)

)

)

Company research29 Apr 2026

Target Corporation: The Business Behind the Bullseye

How Target grew from a Minneapolis dry goods store into a retail giant, blending discount pricing with design and private-label power.

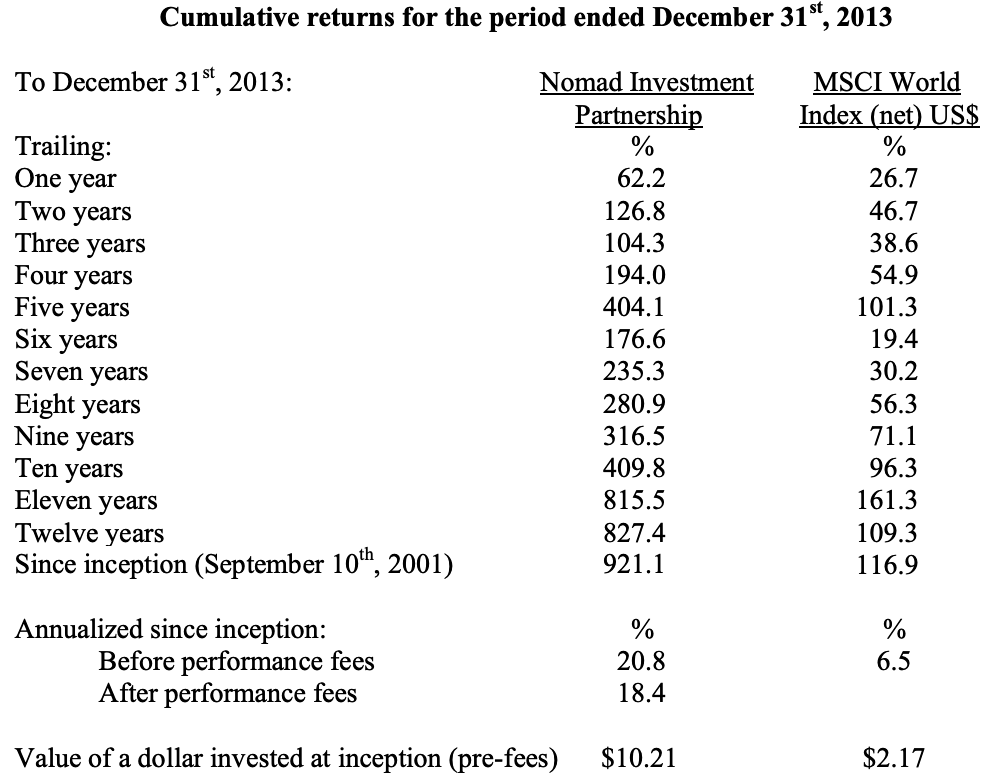

Investor Nick Sleep remains a mysterious figure in the world of investing and has avoided giving barely any interviews. He and his companion Qais Zakaria, together forming the Nomad Partnership, boasted an astounding 921% investment return between 2001-2014, dwarfing the MSCI World Index's 117% return during the same timeframe. For those curious about how Sleep and Zakaria produced this incredible return, the most hands-on insights are available through the Nomad Partnership Letters written by Sleep.

One of Nomad's most notable investments is Costco, a company adopting Sleep and Zakarias well-known concept of Scale Economies Shared. We've read every mention of this multibagger investment in the Nomad Partnership Letters, and it’s a best-in-class case study we think every investor can draw valuable lessons from.

Here’s his 2002 introduction to Costco:

“The retail concept is as follows: customers pay an annual membership fee (standard U$45) which provides entry to the stores for a year, and in exchange Costco operates an every-day-low-pricing strategy (EDLP) by marking up 14% on branded goods and 15% on private label with the result that prices are very, very low. This is a very simple and honest consumer proposition in the sense that the membership fee buys the customer's loyalty (and is almost all profit) and Costco in exchange sells goods whilst just covering operating costs. In addition, by sticking to a standard mark-up savings achieved through purchasing or scale are returned to the customer in the form of lower prices, which in turn encourages growth and extends scale advantages.”

Sleep describes this as “retail’s version of perpetual motion,” and once operations are set in motion, they’ll continue forever without additional energy required to maintain it.

Get curated quality company deep dives every other week.

