)

)

)

Edge15 May 2026

TOMRA: Closing the Loop

The story of TOMRA: from reverse vending machine pioneer to global technology for deposit systems, recycling, and resource optimization.

Few companies have a name that so precisely describes their day-to-day operations as Waste Management. In the most literal sense, the company does exactly what its name suggests. But behind the bins and trucks lies an operation defined by immense scale and dense regulation, spanning thousands of assets, operating across an entire continent, and governed by rules that dictate what can be built, how it must be run, and who is allowed to operate. This is an inside look at the largest waste management company in the world.

A century ago, Americans dumped their waste wherever they could, with limited oversight or consequence. As populations grew and cities expanded, trash collection shifted from an inconvenience to a necessity and eventually into a business. Although structures and implementation varied significantly across the nation, the trend was increasingly that waste ended up at the same destination: a centralized dumping site. The industry's early fragmentation, weak oversight, and steady cash flow often attracted criminal involvement, but over time, decades of regulation formalized the industry and shifted control of waste toward legitimate businesses.

Out of that process emerged one of the most stable business models in the American economy, and, eventually, the company now known as Waste Management (WM). What looks like a boring business on the surface is, in reality, a story of expansion, consolidation, and remarkably reliable returns. Trash is unavoidable and predictable, and scale within the industry confers enormous advantages. Over time, WM built a vertically integrated empire spanning collection, transfer, landfills, and resource recovery, touching every point of the waste value chain.

Before we go back to the 1960s, it's worth fast-forwarding to 2026 to see what scale and integration have produced at WM over the years.

)

We begin the story in the late 1960s Illinois with three businessmen, H. Wayne Huizenga, Dean L. Buntrock, and Larry Beck. All three operated small garbage collection businesses, and seeing the opportunity in combining their operations, they merged into a single company. Perhaps more focused on the task at hand than wanting to spend three weeks debating what to call their new venture, they chose the very practical name Waste Management.

The trio didn't waste any time, and right from the start, WM grew with astonishing speed. The combination of their businesses delivered instant scale, generating $5M in revenue in that first year, while also fueling growth through the acquisition of roughly 20 smaller companies that expanded its garbage empire. The trend continued into the following years, and in June of 1971, Buntrock, who was serving as President and Chairman, took the company public. The IPO raised around $4M, and the capital was immediately put to work.

Having seen the benefits firsthand when they merged their own businesses, the founding trio continued on that acquisition-led growth, bringing clear economies of scale. By consolidating routes and standardizing operations, WM could operate profitably while navigating the increasingly complex regulatory landscape more efficiently than small regional players could.

Within 18 months of the IPO, the company acquired around 75 small-scale, local trash haulers from Chicago, through the East Coast, and all the way down to Florida. As a rule, the owners were bought out using WM stock, while being kept on as managers. By the end of 1972, WM was operating in a total of 19 states. What had started as a regional patchwork of small, local operations was quickly scaling into a wide network of routes, customers, landfills, and trucks.

To bring more synergies to the constantly scaling organization after its acquisition-led growth, it also strategically added operations to increase vertical integration. At a time when many haulers paid to dump their loads at facilities owned by others, WM prioritized ownership, steadily expanding its portfolio of landfills and disposal sites. While many of those early sites have since been closed, the strategy itself has proved enduring and a central driver of its long-term success.

Beginning in the 1970s, a formal regulatory framework took shape, replacing fragmented and uncoordinated waste management practices across the United States. While disruptive at the time, these changes ultimately established the industry's modern rules, many of which have benefited WM and its large competitors over the years. We'll return to these environmental protection acts later and their lasting impact on industry dynamics.

No matter which numbers you look at – amount of landfills, companies acquired, routes, revenue, or just about anything else – growth during the 1970s was striking. Through aggressive expansion, Waste Management became the largest waste hauler in America by 1980. The company was perfectly positioned to to benefit from a gradual but persistent increase in household waste, as population growth and rising consumption expanded the volume of trash Americans produced.

