)

)

)

Company research17 Oct 2025

Beneath the Surface: A Conversation with Epiroc CEO Helena Hedblom

Legacy, innovation, and leading one of Sweden's most influential industrial companies into a new era.

What started as a manual on securities 125 years ago has grown into one of the most influential institutions in global finance. Since then, Moody's has expanded from publishing investment information to setting the standards by which credit risk is measured worldwide. Today, its ratings are embedded in the financial infrastructure, shaping how issuers borrow, how investors allocate capital, and how regulators safeguard stability. This is the story of Moody's.

The foundational publications: What started with John Moody's bond analyses in the early 1900s gave rise not only to Moody's but to the modern credit rating system.

Spin-off in 2000: After decades under Dun & Bradstreet, Moody's was spun off at the turn of the millennium, establishing itself as an independent, publicly traded company.

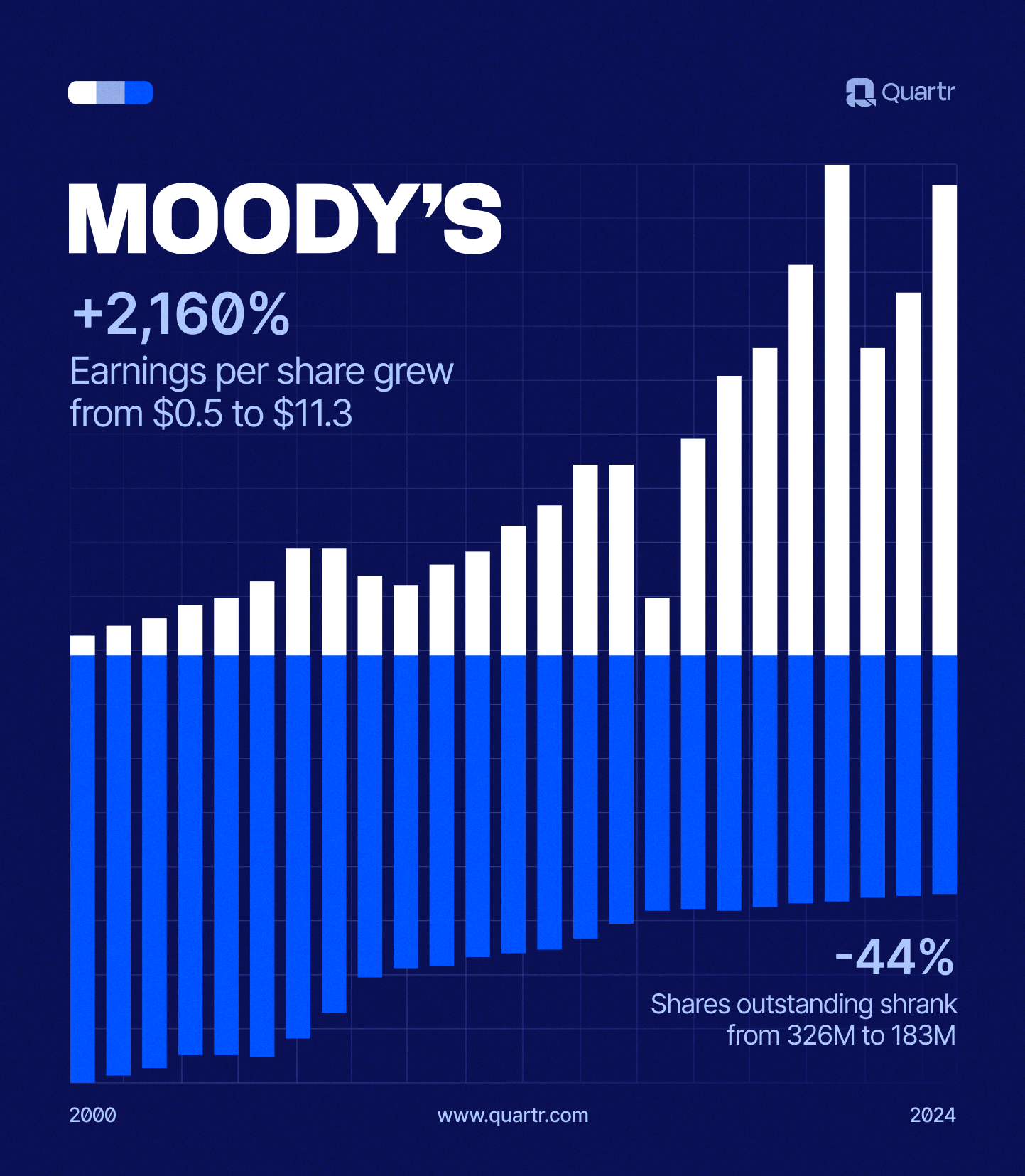

Capital allocation: Since 2000, Moody's has steadily raised its dividend and reduced its share count through consistent buybacks.

In the early 1900s, what is now a cornerstone of global credit markets began with the publication of a securities manual. That first step marked the start of Moody's journey into one of modern finance's most influential institutions.

