that our businesses are continuing to practice conservative revenue recognition.

Taxes

We have had low tax rates during the last couple of years, but increasing profitability is driving them up. In Q1 2009 we provided for current taxes ($3.1 million) that are more than three times the amount provided for in Q1 2008. Taxes are inevitable, and despite our efforts to minimise them, we anticipate that our ratio of cash taxes to Adjusted Net Income will continue to increase during 2009.

Canadian Dollar

In the Q4 2008 letter to shareholders I chronicled how the Canadian dollar had affected our profitability during the last 7 years. The gist of the matter, is that with disproportionate expenses in Canadian dollars and revenues in US dollars, we run a fundamental and unhedged foreign exchange position. This hurt us for many years as the Canadian dollar appreciated vs the US dollar, but in the second half of 2008 as the Canadian dollar plummeted by over 20%, we benefited significantly. In Q1 2009 the average Canadian dollar vs US dollar exchange rate was .8054, down from an average rate of .8264 in Q4 2008. Of late the Canadian dollar has strengthened, and should it continue, we can expect leaner profit margins.

We had comforted ourselves in the last couple of quarters that poor organic growth for Constellation likely meant even worse performance for other vertical market software businesses, and hence we would see a number of good acquisition prospects. This hasn’t proved to be the case. Q1 2009 was a slow acquisition activity quarter for Constellation, with just one acquisition and no new signed letters of intent. Many owner-managers of healthy businesses seem to be waiting out the recession before selling, but I had expected some of the leveraged transactions of the last few years to come unraveled. To date, we have seen very few distressed asset sales. I’m still hopeful that lenders will lose patience with some private equity sponsored vertical market software businesses during the second half of the year culminating in some larger transactions. We are currently negotiating an increase in our credit line so that we can pursue large acquisitions.

The toughest challenge in the software business is intelligently trading off profitability and organic growth. Many entrepreneurs have a huge bias towards growth at the expense of profits. Most private equity owned software firms have the opposite bias. At Constellation we try to find an optimum position where incremental investment still generates good incremental long term returns. I think our managers and employees are doing a great job of maintaining profitability in a difficult economic environment, without curtailing our record Research & Development spending ($15 million in Q1).

I look forward to seeing those of you who are able to attend our Annual General Meeting on May 7th, 2009.

Mark Leonard, President

May 6th, 2009

We had record revenues in Q2 2009, topping $100 million in quarterly revenue for the first time. At 27%, our ROIC (Annualized) continues to be very good. Disappointment in the quarter stemmed primarily from our Organic Net Revenue growth of -4%. Our private sector businesses’ Q2 organic revenue growth was significantly negative (-14%) vs Q2 of last year, and the rate of organic revenue decline has not yet moderated. The public sector businesses have also seen slow organic revenue growth (4%), some of which was due to foreign exchange fluctuations, but a significant portion of the slow growth was due to lackluster bookings in the last couple of quarters.

The Maximus Asset Justice and Education solutions (“MAJES”) businesses that we acquired in Q3 of 2008 contributed significantly to revenue ($19 million), Adjusted EBITDA ($5.5 million) and cash flow from operating activities ($7.1 million) in Q2 2009. This was the first quarter where the MAJES cash flows suggest that the purchase price that we paid might be reasonable. It is still too early to congratulate ourselves, as contract penalties and/or contingent liabilities assumed as part of the acquisition could yet reverse the positive cash flows achieved to date.

During Q2 we completed one acquisition, and subsequent to quarter-end another four acquisitions closed. Total capital deployed for the five acquisitions was $8 million. Our cash flow exceeded the capital deployed on acquisitions, and our bank line was paid down by $17 million during Q2.

This quarter, John Billowits (CFO) and I visited with a large number of private equity (“PE”) firms that acquire software businesses. Our initial hope was that they might have some over-levered businesses to sell. We found that they had very few software businesses in financial difficulty. In fact, software businesses in general, whether PE owned or public, appear to have fared remarkably well during the recession. Their costs are largely headcount related, their revenues are largely recurring, and most of them have trimmed headcount in response to modest revenue contraction. Software Equity Group, LLC reported in their 2Q09 Software Industry Equity Report, that the median public software company EBITDA margin is at a four-year high. The good news is that most software businesses are resilient high return businesses. The bad news is that a large number of deep-pocketed PE organisations and well financed profitable public companies continue to compete with us for all of the larger acquisition opportunities.