Driving this success was the leadership's near-religious focus on expansion. Huizenga and Buntrock had proved to be masters at identifying underpriced local haulers and persuading their owners to sell for stock, rapidly adding to WM's ever increasing network. “Route density” became the guiding principle, and the concept itself is very straightforward: increase the number of customer stops along each truck's route.

Owning and operating landfills quickly became a competitive advantage in its own right. Not only did this eliminate tipping fees, but the value of these assets has only increased over time as environmental regulations made new landfill development increasingly difficult.

By offering a complete solution to municipalities and industrial customers in need of reliable services, WM won lucrative contract after lucrative contract, while constantly modernizing its operations. Early innovations included the use of standardized steel trash containers and hydraulic compactors, allowing for faster (and cleaner) collection.

By the early 1980s, Waste Management was riding high, having experienced revenue growth of nearly 50% annually through the 1970s. The complex regulatory changes were beginning to have a significant impact on the industry, and WM's scale and experience meant that it could quickly turn compliance into operational advantages, making it an early nationwide leader. The momentum continued into the following decade as WM was looking to broaden its services and expand its business into new markets.

First and foremost, the company was going international. While it had been operating in Canada since the early 1970s, it was now looking to expand outside North America. The first contract came from Saudi Arabia, and throughout the following years, WM added clients in countries close to their own shores in Venezuela, all the way to Australia. The leadership had taken a gamble on the fact that its formula could work overseas, and early results appeared to vindicate that bet. By 1990, it had operations in over 20 countries.

The new strict regulations of handling toxic and chemical waste also proved to create an opportunity for WM, as everyone from big manufacturers to the Department of Defense was in need of these services. WM happily swooped in and won contract after contract. By the mid 1980s, the company had become the nation's largest handler of hazardous waste, and dealing with the toxins and chemicals had, in just a few years, expanded to a sizable part of the company's revenue.

In 1986, Waste Management launched a program aimed at extending services into recycling. Never having been the ones for a convoluted name, WM called the program “Recycle America” and got to work.

Curbside recycling was gaining traction across the country, and municipalities that once paid only for trash collection were increasingly willing to pay for diversion programs, or at least demand them as part of a broader contract. In order to protect its relationships with municipalities going forward, recycling had to be part of the deal. By the end of the 1980s, Recycle America had grown into the nation's largest recycling program, serving over a million households through curbside pickup of recyclables.

Going into the 1990s, Waste Management increasingly described itself as a “full-line environmental services” provider. No longer just hauling garbage, but a one-stop shop for waste reduction, recycling, and sanitation services.

In 1993, the company rebranded as WMX Technologies, Inc., turning itself into a holding company. Its traditional waste collection and landfill business continued to operate as Waste Management, Inc., but it now sat alongside four other publicly traded subsidiaries, each focused on a different corner of the environmental services market.

These included Chemical Waste Management, which handled hazardous and toxic materials; Wheelabrator Technologies, which ran waste-to-energy and treatment facilities; Rust International, focused on engineering and environmental remediation; and Waste Management International plc, which housed the company's overseas operations.

In theory, the structure created a portfolio of specialists: a core solid-waste business complemented by businesses designed to tackle more complex and regulated problems. Together, this attempt cemented WMX's vision to present itself as not just a waste management business.

At first glance, the structure made sense. In practice, it proved far more fragile than it appeared.

As the economy began to face a downturn and commercial activity slowed, industrial waste volumes decreased, and customers deferred expensive environmental projects. WMX's subsidiaries were capital-intensive, heavily regulated, and dependent on steady project pipelines, conditions that evaporated in a slowdown. Its new structure may have supported diversification, but it proved to concentrate risk. In 1993, for the first time in its history, WM's revenues declined, and profits fell 47% year-over-year.

WMX was forced to respond. In 1994, COO Phillip Rooney announced plans to shed $1B of assets. Some listed subsidiaries were sold, while others were pulled back in-house after their share prices collapsed. What was meant to unlock value through specialization instead created complexity, market confusion, and less flexibility when conditions turned.