Something that was extremely important to Jim Sinegal, the founder of Costco, was the EDLP strategy. Sleep explains this strategy through the story below, told by a company director:

“Costco bought 2m designer jeans from an exporter and shipped them into international waters and re- imported the jeans for an all-in price of U$22 or so per pair. This was U$10 less than the firm had sold the jeans for in the past (offering the potential for a 50% mark-up) and half the cost of most other retailers. One buyer recommended taking a higher gross margin than was usual (i.e., more than the usual 14% mark-up) as no one would know. Apparently Sinegal insisted on the standard mark-up, arguing that if "I let you do it this time, you will do it again". The contract with the customer (very low prices) must not be broken.”

This is not how retailers usually operate. They employ high-low price strategies instead, trying to influence store traffic by taking prices up and down. Sleep explains how confusing this proposition really is to the customer using an example of a bottle of shampoo. Is it worth $2 if the price is systematically reduced to $1 through couponing campaigns?

The strategy can even backfire according to Sleep, and he outlines how consumers should feel taken advantage of when paying $5 for tissues that they could buy for $4 last week. At Costco, the consumer knows – the price is 14% or 15% above the wholesale price, period.

This strategy has been described by Costco management as “easy to understand and hard to operate,” not surprising, as the temptation often is to mark-up the goods for maximized profit.

After introducing the business, Sleep laid out the Nomad investment case:

“Costco is profitable enough to self-fund growth of around 14% per annum and not to have to resort to leases for expansion […]. This means that growth will be more measured [...] and should be more sustainable. As to the potential for growth the firm has 21 stores in Washington State which houses just 2% of the US population. This density coast to coast implies room for around 1,000 US stores (currently 284) and 200 stores in the UK (currently 14) although planning regulations may not allow for this. Even then Home Depot, the largest DIY store in the US currently has 1,500 stores. At 10% growth per annum, this implies the firm has another 13 years of growth ahead. The share price has declined from a year 2000 high of $55 to $30 (Nomad’s purchase price) as margins declined slightly (they are measured in basis points at this firm) with the cost of several new distribution centers which will support the next few year’s growth. For example, in the UK the firm has warehousing and logistics capacity for 40 locations but only has 14 stores. At $30 the firm is valued as a cash cow, with higher levels of profitability (as capacity utilization increases) and modest levels of growth justifying a valuation over $50 per share. Costco is as perfect a growth stock as we have analyzed and is available in the stock market at a close to half price.”

Two years then passed, and in the 2004 letter Sleep returned to Costco again, now constituting 10% of Nomads assets, up from ~3% in 2002.

He shed light on the EDLP strategy once again:

“The act of purchasing membership has the effect of raising the company’s share of mind with the customer in the same way that consumer goods companies hope to achieve with conventional advertising. At Costco, the consumer has chosen to commit to the retailer. In other words, people shop at Costco because it is Costco, not because Costco stocks Coke. And the reason they shop is that goods are priced at a fixed maximum 14% mark-up over cost.”

The Costco mark-up is in aggregate twice as low as most supermarkets, and even Walmart marks up half as much as Costco. Making money at such low gross margins is an art in itself, and Sleep writes how Costco must ensure that:

1) Operating costs are very low, signified by the fact that the company measures its costs in basis points (there are 100 basis points in one percentage point).

2) That the wholesale price is as competitive as possible. How Costco negotiates this is by keeping the maximum number of items in a store (stock keeping units or SKUs) fixed at 4,000, and every spot is auctioned out to the supplier that provides the best value proposition. Here are Costco’s criteria for becoming a supplier, listed after setting the definitions of quality, pricing, packaging, and gratuities:

“We expect all vendors to consistently and voluntarily quote the lowest possible acquisition price available on all items. A vendor who does not consistently and voluntarily quote its lowest prices to our buyers will be permanently discontinued as a purchasing source for Costco.”

3) Revenues need to be very high. According to Sleep partly a self-fulfilling prophecy – revenues will be high if factors 1 and 2 are favorable.

When talking about network effects, most people mention Meta’s social media platforms or marketplaces like eBay and Amazon. What Nomad figured out, however, was that Costco’s customers, thanks to the company’s religious commitment to giving cost-savings back to them, experienced similar network benefits. Below, Sleep explains what Costco does with its scale advantage, very similar to the Amazon flywheel concept:

“In the case of Costco scale efficiency gains are passed back to the consumer in order to drive further revenue growth. That way customers at one of the first Costco stores (outside Seattle) benefit from the firm’s expansion (into say Ohio) as they also gain from the decline in supplier prices. This keeps the old stores growing too. The point is that having shared the cost savings, the customer reciprocates, with the result that revenues per foot of retailing space at Costco exceed that at the next highest rival (Walmart’s Sam’s Club) by about fifty percent.”