At the time of our initial public offering we established an objective of generating in excess of 20% average annual revenue growth per share and EBITDA growth per share for the period January 1, 2006 through December 31, 2010. We continue to believe that the employees of Constellation will deliver this remarkable performance despite the current economic environment.

Mark Leonard, President

August 5th, 2009

Constellation had record revenues of $107 million in Q3 2009. EBITA was also at record levels ($22 million), as our businesses continued to manage expenses and margins well despite Organic Net Revenue Growth of minus 3%. We are forecasting much improved Organic Net Revenue Growth in the coming year, but not counting on it.

We had a flurry of acquisitions (i.e. 8) during Q3 2009, with capital deployed totalling in excess of $38 million. On November 2nd our Trapeze Operating Group acquired Continental Automotive AG’s Public Transit Solutions business (“PTS”). The PTS business will be a significant contributor to Net Revenue growth in Q4 and in 2010, but is unlikely to be a significant contributor to EBITA growth for quite some time.

Q3 Adjusted Net Income and ROIC (Annualized) at $15 million and 22% respectively, slipped markedly vs the last 3 quarters’ results. Foreign exchange losses ($2 million in Q3 2009 vs $0 million in Q3 2008) and current taxes ($5 million in Q3 2009 vs $2 million in Q3 2008) played a large role in these decreases.

The Maximus Asset Justice and Education solutions (“MAJES”) businesses that we acquired in Q3 of 2008 continued to generate strong cash flows from operating activities ($6 million in Q3 2009). As you’ll see in the MD&A, the purchase price allocation for this acquisition has been finalised, but a number of contracts that we assumed at the time of the acquisition continue to have significant economic risk. We will report supplementary financial information regarding the MAJES acquisition until such time as we believe that the business is unlikely to have major cash flow swings.

This is the last quarterly letter to shareholders that I’ll be writing, although I still anticipate producing the annual letter to shareholders. We plan to incorporate the table that appears in this letter into our future MD&A documents.

At the time of our initial public offering we established an objective of generating in excess of 20% average annual revenue growth per share and EBITDA growth per share for the period January 1, 2006 through December 31, 2010. We continue to believe that the employees of Constellation will deliver this remarkable performance despite the constant (well intentioned) reminders of shareholders and analysts that we will inevitably revert to the mean and be subject to the law of large numbers.

Mark Leonard, President

November 3rd, 2009

We had discontinued the quarterly president's letter, but the events of this last quarter warrant an exception. In November 2009, our Trapeze Operating Group purchased the PTS business from Continental Automotive. This is a large and very different business from our core vertical market software businesses: It requires skills in wireless networks, mobile computing hardware, and system integration. The industry has a very spotty history of profitability, and seems to have a voracious appetite for working capital. The contracts are alluringly large and have historically been won by vendors offering to meet stringent performance criteria which are apparently very difficult to achieve in real world situations. PTS is one of the largest competitors in this industry.

We are well aware of the industry's unfortunate history, and as Mark Miller, the general manager of our Trapeze Operating Group explains below, we believe we can avoid repeating that history. In a nutshell, we only intend to take new customer contracts when the contract risks are appropriate, otherwise we will concentrate on providing superior service to the acquired PTS customer base.

Mark Miller, Trapeze Operating Group, re. the PTS Acquisition

PTS develops technology for Vehicle Fleet Management (VFM) for transit agencies primarily in North America, continental Europe, and the United Kingdom.

Trapeze’s traditional transit business provides single and multi-departmental software systems for both public and private transit operators in all of the above markets. Specifically, Trapeze’s systems deliver planning, scheduling, fleet maintenance, work force and customer relationship management technology to its transit customers.

Since Trapeze’s departmental systems both send and receive data to and from VFM systems this has required connecting with several VFM systems for over the last 10 years, including the newly acquired PTS VFM system. These interfaces create duplication of data and business logic that have a high cost to acquire, maintain, and modernize.

To reduce the VFM system integration cost for our customers Trapeze began to internally develop an integrated VFM. This opened up a newly addressable market for Trapeze. The development of this system began 5 years ago and has been implemented at several of our customer sites. This system was developed as an extension to Trapeze’s existing departmental systems and was designed to target mid- to low-end transit customers that owned other Trapeze products.

By acquiring PTS, Trapeze has achieved three objectives.