However, the core business itself remained intact. WM still operated hundreds of collection centers, tens of thousands of trucks, hundreds of landfills, and extensive recycling operations. But the mood around the company had changed. Scale was no longer an automatic proof of future success.

In June 1996, after 28 years as CEO, Dean Buntrock stepped down and handed the role to Phillip Rooney. WM's next chapter would require a focus on streamlining and execution rather than grand reinvention. At the time, activist investors, including George Soros, began pushing for more radical change. While critical of some of the more recent strategic choices, some also questioned the integrity of management.

That suspicion and unease ultimately led to Rooney's departure just months into the role. The concerns, as it would turn out, were not unwarranted and once the full truth came out, it would become one of the era's biggest accounting scandals.

In early 1997, the board brought in an outsider, Ronald T. LeMay, formerly a top executive at Sprint, to serve as CEO and inject fresh discipline. But LeMay lasted only a few months, abruptly quitting after (reportedly) discovering accounting irregularities.

The board then turned to Robert C. Miller, a turnaround specialist known for steering companies through crises. Miller took charge in late 1997 and would soon deliver crushing news. In February 1998, the company announced it would restate earnings for the past five years, from 1992 through 1997. The restatement revealed $1.7B in overstated earnings. In addition, the company took a $3.54B one-time charge to write down overstated assets and unwind years of improper accounting.

For years, top executives inflated earnings through aggressive and improper accounting. Expenses were understated and asset values overstated, most notably by depreciating garbage trucks and dumpsters far too slowly, as if the equipment would last years longer than it realistically could. Additionally, landfill costs that should have been expensed or written down were improperly capitalized, keeping inflated asset values on the balance sheet.

Regulators quickly identified who had driven the culture that allowed the fraud. The SEC described Dean Buntrock as the driving force, alleging that he set earnings targets and fostered pressure that pushed accountants to make the numbers look good. Phillip Rooney was also implicated, along with CFO James Koenig and other top finance executives who were accused of orchestrating the scheme. Beyond management, the company's auditor, Arthur Andersen, was cited for its role in approving accounting practices that allowed the misconduct to continue over the years.

The accounting scandal did not erase Waste Management's underlying asset value, but it clearly weakened the company's leadership, credibility, and ability to operate from a position of strength. The Houston-based USA Waste Services had been rapidly acquiring regional waste companies throughout the 1990s, and saw a once-in-a-generation opening. In March 1998, barely a month after the restatement, USA Waste announced a deal to acquire WM for roughly $15B in stock and assumed debt.

The deal was stunning in its reversal of roles: USA Waste was acquiring a company nearly four times its size. While technically an acquisition, the transaction in practice looked more like a merger of equals. WM shareholders would own 60% of the combined company, but control would shift to USA Waste's management team. The combined entity would keep the Waste Management name since it was too valuable to discard, but the headquarters would move from Oak Brook, Illinois, to Houston, Texas. The merger closed in July 1998, creating a company that controlled roughly 20% of the U.S. waste market.

For a brief period, it appeared the company had found its reset. New leadership promised discipline, the accounting cleanup was underway, and the combination of operations brought scale advantages that few competitors could match.

That optimism proved short-lived.

On July 6, 1999, WM shocked the market by warning that it expected to fall about $250M short of its Q2 revenue targets. More troubling than the size of the shortfall was management's admission that it lacked clear visibility into where performance was breaking down. Investor confidence collapsed, and the stock fell 37% during that single day.

In the months that followed, pressure continued to build as it seemed that many of the issues that had led up to the merger had not been fully resolved. That creeping realization made this episode more damaging than the earlier scandal. Investors had believed the company was past its troubles and ready to turn the page, only to discover that the same underlying problems still lingered within the combined business.

