For a retail investor, MSCI is one of those names that pops up every once in a while. Perhaps it's flashed by in the name of an ETF, on a fund fact sheet, or in a presentation. But for an institutional investor, it's one of the most important companies in the world. What began as a tool to benchmark international equities has evolved into a deeply embedded platform that guides trillions of dollars in asset allocation, portfolio construction, and investment strategy. This is the story of MSCI: where indexing meets infrastructure at a global scale.

Behind the benchmarks

MSCI might be one of the most recognized names in investing, yet few people could tell you exactly what the company does. At its core, the company creates market indexes that help investors benchmark performance and structure portfolios. While this might sound simple, perhaps even negligible, that's far from the truth. Over the decades, it has become one of the most deeply embedded and indispensable layers of financial infrastructure in the world.

The result of this positioning is a business with extraordinary stability – one that quietly operates in the centre of passive investing, portfolio construction, and global capital flows. The outcome: standout performance. Since its IPO in 2007, MSCI's stock has delivered a CAGR of over 20%, fueled by revenue and EBIT growth of 15% and 22% per year, respectively, over the past two decades.

Let's rewind to where MSCI's story began: toward the end of a two-decade market comeback after a global depression and a world war.

Showcasing MSCI's financial growth and scalability over the last two decades.

The history of an index pioneer

We begin this story in the late 1960s. After some frankly horrendous decades that had encompassed the crisis of 1929, followed by the Great Depression and finally the Second World War, global equity markets entered a period of renewed strength. Investor confidence was returning, and as globalization gathered pace in the real economy, public markets began to reflect that shift. More capital was flowing across borders, and institutions were looking for ways to navigate an increasingly interconnected world.

It was during this time that an idea of bringing more structure to global investing began to take shape. In 1968, Capital International, a division of the investment management firm Capital Group, launched a series of global equity indexes that would later form the foundation of MSCI. The project was aimed at helping institutional investors benchmark international performance, allocate capital more precisely, and compare exposure across countries and regions.

In the years that followed, Capital International rolled out indexes that covered the U.S., Europe, Asia, and Australia, along with broader global benchmarks. The most notable of these was the EAFE Index (short for Europe, Australasia, and the Far East), which became the first global equity index of its kind. It offered investors a way to track and access a diversified portion of markets outside North America.

As the 1970s unfolded, Capital International continued to expand its coverage, adding more countries and regional indexes. By then, many institutional investors, including large U.S. pension funds and global asset managers, were using the EAFE and other Capital International indexes to benchmark the performance of their international holdings. The indexes filled a crucial gap in global investing and quickly became the industry standard for measuring non-U.S. equity market performance.

The MS to the CI

In 1986, Morgan Stanley, which was an early client of Capital International's indexing business, acquired a large stake in the operation, securing full rights to the indexes. It rebranded the business by adding its own name, creating Morgan Stanley Capital International, MSCI. Morgan Stanley had ambitious plans to expand the indexing business beyond its original focus and transform it into a truly global platform.

In 1988, MSCI launched its first major product under the new ownership: the MSCI Emerging Markets Index, covering 10 developing markets. At the time, these markets represented less than 1% of global public equity market capitalization, but they would later become a core allocation for global investors. This was eventually followed by the MSCI All Country World Index, which brought together developed and emerging markets into a single benchmark.

These innovations marked a turning point, expanding MSCI's offering from a pioneering benchmark provider into an emerging leader in the evolving global indexing landscape. Morgan Stanley's involvement was instrumental, not just as a financial backer, but as a strategic partner with the distribution reach to accelerate adoption. Under its guidance, MSCI further enhanced its methodology, introducing standardized rebalancing schedules and shifting toward free-float-adjusted market cap weighting.

As MSCI expanded its global indexing offerings, it entered a market that already included players like FTSE (launched in 1984 by the Financial Times and the London Stock Exchange) and S&P (published by Standard & Poor's, a division of McGraw-Hill). But instead of going head-to-head, MSCI carved out a stronghold in international and emerging markets, a segment that had up until this point had been relatively underserved. Early adoption by institutional investors gave it a lead in the niche that would prove both durable and defensible.

Throughout the 1990s, MSCI continued to broaden its coverage. It moved into small-cap and frontier markets and launched more specialized indexes targeting sectors, industries, and investment styles like value and growth. This expanding lineup made MSCI increasingly indispensable to asset managers seeking global exposure with precision. At the same time, it developed tools and data feeds that helped institutional investors integrate its indexes more seamlessly into portfolio construction and performance measurement.

In 1996, Morgan Stanley, in collaboration with fund manager Barclays Global Investors (a division of Barclays), launched a series of ETFs called World Equity Benchmark Shares (WEBS), designed to track MSCI's international stock market indexes. Unlike the earlier SPDR fund, which was structured as a unit investment trust with limited flexibility, the WEBS were organized as open-end mutual funds, allowing for features like dividend reinvestment, securities lending, and easier fund adjustments.

While basic index-tracking products had existed for roughly two decades, they lacked tradability and accessibility. This more adaptable structure helped broaden ETF adoption and paved the way for a new generation of index-linked investment products.