VFM systems are complex to develop and implement. With the acquisition of PTS we acquired Intellectual Property that is expected to enhance our ability to deliver increased functionality to our customers and we have engaged an experienced team with the capability of installing and developing VFM systems on a larger scale than we'd previously pursued.

In North America and the United Kingdom we share many joint customers with PTS. We intend to improve the integration of our products and to eventually eliminate duplication of effort. In addition, we intend to provide the PTS VFM clients with access to many of Trapeze' other departmental systems.

In Europe, PTS has strong share of the DACH (German, Austrian, and Swiss) market for VFM systems. Trapeze has a good market share in Scandinavia in its traditional multi-departmental systems but has only a 2 limited number of customers in DACH. The acquisition provides a significant presence in the DACH markets with the opportunity to cross-sell other Trapeze systems over time.

With the acquisition of PTS we took over a number of uneconomic contracts that we are working to resolve. Historically PTS has focused on winning large contracts that can be in the ten of millions of dollars in size and sometimes even larger. These contracts often have unattractive contract terms. There are bonds, liquidated damages, penalties, and aggressive timelines. Larger contracts typically have many customization components that make it difficult to predict development timelines. As a result, project delays occur, which can lead to ballooning working capital and cost overruns.

Historically at Trapeze we achieve most of our revenue by continuing to deliver more value to our existing customers through a more integrated system that minimizes data duplication and provides additional functionality. PTS has not focused on this higher margin recurring revenue stream. We plan to provide new or improved functionality to the PTS customer base. We believe this can be achieved by improving PTS’ existing products, cross-selling other Trapeze products, developing new products, and acquiring complementary technologies.

A long term relationship with our customers must make sense for both parties. We intend to deliver value and in turn be paid equitably for our efforts. Being more selective with new business opportunities and carefully evaluating the economic terms and conditions prior to establishing the relationship, is necessary.

As we work through the contracts we received as part of the acquisition we anticipate PTS profitability will be depressed and volatile. We also expect the business to shrink in size as we change the strategy to be more customercentric and selective as to which new projects we decide to bid. As our existing customer base revenue increases at PTS, we expect to be able to reduce working capital and improve our margins. This won't happen quickly, certainly not within this calendar year. Our belief is that PTS will eventually be one of our best acquisitions, providing both a strong return on investment, and products and skills that will allow us to better serve our transit clients.

Mark Miller, President Trapeze Software Inc.

Mark Leonard, President Constellation Software Inc.