In 1900, John Moody, a former Wall Street broker, published Moody's Manual of Industrial and Miscellaneous Securities, a detailed reference covering stocks, bonds, utilities, and other securities. At a time when investors lacked centralized, reliable information, the manual quickly became an indispensable tool. In the years that followed, Moody continued releasing updated editions of the manual, building on the reputation of his data.

The financial panic of 1907 forced Moody to sell both his business and the rights to the manual. By 1909, however, he had returned with Analysis of Railroad Investments, published under the newly formed Moody's Analyses Publishing Company. This work focused exclusively on railroad bonds (the dominant form of corporate debt at the time) and, for the first time, introduced a grading system to evaluate their credit quality.

While Moody acknowledged earlier credit practices as inspiration, his system of standardized, publicly available ratings marked the true beginning of the modern credit rating industry.

Get curated quality company deep dives every other week.

Over the following decades, Moody's publications expanded in scope and inspired competition from new entrants. By the early 1920s, Fitch Publishing Company, Standard Statistics, and Poor's had all begun releasing their own ratings and analyses. A quick sidenote: these firms, together with Moody's, make up today's “Big Three” credit rating agencies, with Standard Statistics and Poor's having merged to form S&P Global.

Moody's quickly became a central fixture in finance, valued for the transparency its ratings provided to investors. As capital markets developed and financial regulations took hold, reliance on formal credit ratings steadily increased, cementing Moody's role at the core of the system.

In 1962, Moody's was acquired by Dun & Bradstreet, a firm with its own long history in credit reporting. Despite the new ownership, Moody's continued to operate much as before, broadening its coverage and strengthening its reputation as one of the most influential voices in global finance.

By the late 1990s, Moody's strong performance and distinct identity led to growing pressure for independence. In 2000, it was spun off from Dun & Bradstreet and listed on the New York Stock Exchange.

The spin-off in 2000 marked the beginning of a new chapter, carrying forward a position it had earned through trust, a well-established methodology, and an influence that has only deepened since.

Moody's of today can be described as a global integrated risk assessment firm with roughly 16,000 employees across more than 40 countries. Although its ratings remain its core and what it is mainly associated with, its business now stretches beyond its original offering.

In 2024, Moody's generated a revenue of $7.1 billion, growing with a CAGR of 11% since its spin-off from Dun & Bradstreet. The business is organized into two main segments: Moody's Investors Service (MIS) and Moody's Analytics (MA).

MIS is the company's historical core segment, responsible for credit ratings and research. With more than a century of history, its trusted service is built around assessing the creditworthiness of debt issuers. These range from corporations and financial institutions to sovereigns, municipalities, and structured products such as mortgage-backed securities and collateralized debt obligations.

The model is straightforward: when an issuer wants to raise debt, they typically pay Moody's to provide a rating that investors can rely on when evaluating the security. That rating is then monitored and updated over time, generating a mix of upfront and recurring fees.

With roughly 55% of total revenue and margins north of 60% in 2024, MIS remains the economic engine of Moody's. Its historical positioning, expertise, and rigorous methodology have made its ratings the gold standard in global credit markets, trusted by issuers, investors, and regulators alike.

The other side of the business is Moody's Analytics (MA), which has grown into a solid recurring-revenue contributor since its launch nearly two decades ago, contributing to roughly 45% of the total in 2024. Unlike the ratings arm, MA monetizes Moody's data and research through integrated solutions that help clients assess risk, manage portfolios, and meet regulatory requirements. Its customers include global banks, insurers, corporates, asset managers, and government agencies.

Its offerings span cloud-based platforms for loan origination and portfolio management, insurance risk models, and compliance products such as Know Your Customer (KYC) services. The segment is primarily subscription-driven, and while its profitability trails the ratings business, MA still delivers operating margins above 30%.

Together, MIS and MA generated $3 billion in EBIT in 2024, corresponding to a margin of 42%. Since its spin-off from Dun & Bradstreet in 2000, Moody's has improved EBIT at a 10% CAGR.

Moody's combines strong cash generation with a disciplined approach to capital allocation. In 2024, the company produced $2.5 billion in free cash flow. Consistent with its outlined strategy, approximately 80% of that is returned to shareholders, with the rest directed toward growth initiatives.

In practice, this translates into a clear framework: reinvest in organic growth and occasionally in targeted acquisitions, then balance dividends with share repurchases. Moody's dividend has grown at a 17% CAGR since separating from Dun & Bradstreet in 2000. Another important component is share repurchases. Moody's has been buying back shares consistently since its spin-off, reducing the number of outstanding shares by a total of 44%.

“And this quarter highlights the unique strength of our business model. We're tracking to our medium-term EPS target of low double-digit growth while we are funding this investment program that will drive future growth, all while we expect to return over $1.6 billion to stockholders this year through share repurchases and dividends. That is the power of the Moody's compounding machine.”

– Robert Fauber, CEO of Moody's, at its Q1 2024 earnings call (sourced through Quartr Pro).

For over a century, Moody's has shaped the way credit markets function. Its methodology and reputation have made its ratings a global benchmark, relied upon by issuers, investors, and regulators. Today, it stands as one of the most enduring and influential institutions in modern finance, with its position only growing stronger.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)