The launch of WEBS also marked a turning point and a new revenue stream for MSCI, giving investors real-time access to its benchmarks through exchange-traded products for the first time. Later rebranded as iShares MSCI ETFs, they became part of BlackRock's platform after its 2009 acquisition of Barclays Global Investors.

By adding these new products on top of its already strong benchmark products, MSCI's adoption increased. And with this, its client base grew rapidly, spanning asset managers, pension funds, sovereign wealth funds, and financial institutions around the world.

Ambitions beyond indexes

During these foundational decades, Morgan Stanley's role in MSCI's growth was indisputable. Without its parents' resources and distribution capabilities, MSCI likely would not have scaled to the level it did. But by the mid-2000s, signs began to emerge that Morgan Stanley's involvement might be nearing its end, as MSCI started exploring opportunities beyond its core benchmark and index-licensing business.

In 2004, Morgan Stanley acquired Barra, a leading provider of quantitative risk analytics and portfolio management tools, for $816 million and merged it with MSCI. The combination brought together MSCI's index expertise and Barra's analytics capabilities, creating a more comprehensive platform for clients navigating complex investment decisions.

With Barra now part of the offering, MSCI's identity as a standalone entity was beginning to take shape. And in 2007, after more than two decades as a Morgan Stanley subsidiary, MSCI was ready to operate as an independent public company.

By then, it had become an important player in the global financial system, with a rapidly expanding client base and a broad portfolio of indexes and analytics used by thousands of institutions worldwide. Its business model had evolved into one built on high recurring revenue, strong margins, and deep integration into asset management workflows. It was clearly no longer just a division, but a global platform in its own right.

Sign up for Edge

Get curated quality company deep dives every other week.

The spin-off of MSCI

In July 2007, Morgan Stanley announced it would spin off a minority interest in MSCI through an initial public offering, selling roughly 15% of the company. Following the IPO, Morgan Stanley still retained a majority stake of over 80%, while Capital Group held on to a small minority position.

The rationale was clear on both sides. For Morgan Stanley, the spin-off was about unlocking the hidden value of a fast-growing but underappreciated asset, while allowing the bank to focus on its core investment banking and wealth management operations.

For MSCI, Morgan Stanley had played a vital role in scaling the business, but by 2007, its ownership had also become a constraint. As a subsidiary of an investment bank, MSCI likely faced limitations, especially when competing for clients that were also Morgan Stanley's rivals, or when pursuing partnerships and acquisitions that might raise conflict-of-interest concerns. Independence offered the chance to sharpen its strategic focus, strengthen its neutrality in the eyes of the market, and pursue growth more freely.

The IPO of MSCI was launched in November 2007. On its first day of trading, MSCI was valued at $1.86 billion. By the closing bell, that valuation had jumped 45% to $2.7 billion, proving that there was plenty of investor appetite for the newly independent company.

A highly anticipated newcomer

MSCI's public debut stood out not just for its market reaction, but for what it represented: it was the first time an index provider had gone public as a standalone company. At the time, MSCI's main competitors were still part of larger parent companies. S&P operated within McGraw-Hill (now S&P Global), Dow Jones was under News Corp before its index business was sold to CME Group in 2010, and FTSE was still jointly owned by the Financial Times and the London Stock Exchange.

Being embedded into larger entities, just as MSCI had been with Morgan Stanley, made it more difficult for investors to get a clear view of how those indexing divisions performed on their own.

Looking at some of its numbers, the investor's interest was understandable. At the time of the IPO, MSCI served over 2,900 clients across 63 countries, including pension funds, institutional asset managers, central banks, and insurance companies. In 2006, the company generated $310 million in revenue, with the index business and the Barra analytics division each contributing half. Both segments were underpinned by long-term, subscription-based licensing agreements – creating a high-margin, recurring revenue model that was compelling then and remains a core strength today.

Over the next two years, Morgan Stanley gradually reduced its position. By May 2009, it had divested all of the shares it had held through the IPO, and a couple of years later, Capital Group sold its stake as well, making MSCI fully independent from its previous owners. In that short span, MSCI's entire shareholder base had been reshaped, bringing in a new set of long-term investors and a refreshed board of directors to guide the company's next chapter.

Coming out of a financial crisis that had shaken markets and institutions worldwide, MSCI was now positioned to chart its own course. Though operating at the core of financial markets during the crisis, it weathered the turmoil well – an early sign of the resilience that would come to define its business model. It still carried the initials of its former owners, but MSCI was now firmly in control of its own direction and entered the new decade with fresh momentum.

Redefining its path

An intensified refocus and acquisition spree began in 2010. In its S-1 filing ahead of the IPO, MSCI had made its ambitions clear to: “actively seek to acquire products, technologies and companies that will enhance, complement or expand our product offerings and client base.”

The company viewed acquisitions as a natural extension of its organic growth strategy, targeting opportunities that aligned with its core strengths while accelerating its expansion into adjacent areas. The vision was to build an integrated platform for institutional investors by broadening its presence across asset classes, geographies, and risk-related services.