March 3, 2010

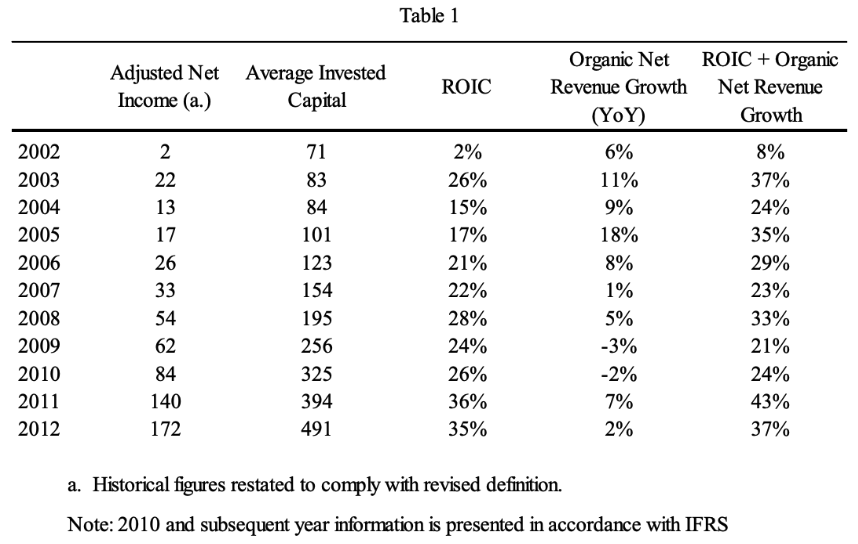

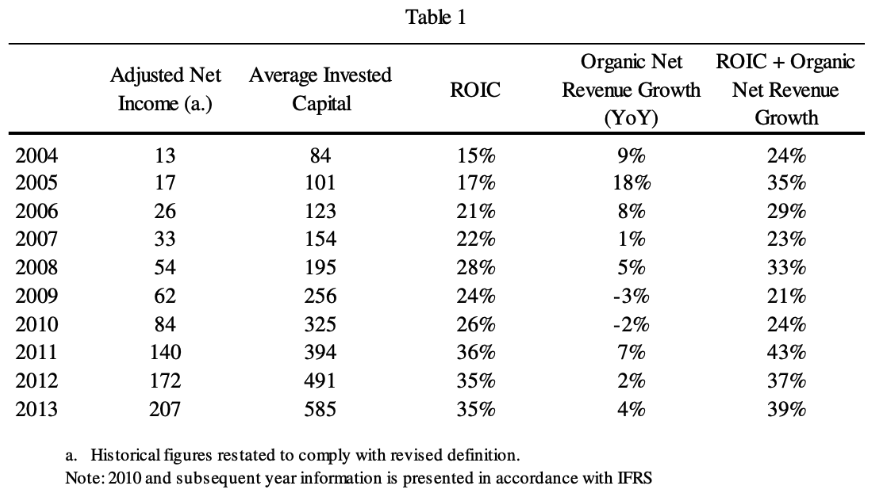

GAAP statements tend to be the best tool that investors have to monitor and judge a company’s performance. We have tried to supplement GAAP by providing you with our own calculations of Adjusted Net Income, Average Invested Capital, ROIC, Organic Net Revenue Growth, and Attrition (the “CSI Metrics”) amongst others. The CSI Metrics do attract cynicism from some quarters, so I’ve also included in this letter a couple of GAAP financial metrics that reflect the company's performance over the last decade. I welcome any suggestions that you may have for other metrics to include in these annual letters.

The definitions of Adjusted Net Income, Average Invested Capital, ROIC and Net Revenue appear in the Glossary below.

Internally we think about Adjusted Net Income as the cash profits we generate after paying cash taxes. The most significant variation from GAAP net income, is that we assume our intangible assets are not diminishing in economic value. This is a critical assumption that our board challenges, and that you, as shareholders, need to monitor. The way we support the “ever-expanding intangibles value” contention with our board is by regularly forecasting the cash flows for each of our acquired business units and comparing them to our original acquisition costs to calculate acquisition by acquisition IRR’s. We don’t provide this level of disclosure to our shareholders because we want to avoid the cost to the company (having done more than 100 acquisitions), the disclosure of competitive information to competitors and overwhelming shareholders with the sheer volume of information that would be required. Instead we disclose the annual changes in our maintenance revenue base, with a particular focus on the organic changes. Our attrition statistics show that we have grown our maintenance revenues organically, even during the recent recession, so I’d argue that the economic value of our intangibles in aggregate has increased rather than decreased for as long as we’ve done our annual maintenance attrition surveys.

And when we think about Invested Capital, we think about the shareholder capital that has been invested in the businesses, plus any Adjusted Net Income less any distributions. Obviously, when you divide Adjusted Net Income by Invested Capital, you get a measure of the return on our shareholders’ investment (i.e. ROIC). If you add Organic Net Revenue Growth to ROIC, you get what we believe is a proxy for the annual increase in Shareholders’ value. In a capital intensive business you couldn’t just add Organic Net Revenue Growth to ROIC, because growing revenues would require incremental Invested Capital. In our businesses we can nearly always grow revenues organically without incremental capital.

If you refer to Table 1, you’ll see that Average Invested Capital is compounding at a handsome pace, largely because we are generating attractive ROIC’s and are paying only a modest dividend. In 2009 we generated a 24% ROIC. I’m particularly pleased with this performance, as it was achieved in a recession, and despite a significant adverse move in currencies. The trend in Organic Net Revenue Growth is less attractive. In the middle of the decade we generated double digit growth rates, but this has slowed, culminating in a 3% contraction in 2009. This is the worst performance that we’ve experienced since we started tracking Organic Net Revenue Growth. The macro economy had a significant influence on our organic growth, but some of the decelerating growth is also self imposed. In 2004 we started tracking CSI’s investments in new Initiatives on an Initiative by Initiative basis. The system was not without flaws, but as the longitudinal data has gradually been amassed, it has convinced me and many of our other managers that the returns that we are generating on these investments are nowhere near as good as we had originally hoped. I believe that our efforts to generate better returns from Initiatives have permanently reduced the amount of Organic Net Revenue growth that we will seek. We are currently targeting an average of 5% organic growth over the long term.