Something that Sleep and the Nomad Partnership probably are most recognized for is their scale efficiencies shared concept. He writes how many companies seek scale efficiencies, but few share them with customers. And it’s the sharing that he thinks makes the model so powerful. The paradox of growing more through giving more back:

“We often ask companies what they would do with windfall profits, and most spend it on something or other, or return the cash to shareholders. Almost no one replies give it back to customers – how would that go down with Wall Street? That is why competing with Costco is so hard to do. The firm is not interested in today’s static assessment of performance. It is managing the business as if to raise the probability of long term success.”

Sleep also updates us on the Costco investment case, beginning with explaining why growth stocks normally fail. It’s often because success encourages competition, and capital flows into industries to compete away excess returns. But what about those who don’t fail?

Sleep uses Michael Dell and the company that bears his name as an example. Dell succeeded by keeping costs low and passing back scale benefits to the buyer of its PCs. Doing this kept the company ahead of competition, and by the time competitors had matched in pricing, it had already moved on. So, whilst Costco continues to recycle cost savings to the customer, it’s lowering the probability of failure, according to Sleep.

He also shares three heuristics he thinks are the reason why Costco shares are mispriced:

“Heuristic One: “the company has low margins” (net profit margin is 1.7%, compared to Wal Mart at 3.6% and Target at 4.2%). True, but that’s the point. The firm is deferring profits today in order to extend the life of the franchise. Of course, Wall Street would love profits today but that’s just Wall Street’s obsession with short term outcomes. Heuristic Two: “it’s expensive at 24x earnings”. Really? Net income is a small residual, as discussed above. The firm could earn Wal-Mart margins by taking pricing up a little, in which case the firm would be on 11x earnings, but would it be a better business as a result? We think not, if it allowed the competition to catch up. Heuristic Three: “Costco has a cost problem”. Costs have risen as a percentage of revenues in the last few years due to the expense of a warehouse and distribution system associated with the next phase of the firm’s growth and the cost of employee benefits and insurance, especially in California. This has people fooled who really should not be.”

So, did Sleep consider Costco a perfect investment? Here’s his thoughts on what characteristics the most valuable company in the world would have:

“Such a firm would have a huge marketplace (offering size), high barriers to entry (offering longevity) and very low levels of capital employed (offering free cash flow). Costco has some of these attributes. The range of products is as wide as any retailer, and by-passing savings back it is building a formidable moat. It is also more asset light than its peers, but it is not the lightest of them all. For that one must turn to the Internet. In our opinion a business such as eBay could be the most valuable in the world. It has a huge marketplace, the biggest, an auction marketplace naturally aggregates to one player, offering high market share and high barriers to entry to the winner. Product pricing may be supported by the incumbent local newspapers and publishing businesses which have expensive machinery to replace and usually unionized labor and may provide a price umbrella for eBay. Better still eBay makes the customer pay for a high proportion of the assets used in the transaction such as PCs, modems, phone lines and so forth. But best of all, the incremental assets required to grow are so small. At Costco the firm will spend around U$15m per incremental store which will serve a radius of perhaps thirty miles. $15m is a lot of servers for eBay, and whilst we are not experts, that may be enough to serve some countries. So no, Costco is not perfect. Perhaps we should own eBay as well.”

This is very interesting considering that Nomad later bought a lot of Amazon with basically the same investment thesis.

In the 2005 letter, Sleep wrote about Nomad’s competitive advantage in investing, and cited a speech held by Bill Miller at Columbia Business School. Miller said:

“what you are trying to do as an investor is exploit the fact that fewer things will happen than can happen”.

And according to Sleep, that’s exactly what they aimed to do:

“We spend a considerable portion of our waking hours thinking about how company behavior can make the future more predictable and lower the risk of investment. Costco’s obsession with sharing scale benefits with the customer makes that company’s future much more predictable and less risky than the average business and that is why it is our largest holding. Our smaller holdings are less predictable but in certain circumstances could do much better as investments. We are just not sure that they will as their “cone of uncertainty” has a much greater radius than at Costco. Bill Miller got there years ago. We are just getting there today.”