In MSCI's 2010 annual report, CEO Henry Fernandez (who has led MSCI since 1998 and previously worked at Morgan Stanley) emphasized the focus on acquiring larger businesses with a leadership position, capable of delivering immediate impact, integrating efficiently, and deepening recurring client relationships.

What followed in the 2010s was precisely this: a series of focused acquisitions that reflected MSCI’s autonomy and long-term strategy. While the 2004 acquisition of Barra had hinted at this direction, the post-IPO deals sharpened it. MSCI expanded its capabilities in multi-asset risk analytics, extended its reach into sustainability and climate data, and broadened its footprint across fixed income and private markets. Each addition was chosen for its strategic value, reinforcing the core business and enabling cross-platform synergies.

Looking back at these years, MSCI noticeably increased its leverage as part of a more assertive approach to growth and capital allocation. The rationale behind this strategic approach was uncovered in seconds using Quartr Pro's AI chat:

Quartr Pro's AI chat: Ask anything across all events and documents from public companies and instantly find what you need.

As can be seen above, MSCI's CFO, Andrew Wiechmann, explained at the 45th Annual Raymond James Institutional Conference 2024 that its former shareholder and activist investor, ValueAct, had helped recalibrate its capital allocation philosophy. This shift has continued to shape its approach to this day. Wiechmann continues:

“And so that was an area that they were helpful to further our thinking and even refine our approach to share repurchases, where we've been extremely successful. I think we mentioned recently that we have bought back, since 2012, close to 40% of the shares of the company at an average price of around $117 per share. And so we've been extremely successful at creating value through our capital allocation.”

It's hard to disagree – MSCI's capital allocation strategy has delivered incredibly well. That approach, aligned with its series of strategic acquisitions, laid the foundation for what the company is today: an infrastructure company at the heart of global investing. Deeply embedded, widely trusted, and indispensable to financial institutions worldwide.

Riding the indexation wave

Before diving into the specifics of MSCI's business and financials, it's worth pausing to emphasize a key point. The recent parts of this story have focused on MSCI's expansion into new segments and its strategic acquisitions. But while those efforts were important, its core index business was thriving all along, steadily benefiting from one of the most powerful structural forces in global investing: indexation.

Indexation refers to the growing use of indexes not just as benchmarks, but as building blocks and tools in portfolio construction. Increasingly, indexes weren't just used to measure performance, but also to deliver straightforward stock market exposure, either through funds or build more tailored strategies around themes like sustainability, or individual sectors. Additionally, this shift created demand for complementary capabilities such as risk analytics, sustainability data, and portfolio customization. All areas where MSCI has steadily expanded its presence.

Although stock market indexes have existed since the late 1800s, index investing as we know it began in the 1970s. When John Bogle introduced the First Index Investment Trust in 1975 (now the Vanguard 500 Index Fund), it was met with open hostility from Wall Street. A satirical campaign titled “Help Stamp Out Index Funds! – Index Funds Are Un-American!” featured Uncle Sam urging investors to reject passive investing. To many in the industry, index funds weren't just unambitious, they were unpatriotic: you were paying fees to lock in average returns, with no attempt to beat the market. It was seen as a betrayal of the stock-picker's craft.

Leuthold Group's famous campaign, claiming that index funds were Un-American.

But over time, the “Un-American” option became increasingly popular. Judging by some of the great investors of the past, the market was clearly beatable, but for most people, embracing what Eugene Fama had formalized years earlier was probably the smarter choice: beating the market consistently is hard, owning it is easy.

Fast forward to the 21st century, and indexing is no longer controversial and has transitioned from measuring the market to driving it. Trillions of dollars now move in tandem with indexes, not just for tracking, but as the basis for product design, asset allocation, and investment strategy itself.

At MSCI's 2021 Investor Day, Diana Tidd, former Chief Responsibility Officer, reflected on this evolution (sourced through Quartr Pro):

“So if we look back 20 years ago, the primary users of indexes were active managers, who are using indexes as a yardstick as a measure of their performance. They would also use the index constituents as a list of potential securities to purchase for their portfolios. As time passed from 2010 to 2020, we saw the huge expansion of the use of indexes for ETFs growth in futures contracts based on multicurrency indexes, structured products, and an explosion in the use of model portfolios, which so often used to capture the exposures indexed or passively managed funds underneath to build their asset allocation for their modeled portfolio.”

MSCI was uniquely positioned to capitalize on this shift. Some parts of its index business, like ETF licensing, custom index creation, and the development of thematic, sector, and sustainability indexes, were directly tied to the capital flowing into passive products. Others, like performance benchmarking, benefited more indirectly as investors used indexes to guide allocation models and track risk-adjusted returns.