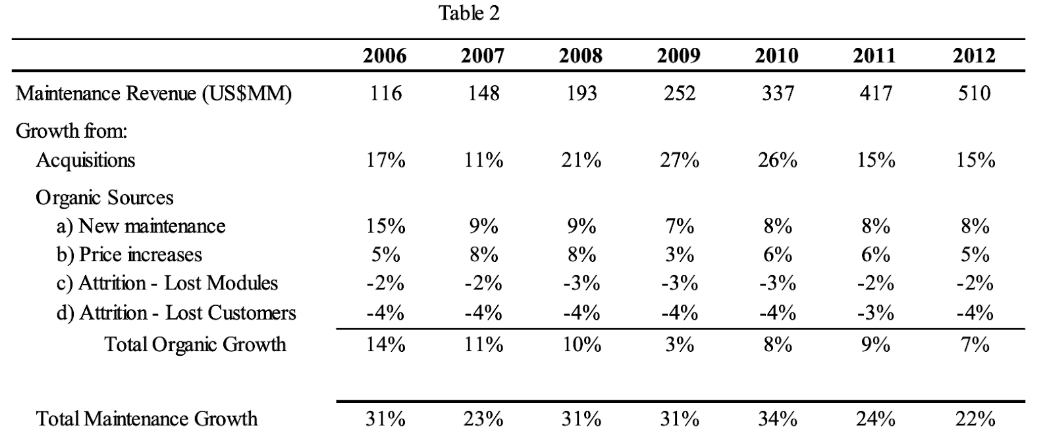

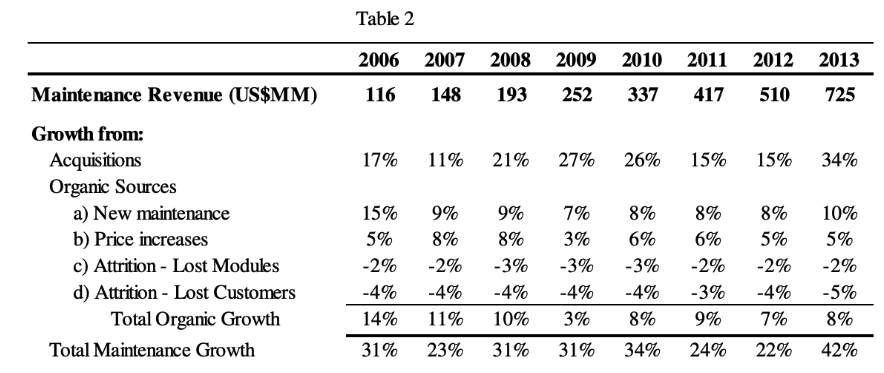

The attrition statistics for 2009 and the previous three years appear in Table 2. We calculate attrition and growth each year based off of the prior year’s GAAP maintenance revenue, rather than the run-rate of maintenance revenue at the end of the prior year. This creates a persistent overstatement of both organic growth and attrition if we consistently acquire significant amounts of maintenance revenue late in each year. Foreign exchange changes during the last couple of years have been significant and also complicate the analysis. Despite the challenges of pulling together accurate data across tens of thousands of clients in a multitude of different geographies, we believe that the table is indicative of the trends in our maintenance base.

Our customer and module attrition has consistently been less than the sum of new maintenance revenue plus maintenance price increases (i.e. the organic growth in our maintenance revenue has been positive). This suggests that the economic value of Constellation’s intangible assets has appreciated even during the recent recession. And while the Total Organic Growth in maintenance has slowed during the recession, 2009 was a record year for the acquisition of maintenance revenues so we still had a very attractive increase (31%) in our maintenance revenues. It seems intuitively appealing that as we go through an economic cycle there will be good times to organically grow maintenance revenues and good times to buy maintenance revenues, and that those events will rarely coincide. I only wish we had acquired more maintenance during the recession before acquisition prices rebounded.

Our attrition rates also illustrate the long-term nature of our client relationships. Attrition due to the loss of customers in 2009 was ~4%, suggesting that our average customer will stay with Constellation for 26 years. Customer relationships that endure for more than two decades are valuable. We have symbiotic relationships with tens of thousands of customers: we handle thousands of their calls each day, and issue scores of new versions of mission critical software each year which incorporate their feedback and suggestions. For an annual cost that rarely exceeds 1% of a customers’ revenues, our products help them run their businesses efficiently, adopt their industry’s best practices, and adapt to changing times.