Wonder about the moat of Costco? This comparison to Walmart – its closest competitor – sheds light on it:

“An analysis of the limited disclosure of financials at Sam’s Club suggests that the size of the distribution to Costco customers is so large that any attempt to match its prices would cost Sam’s somewhere in the region of US$1.4 billion annually while matching Costco’s pay scales would set them back another $750million. Such numbers are not insignificant even to Wal-Mart which last year earned net profits of US$9 billion. Such a chasm of competitiveness is, of course, difficult to capture using traditional analytical tools. After all, both Costco and Sam’s Club generate thin profit margins, both are growing revenues, and both are placing enormous pressure on traditional supermarkets and smaller wholesale clubs. But it seems inevitable that the long-term outcome for the two businesses will be significantly different particularly as measured by the growth of revenue per unit of selling space over the long-term. And Costco’s business model dictates that this competitive gap should expand over time as a fall in Costco’s relative asset intensity and increasing buying power will lead to greater scale efficiencies, which in turn are handed back to the customer in the form of lower prices. Game over.”

It’s evident that Sleep doesn’t like the high-low retailing model where the incentives clearly are misaligned. There, customers are trained to buy on a deal, be disloyal, and shop around, resulting in operating cost inefficiencies for the retailer. He likes the Costco model of scale economics shared more, which he described here in the 2008 letter:

“Scale economics shared operations are quite different. As the firm grows in size, scale savings are given back to the customer in the form of lower prices. The customer then reciprocates by purchasing more goods, which provides greater scale for the retailer who passes on the new savings as well. Yippee. This is why firms such as Costco enjoy sales per foot of retailing space four times greater than run-of-the-mill supermarkets. Scale economics shared incentivises customer reciprocation, and customer reciprocation is a super-factor in business performance.”

When analyzing potential investments it’s common to search for the one big thing that a company does right, explaining its success. Sleep discussed in the 2010 letter how he’s often hearing companies state: there’s no secret sauce or any one thing that we do special, but simply many, many things we do slightly better than others.

This is something he’s always waived off as a cover-up for the lack of any real competitive advantage, but taking Costco as an example, he declared he might have been wrong:

“Costco’s advantage is its very low-cost base, but where does that come from? Not from low-cost land, or cheap wages or any one big thing but from a thousand daily decisions to save money where it need not be spent. This saving is then returned to customers in the form of lower prices, the customer reciprocates and purchases more goods and so begins a virtuous feedback loop. The firm’s advantage starts with 147,000 employees at 566 warehouses making multiple daily decisions regarding $68bn worth of annual costs. It’s thousands of people caring about thousands of things a little more, perhaps, than may occur at other retailers.”

On the same note, Sleep remembers when he met Jim Sinegal, and he stopped mid-sentence and said “I must show you this.” What Sinegal showed was a memo from 1967 written by Sol Price, Fed-Mart’s founder (the predecessor firm to Costco). According to Sleep, the best summary of the business case for scale economics shared he’s come across:

“Although we are all interested in margin, it must never be done at the expense of our philosophy. Margin must be obtained by better buying, emphasis on selling the kind of goods we want to sell, operating efficiencies, lower markdowns, greater turnover, etc. Increasing the retail prices and justifying it on the basis that we are still “competitive” could lead to a rude awakening as it has with so many. Let us concentrate on how cheap we can bring things to the people, rather than how much the traffic will bear, and when the race is over Fed-Mart will be there”

As of 2023, it’s 56 years since that memo was written, and Costco could very well be considered the most valuable retailer of its type in the world. So in hindsight, it seems like Sleep indeed was wrong. Here’s his explanation:

“I had gone looking for what I thought ought to be there, a vivid smoking gun such as a brand name, a location, a clever re- insurance contract, or a patent. However, there is no a priori reason why a comparative advantage should be one big thing, any more than many smaller things. Indeed, an interlocking, self-reinforcing network of small actions may be more successful than one big thing.”

And to outcompete Costco or Amazon, for example, rivals would have to do not one thing, but millions of things better than they do – a way harder task.

Costco provides insights into what drives sustainable business growth and long-term shareholder value. Firstly, a relentless focus on delivering genuine customer value, rather than chasing short term profits, can create a defensible moat with high barriers to entry. While market trends may convert many into short-termists, focusing on the long-term can yield exceptional returns.

Secondly, Nomad’s investment in Costco signifies the importance of analyzing the underlying business and not only financial metrics. A quick glance at profit margins might point Costco out as a weaker player compared to its peers, but a deeper dive reveals its strategic decision to reinvest in the business and its customers.

Lastly, millions of small decisions can cumulatively create a company’s competitive advantage. Instead of seeking ‘one big thing’ that moves the needle, companies might do well to recognize the compounded power of countless better decisions made consistently over time.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)

)