The second part of Tidd's remarks captured just how central indexing had become and how deeply MSCI was embedded in that shift:

“As we look forward, we see continued and accelerated opportunity for growth as use of ETFs expands, futures and options growth, using annuities, index-linked annuity products, fixed income, multi-asset class and new areas like direct indexing. And these new use cases put indexes at the center of the investment process. So whether it's for portfolio construction, defining the investable universe and for asset allocation or for portfolio management, use and exposure and liquidity management and performance attribution or risk management, where clients can customize their own index to meet their own risk profile or they can use futures and options contracts to hedge their exposures and, of course, reporting their benchmark performance and so much more. So when you take these huge transformations occurring in the industry and the expansion of the use cases and add a layer of MSCI's focus on relentless product innovation, you can see that if you want an index for a particular country, a region, global, a sector, developed markets, emerging markets, front-tier markets or more, we are there. If you're an asset owner, an asset manager, a hedge fund, a wealth manager, an insurance company or more, we are there. If you're looking for equity, fixed income, private asset classes, multi-asset classes, we have the indexes. If your investment approach is active, passive or indexed, quantitative and you're investing globally in ESG, climate, thematic, factors, we are there.”

As Tidd's comments make clear, indexing is no longer just a benchmarking tool, it has become the connective tissue of the modern investment process. MSCI's strategic expansion into analytics and sustainability has only strengthened its positioning in this new era. As indexing extended across asset classes and strategy types, demand grew not just for benchmarks, but for the surrounding infrastructure: risk tools, sustainability data, and portfolio insights. MSCI was uniquely aligned to meet those needs.

To illustrate what this trend looks like in practice, consider the image below from MSCI's Q1 2025 earnings call presentation, showing the rising assets under management (AUM) tied to ETFs based on MSCI indexes. It's a clear visual of how deeply MSCI is woven into the fabric of the indexation era.

Since 2008, the AUM of ETFs tracking MSCI indexes have increased from $119B to $1.78T.

MSCI of 2025

So, what does this financial infrastructure company look like beneath the topline numbers?

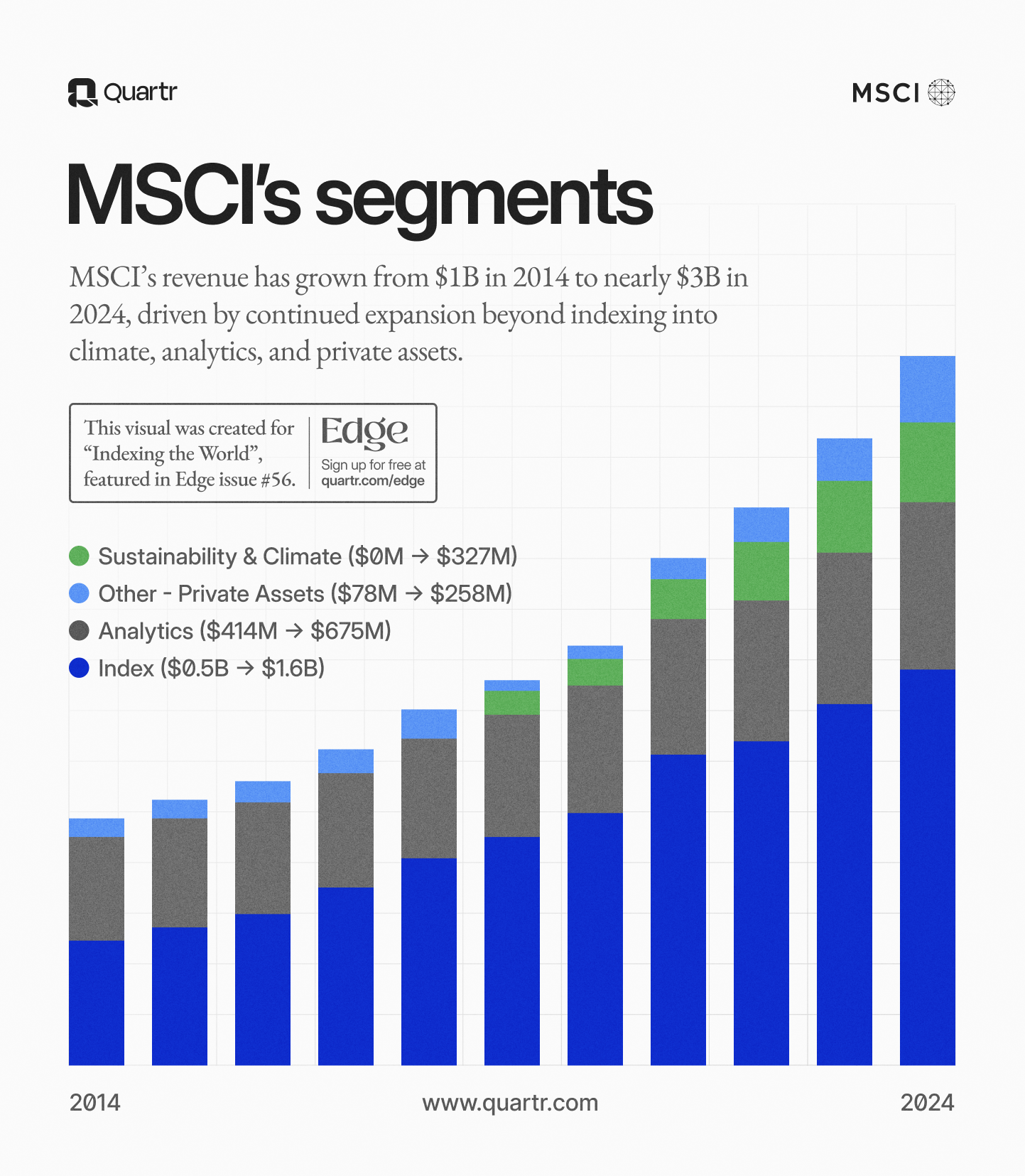

Breaking down revenue by segment, MSCI's Index segment has consistently accounted for about 55% of total revenue over the past five years. Its Analytics segment has contributed roughly 25%, while its fast-growing Sustainability and Climate segment has taken an increasing share, now representing 11% of total revenue.

