)

)

)

Company research25 May 2024

EQT: From Nordic Roots to Global Dominance

EQT's growth from a Nordic-focused firm to a global investment leader highlights its commitment to responsible ownership, innovative strategies, and sustainability.

Verisure was founded in Sweden in 1988 as Securitas Direct, providing professionally monitored alarms for homes and small businesses. Since then, it has grown into Europe's largest monitored alarm provider, serving more than five million customers across 17 countries. After years under private equity ownership and steady expansion, the company is now preparing for a return to the public markets. Let's take a closer look at Verisure's journey and what lies ahead.

Securitas roots: Verisure traces back to 1988, when Securitas launched Securitas Direct to provide monitored alarms for homes and small businesses.

Private equity ownership: Private equity has shaped Verisure's path since 2008, with Hellman & Friedman today holding a majority stake alongside GIC and Alba.

Market comeback: After years of growth under private ownership, Verisure is ready to return to the stock market on October 8.

Verisure traces its roots back to Sweden in the late 1980s as part of Securitas, a global security services company. In 1988, Securitas launched a new segment named Securitas Direct, a provider of professionally monitored alarms for homes and small businesses. In a few years, the service combined its intrusion alarms with 24/7 monitoring and rapid response, offering customers security solutions that basic locks or insurance couldn't.

While it continued to innovate with wireless technology and image verification, Securitas Direct was spun out as a separate company in 2006 and listed on the Stockholm Stock Exchange.

A short sidenote here: Securitas is no stranger to spin-offs. Beyond Securitas Direct, it also spun off Assa, which later merged with Finland's Abloy to form Assa Abloy, now a global leader in locks and access solutions, as well as Loomis, a specialist in cash handling.

Back to Securitas Direct. Although it maintained its momentum in the public markets, its time as a listed company would prove short. By 2008, just as it surpassed one million customers, it was acquired by private equity firm EQT. As a private company, it was rebranded Verisure, accelerating both international expansion and a broadening of its services.

Today, Verisure operates in 17 countries across Europe and Latin America, serving more than five million customers. From its Swedish origins, it has grown into Europe's largest monitored alarm provider, far beyond the scope of its original offering.

Get curated quality company deep dives every other week.

Over the years, Verisure has expanded well beyond traditional burglar alarms to include smoke detectors, smart locks, security cameras, and other connected services. All of these vertically integrated products are linked through a unified security ecosystem. Today, the company manages more than 85 million connected devices and processes 1.4 trillion signals annually.

Its revenue streams are divided into three parts. The largest part, portfolio services, makes up nearly 87% of revenue and consists of subscription-based monitoring and support (sourced through Quartr Pro). This highly recurring cash flow funds the company's growth engine. The second, customer acquisition, covers the installation of alarm systems for new clients. While this segment typically operates at a cash flow loss, it is essential for expanding the subscriber base that feeds into portfolio services. The third, adjacencies, is smaller but strategically important, spanning services such as senior citizen monitoring and connected camera systems.

Verisure's core customers remain residential households and small businesses, and it avoids larger-scale enterprises and government contracts. This focus has made it the leading security installation provider in 13 of the 17 countries where it operates.

Verisure's business model translates into a combination of resilience and growth. Over the past decade, the company's annual attrition rate has remained below 8%, while the average customer lifetime exceeds 15 years. Together, these figures highlight the stickiness of its services: once customers sign on, they tend to stay.

This dynamic underpins Verisure's self-funding growth flywheel. In 2024, the company generated €1.2 billion in portfolio cash flow, reinvesting 61% of it into acquiring 840,000 new customers while still expanding profitability. The formula is straightforward: subscription revenues generate cash flow, which is reinvested in new customer acquisition, which in turn grows the base of recurring revenues and compounds value over time.

Over the last 15 years, annualized recurring revenue has grown at a 14% CAGR, reaching €3.1 billion by the end of 2024. That year, Verisure reported total revenue of €3.4 billion and EBIT of about €740 million, corresponding to a margin of roughly 22% – a level it has consistently maintained in recent years.