Finally, we have the All Other – Private Assets. This segment builds on the trend of institutional investors increasing their allocations to private markets, offering the same kind of data, benchmarking, and risk tools MSCI is known for in public markets, but applied to the less standardized world of private equity, private credit, and real assets. The segment has grown from a 3% revenue share in 2020 to 9% in 2024, boosted in part by the integration of Burgiss, acquired in 2023.

In terms of customer mix, roughly half of MSCI's revenue comes from asset managers. Other client categories, such as banks and trading firms, asset owners and consultants, and hedge funds, each account for about 10%. MSCI's client base is well distributed globally, spanning approximately 7,000 institutions across more than 95 countries. While the Americas (mainly the U.S.) account for the largest share of revenue, MSCI also serves a wide range of clients across Europe, Asia, and other international markets.

Before we dive into the financial specifics, let's take a closer look at MSCI's three largest business segments.

Research anytime, anywhere

The #1 app for qualitative research. Live earnings calls, AI chat, transcripts, and more. All for free.

MSCI's index business is the foundation the company was built on and it has remained the cornerstone of its model ever since. Many of its other offerings, from analytics to sustainability and risk tools, have grown out of this core capability. We've already touched on the types of clients it serves and a few use cases, but let's take a closer look at how the business actually works.

Although the scope and sophistication of MSCI's index business have evolved dramatically since 1968, its core purpose within benchmarking remains the same: providing structured, rules-based representations of markets to guide investment decisions. Today, MSCI offers more than 240,000 indexes across equity and fixed income markets. Some of the most widely followed include the MSCI Emerging Markets Index, MSCI Frontier Markets Index, and MSCI World Index, but its catalog also includes a growing number of thematic, factor-based, and sustainability-focused benchmarks.

MSCI's indexes are used across a wide range of investment processes, serving as the basis for index-linked products like ETFs and mutual funds, guiding asset allocation, rebalancing portfolios, measuring performance, and informing model strategies.

Beyond standard benchmarks, MSCI also offers customization. Clients can tailor indexes by excluding specific stocks, sectors, or regions, or by aligning them with specific objectives, such as sustainability, climate, factor, or thematic exposures. This flexibility allows investors to adapt MSCI's methodologies to meet regulatory requirements, investment mandates, or strategic preferences.

One of the most common use cases is ETF index licensing, where an asset manager licenses an MSCI index to serve as the blueprint for an ETF. The ETF is constructed to closely mirror the index's holdings and weightings, and as MSCI periodically updates the index, the ETF is rebalanced to maintain alignment. This ensures that when you invest in an ETF tracking an MSCI index, you're getting precisely weighted exposure based on a methodology trusted by institutions worldwide to reflect that market as accurately as possible.

Deeply embedded infrastructure

At its core, index services like MSCI's are essential infrastructure for institutional investors, many of whom are required to benchmark performance against widely recognized indexes.

MSCI's indexes are often seen as representative of “the market” as a whole. This stature, built on decades of global market data, widespread institutional adoption, and consistently applied index methodologies, feeds directly into the strength of the MSCI brand. Having “MSCI” in a fund's name signals consistency, transparency, and institutional acceptance, especially in global or sustainability-focused products. It has become a shorthand for quality across the entire value chain, from meeting regulatory and mandate requirements to reassuring individual investors choosing an ETF with a trusted name.

One of the most powerful advantages that MSCI has is how deeply integrated its products are in the workflows of its clients. Its indexes and analytics support everything from portfolio construction and asset allocation to performance attribution and reporting. This level of integration creates substantial switching costs: replacing MSCI often means overhauling internal systems, rewriting client mandates, and redoing regulatory disclosures. For most firms, the disruption far outweighs the potential cost savings.

An additional aspect is the potential consequences for individual funds having benchmarked against the same index for years or decades and then switching. This might introduce complexity in backtracking historical performance and may send an unintended signal to investors, raising questions about consistency or strategy.

Another critical factor is MSCI's scale and breadth. With over 240,000 indexes across geographies, asset classes, factors, and themes, it can support nearly any mandate – from standard beta exposure to sophisticated sustainability overlays.

Add to that its customized reporting tools, tailored benchmarks, and integrated analytics, and MSCI offers a level of continuity and convenience that's hard to replicate. This comprehensive, deeply rooted presence is what has transformed MSCI's role in finance from a service provider to infrastructure.

This depth also reflects how MSCI has structured its broader offering. Since being spun out in 2007, the company has steadily expanded its presence into analytics, sustainability, and private assets. Not just to diversify, but to build an interconnected platform for institutional decision-making. What often begins as an index relationship frequently grows into broader adoption of MSCI's risk models, sustainability data, and climate reporting tools.

This broader integration is supported by MSCI ONE, a platform designed to give clients a unified entry point to the company's content across public and private markets. Besides improving the client experience, it also helps MSCI scale relationships and support several parts of the investment process.

On the Q1 2025 earnings call, CEO Henry Fernandez highlighted that, “88% of our subscription run rate comes from clients who use multiple MSCI product lines.” That growing cross-segment adoption is a direct result of MSCI's platform design, encouraging expansion from initial index relationships into its other products. Sustainability ratings flow into index construction. Climate data powers transition risk analytics. Factor models inform portfolio optimization and new index launches. Private asset data increasingly complements climate risk models.

The more clients adopt, the more indispensable the platform becomes, creating a self-reinforcing cycle. And as MSCI becomes further embedded in decision-making, reporting, and regulatory workflows, its competitive edge grows both deeper and wider.

Client risk in the index oligopoly

Despite its scale and embedded role in global finance, MSCI still faces competition and the risk that even long-standing client relationships may shift. In 2012, Vanguard announced that it would transition 22 of its index funds, totaling $537 billion in assets, from MSCI benchmarks to those provided by FTSE Russell (now owned by LSEG) and the Center for Research in Security Prices (CRSP), in a move aimed at reducing licensing costs.

Although the shift was only said to impact roughly 3% of MSCI's annual revenue, the market feared that the product might not be as sticky as earlier thought and that perhaps some of its clients might want to reconsider or at least re-negotiate their agreements. These fears led to a nearly 30% drop in the stock within a week.

In response, BlackRock – MSCI's largest client then and now, with iShares funds closely tied to its benchmarks – publicly reaffirmed its commitment: “MSCI is the gold standard of global and international equity indexes – the near-universal choice of professional investors. We plan to deepen our partnership with MSCI to help deliver the highest quality products and portfolio construction to our clients.”

Despite the concerns raised in 2012, MSCI's major client relationships have remained strong. As of 2024, BlackRock accounted for roughly 10% of MSCI's total revenue, primarily from fees linked to the assets in its MSCI-based products. While the longstanding relationship and deep integration reduce the likelihood of churn, the loss of a client like BlackRock would represent a significant blow to MSCI.

In reality, the global index landscape has become something of an oligopoly. The early competitors of MSCI, S&P Dow Jones Indices, and FTSE Russell still dominate, each with its own stronghold. MSCI leads in international equity benchmarks, including developed, emerging, and frontier markets, and is widely used in global ETFs and institutional mandates. S&P is firmly rooted in U.S. equities via the S&P 500 and other influential benchmarks, including sector and futures-linked indexes. FTSE Russell, under the LSEG umbrella, dominates the U.K. equity market and is also behind the widely used Russell 1000 and 2000 indexes, mainstays in U.S. small- and mid-cap investing.

These indexes are deeply embedded in asset manager workflows, investment mandates, and decades of historical data. As a result, competition among providers is less about displacing one another and more about defending their respective territories. The cost, operational burden, and signaling risk of switching benchmark providers all reinforce this status quo, keeping most clients firmly in place.

Analytics: data driving decisions

MSCI's analytics business began with the acquisition of Barra in 2004 and was significantly expanded in the 2010s, most notably through the purchase of RiskMetrics, a former JPMorgan Chase spin-off. Since then, the segment has grown into a comprehensive offering that supports portfolio construction, performance attribution, and risk management across asset classes. These tools support clients in simulating exposures to credit, liquidity, and market risks, delivered through APIs and platform integrations embedded into daily workflows.

One of the core offerings is Equity Analytics, which supports stock selection, portfolio construction, and performance attribution. At its core is the Barra equity factor model, attributing risk and return to systematic drivers such as value, momentum, size, industry, and region. Typical users include quantitative and fundamental asset managers, hedge funds, and equity portfolio managers seeking deeper insight into portfolio exposures and positioning.

To give a sense of how these services are used in practice, consider a quantitative asset manager overseeing thousands of separately managed accounts, each tailored to the individual client's preferences. With MSCI's Quantitative Investment Solutions, the manager can integrate tax optimization, sustainability preferences, and factor exposures into portfolio construction and rebalancing, while also enabling risk scenario analysis and swift adjustments to client mandates or market shifts. This allows for highly personalized portfolios to be built and managed at scale, with rules-based precision and responsiveness that would be difficult to replicate manually or through less integrated systems.

MSCI's Multi-Asset Class Analytics extends the segments capabilities beyond equities and into fixed income, currencies, commodities, alternatives, and private assets, integrating it into a single risk framework. This gives institutions a unified view of portfolio risk, including correlation effects, concentration risks, and diversification dynamics.

These tools are particularly valuable for institutions managing complex portfolios, such as pension funds, sovereign wealth funds, multi-asset mutual funds, and banks. Typical use cases are asset allocation decisions, stress testing, and scenario analysis, helping clients model exposures, simulate market shocks, evaluate counterparty risks, and drill down into specific portfolio segments.