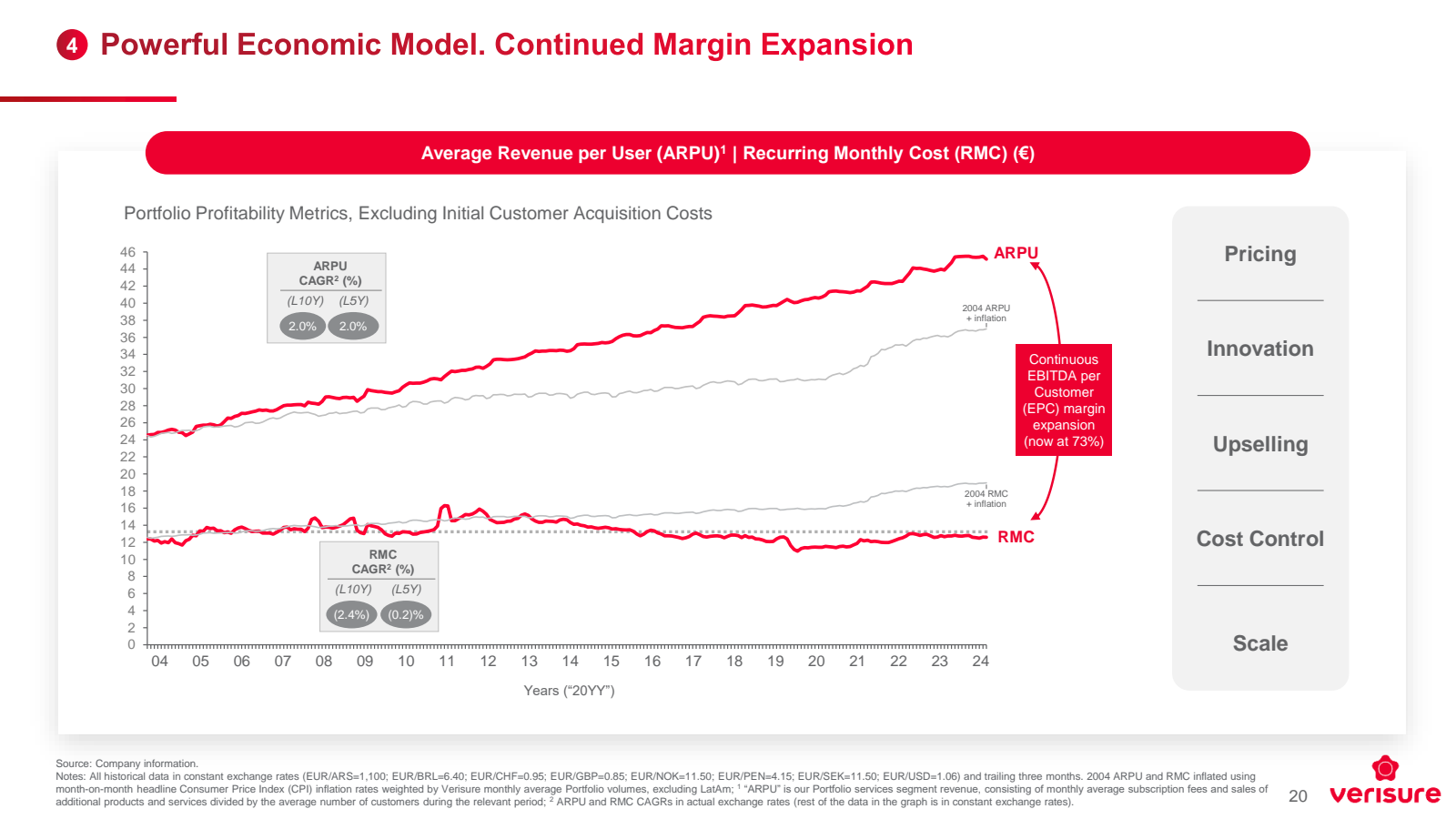

Over time, as Verisure has scaled its operations, it has also become more efficient. Average revenue per user has risen at a 2% CAGR over the past decade, while recurring monthly costs per customer have fallen by a CAGR of 2.4%. The result is steady margin expansion per customer:

After being taken private by EQT in 2008, Verisure was sold to Hellman & Friedman and Bain Capital in 2012 in a deal that valued the company at roughly €2.3 billion.

Three years later, Hellman & Friedman bought out Bain and has remained the controlling shareholder ever since, currently holding about 59% of the company. Other notable investors include GIC, Singapore's sovereign wealth fund, with around 21%, and Swiss investment firm Alba with 8%, while the remaining 13% is distributed among smaller owners.

Speculation about a potential IPO has circulated for years, but a concrete listing is now drawing closer. On September 29, Verisure confirmed that the company is set to list on Nasdaq Stockholm on October 8.

The offering is expected to raise €3.1 billion. Verisure is targeting a share price interval of €12:25-13:50, which would take its market capitalization to €12,9-13,9 billion. It would mark Europe's largest IPO since Porsche made its debut in 2022.

Verisure's path from a Swedish alarm provider to Europe's largest monitored security company has been a story of expansion, steady growth, and resilience. With millions of loyal customers and a business model becoming more efficient as it scales, it's now ready for its next chapter. The stage is set for its return to the public markets.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)