When it comes to competition, MSCI faces a broader and more fragmented set of rivals in analytics than in its index business. Key competitors include SimCorp (owned by Deutsche Börse), BlackRock Solutions, Bloomberg, and FactSet. Additionally, several broker-dealers have developed proprietary analytics platforms for client use, while large global custodians, such as BNY Mellon and State Street, offer internal risk and performance analytics tools to their institutional clients.

Sustainability and Climate

While all parts of MSCI's business have shown steady growth, one segment has stood out in recent years: Sustainability and Climate. Though it currently accounts for 11% of total revenue, it has grown at a CAGR of nearly 30% since being reported as a standalone segment five years ago. Before that, it had long contributed to MSCI's Index and Analytics segments, providing sustainability-themed indexes and climate-integrated portfolio tools with ratings, datasets, and screening capabilities.

The foundations of this segment were laid in the late 1990s while MSCI was still a division at Morgan Stanley. In a 2023 episode of In Good Company with Nicolai Tangen, CEO Henry Fernandez recounted how MSCI's sustainability ratings were first established in 1999, sparked by a request from a portfolio manager at Storebrand (a Norwegian insurance company) who was pursuing socially responsible investing, as it was called back then.

The manager was looking for a benchmark to measure the performance of these types of investments, but no such index existed at the time. He asked MSCI to create one and, true to its forward-leaning mindset, the firm took on the challenge, taking the very first steps toward what would later evolve into MSCI's Sustainability and Climate segment.

While that early index and others like it remain part of MSCI's Index segment, the company has steadily expanded its broader sustainability capabilities. Much like its approach in analytics, MSCI has used targeted acquisitions to deepen its offerings in areas such as sustainability data, corporate governance analysis, and risk scoring.

Today, this segment helps clients incorporate environmental and social considerations into investment decisions, portfolio design, risk modeling, and regulatory reporting. These tools support analysis of long-term sustainability risks, carbon emissions, and climate transition scenarios, and are delivered through applications, APIs, and data feeds, mirroring the delivery of MSCI's other offerings.

The cornerstone product is MSCI's Sustainability Ratings, which assess how resilient a company is to long-term environmental and social risks, scoring firms relative to their industry peers. As of 2025, MSCI provides ratings coverage for over 10,000 entities. Its ratings aim to provide a standardized framework for comparing companies' exposure to sustainability risks.

Demand for these solutions has surged in recent years, fueled by regulatory mandates, rising stakeholder expectations, and a broader shift toward sustainable investing. Its clients, including global asset managers, insurers, banks, pension funds, and regulators, are all under increasing pressure to embed sustainability into their investment processes.

Similar to the analytics space, this segment operates in a fragmented market, where competing providers offer differing methodologies, and no clear dominant player has emerged. Some of MSCI’s largest competitors include Sustainalytics (owned by Morningstar), Institutional Shareholder Services (ISS) (majority owned by Deutsche Börse), S&P Global, Refinitiv (part of the LSEG), and Bloomberg.

The economics of financial infrastructure

MSCI's financial model is built on high-margin, recurring revenue across all of its core segments. The company earns licensing fees through long-term subscription contracts for benchmarks, analytics, and sustainability tools. These subscriptions make up the vast majority of revenue – 98% as of Q1 2025 – a figure that typically stays in the mid-to-high 90s. When client churn does occur, it's almost always due to structural changes like fund closures or M&A, not dissatisfaction. Voluntary departures remain rare due to the deep integration and switching costs associated with MSCI's services.

While most of MSCI's revenue is contract-based, a sizable portion comes from asset-based fees, primarily within its Index segment. These are tied to assets under management (AUM) in ETFs and other products that track MSCI benchmarks. Over the past five years, 22% to 26% of MSCI's annual revenue has been asset-based. While this stream naturally fluctuates with market performance and fund flows, it is largely stable, driven by long-term passive investment allocations.

Of MSCI's $2.9 billion in LTM Q1 2025 revenue, approximately 57% came from Index-related offerings. Around 40% of that was asset-based, with the remainder generated through subscriptions to its benchmark services. Although asset-based fees vary with market conditions, they're still considered recurring in nature due to the durability of the underlying products and mandates.

This revenue model enables an exceptionally scalable business structure. With almost no incremental cost to serve an additional client, MSCI expands smoothly with adoption. For a clearer view of profitability across its business lines, MSCI reports adjusted EBITDA by segment. The Index segment consistently delivers adjusted EBITDA margins above 70%, most recently reaching 76.6% in 2024. The Analytics and Sustainability and Climate segments, while smaller, also show strong operating leverage, with margins of 49% and 32%, respectively, and trending upward. Given its scale and superior margins, it's the Index segment that leaves the clearest imprint on MSCI's bottom line.

MSCI's revenue growth per segment since 2014.

This efficiency translates into robust free cash flow generation. MSCI's free cash flow margin has ranged from 45% to 53% over the past five years, supported by its asset-light model, low capital requirements, and recurring revenue streams. With virtually no additional cost to onboard new clients, much of each dollar earned flows directly through to free cash flow.

These features give MSCI a financial model that is not only scalable but built to perform across market cycles:

“MSCI has the capabilities and the business model to weather periods of global turmoil. Periods of market disruptions have always been when MSCI's clients need us the most. These are the moments when MSCI standards and solutions take on much greater importance for clients across segments, not just our benchmark indices and risk analytics, but also the full range of our integrated, interconnected tools and content. 88% of our subscription run rates come from clients who use multiple MSCI product lines. We provide mission-critical data, models and technology that clients need in all environments and all phases of the business cycle, but especially in periods of high uncertainty, low clarity and relative volatility in markets. This enables MSCI's all-weather franchise, robust cash flows and fortress balance sheet, and all of that makes us confident in our ability to deliver consistent financial results amidst the current market turmoil.”

Since launching its first indexes in the late 1960s, MSCI has played a foundational role in shaping how global investors understand and access markets. But in recent decades, driven by the rise of indexation and the trillions of dollars now benchmarked to its products, MSCI has, somewhat unintentionally, assumed the role of gatekeeper and flowmaster within the global financial ecosystem. Its rule-based methodologies have become essential infrastructure for large-scale capital allocation, giving technical decisions outsized influence over markets, economies, and capital flows.

As discussed earlier, MSCI's benchmark indexes serve as blueprints for a vast universe of investment products. Funds tracking these indexes, especially ETFs and institutional mandates, replicate their holdings and weightings with precision. When MSCI makes routine adjustments, such as rebalancing or swapping companies in and out based on size or liquidity, the effects are generally modest: a bit of sell pressure here, some buy pressure there, all in service of staying aligned with the index.

But not all updates are minor. MSCI's country classification reviews can have far-reaching consequences, often triggering sharp capital inflows or outflows. This is because many large allocators, sovereign wealth funds, pension plans, and other institutions tie their mandates directly to these classifications and must adjust their portfolios accordingly. An upgrade from Frontier to Emerging Market status, for example, can unlock significant new capital. Conversely, a downgrade can result in immediate outflows, with a recent case being Russia's removal from MSCI's Emerging Markets Indexes in 2022, when capital controls and trading restrictions rendered the market uninvestable.

Worldwide, governments and stock exchanges are well aware of MSCI's influence. Throughout times, regulatory bodies have often implemented structural reforms, improving liquidity, transparency, or foreign investor access, hoping such changes will lead to inclusion or an upgrade, and attract capital inflows. With the enormous amount of capital linked to MSCI's indexes, the incentives to align with its criteria are obviously substantial.

While MSCI's classification process is data-driven and rules-based, it carries substantial geopolitical weight. In this way, MSCI occupies a rare position in the financial system: a neutral but powerful facilitator whose decisions quietly steer global capital, shape investor behavior, and influence the economic trajectory of entire nations.

But with influence comes scrutiny, especially when index decisions intersect with politics, national policy, or questions of corporate responsibility.

China's 2018 inclusion into MSCI's Emerging Markets Index

Few events highlight MSCI's unintended geopolitical weight more clearly than the 2018 inclusion of China A-shares into its Emerging Markets Index. What began as a methodical, rules-based adjustment soon became a flashpoint in the debate over financial access, national security, and the role of global capital in geopolitics.

For years, Chinese officials had pushed for the inclusion of A-shares (stocks listed on the Shanghai and Shenzhen exchanges), which had been excluded due to longstanding concerns over market accessibility, capital controls, and transparency. While China was already classified as an Emerging Market, MSCI's indexes had previously focused on offshore-listed Chinese firms, such as H-shares (listed in Hong Kong) and ADRs (U.S.-traded American Depositary Receipts).

In 2018, after years of engagement and incremental reforms by Chinese regulators, MSCI announced it would begin adding A-shares to the index. The initial weighting of around 0.73% was modest (eventually increasing to approximately 4% by 2019), but the signal was significant: global investors now had index-based exposure to mainland China's equity market, marking the beginning of large-scale, benchmark-driven inflows.

The inclusion, however, drew sharp criticism. U.S. lawmakers, policy groups, and national security advocates expressed concern that passive investment flows would now be funneled into some Chinese companies that were state-owned or flagged for security or human rights issues. At MSCI's AGM in 2020, CEO Henry Fernandez was asked whether the company planned to exclude any companies that lacked any of these criteria in response to these concerns, but emphasized MSCI's neutrality:

“In general, I will say that all clients of MSCI around the world have a choice of any index benchmark they wish to use, pursuant to their stated investment objectives. Some of them may use our standard indices, which include all companies, whether it's state-owned or not state-owned and that are publicly listed, whether they are in China or in France or in the U.S., and those are the standard indices that we offer. If somebody wants to make a specific -- an explicit exclusion of a particular set of companies or countries, they would come to MSCI and ask us for a specialized, customized index, which we are always happy to provide, in order for them to have their own benchmark for their own investment objectives.”

Since its spin-off and IPO in 2007, MSCI has grown into a deeply embedded infrastructure company at the center of global investing. With a position built over decades, its scalable model, powered by a robust recurring revenue stream and long-term client relationships, has made it indispensable to financial institutions worldwide. As markets evolve, MSCI's position remains quietly, but firmly, intact.

)

)

)

)

)

)