As integration continued to progress, it became clear that key assumptions underpinning asset values, particularly around landfill lives, capitalized costs, and acquisition returns, had remained overly optimistic. In October 1999, WM recorded a $1.23B pre-tax charge to write down overstated assets and goodwill. While smaller than earlier clean-up charges, the signal was nonetheless devastating. Between July and October, the stock fell roughly 75%.

Another management change followed, along with a familiar promise of stability. This time, the shift was explicit: growth would come from integration and discipline, not structural experimentation. Waste Management pulled back from expansion and focused on consolidating what it already owned, bringing fragmented businesses together while prioritizing debt reduction.

Non-core assets were sold, including the international operations that had once been central to the WMX vision. The proceeds were used to strengthen the balance sheet and reduce the sense that the company was perpetually one downturn away from another crisis.

By 2002, the business had stabilized and returned to growth. During the years that followed, WM focused on operational efficiency, steady improvements, and polishing its identity as an environmentally responsible firm. The company had learned, painfully, that reckless expansion and weak controls could jeopardize its dominant position.

While WM remained the dominant force in the U.S. waste management industry, that position was threatened in 2008. This time by external forces rather than internal missteps. Republic Services, the second largest waste company, announced a merger with Allied Waste Industries, the number three. WM soon inserted itself into the mix, launching a bid for Republic. Publicly, the company framed the move as a strategic opportunity. Privately, some observers questioned whether the offer was as much about blocking the creation of a stronger rival as it was about completing a deal.

But as the global financial crisis intensified and credit markets froze, WM ultimately withdrew its bid. In line with its new disciplined identity, management said it was unwilling to pay any price that might undermine the financial stability it had worked to restore. The withdrawal cleared the way for Republic and Allied to merge, creating a more formidable number two.

While the company avoided takeovers of its largest competitors in the 2010s, it continued to build scale through organic growth and the acquisition of smaller regional operators across North America. At the same time, WM leaned into selective innovation and measured service expansion, investing in landfill gas recovery systems that captured methane from decomposing waste and converted it into energy. While landfill gas capture itself was not new, the emphasis on upgrading these systems to produce renewable natural gas (RNG) was.

The fleet was modernized as well, as WM took early steps toward more automated collection and began shifting trucks from diesel to compressed natural gas, a cleaner-burning fuel. Recycling also grew, with the company adding several materials recovery facilities (MRFs) equipped with advanced automation technology.

Together, these moves slowly redefined the company's identity. From a scale-driven waste hauler to an integrated environmental services operator focused on efficiency, recovery, and emissions reduction. That evolution was eventually formally sealed in 2022, when the company rebranded itself simply as WM. Efforts to anchor the rebrand around WM as a broader, more integrated business have only intensified in the years leading up to 2026. Today, the company operates as a vertically integrated waste infrastructure provider, spanning the full value chain.

America's waste management industry is a product of events leading to regulation. In the second half of the 20th century, environmental failures, public health crises, rapid urbanization, and growing scientific understanding of contamination pushed lawmakers to formalize how waste was handled, transported, and disposed of. That framework still defines the industry's foundations: who can operate at scale, where capital must be deployed, and why the market looks the way it does today.

Beginning at the federal level, the regulatory framework rests on four pillars: RCRA (1976) for operational standards, CERCLA (1980) for environmental liability, and the Clean Water Act (1972) and Clean Air Act (1970) for emissions control.

Together, these laws set the baseline. In practice, enforcement and implementation largely fall to states and municipalities, which often impose requirements more stringent than federal minimums. The result is a patchwork of permits, operating standards, and compliance obligations that vary by jurisdiction. For companies operating at a national scale, that means navigating several regulatory environments at once, favoring operators with deep expertise, established systems, and institutional scale.

One consequence of the regulatory framework is that landfills have evolved into critical infrastructure assets. The open dumps of the past, without structure and oversight, are now illegal and replaced by regulated landfills that operate under tightly engineered systems and procedures. Building and operating one is capital-intensive and requires commitments that extend decades into the future. Sites must incorporate liners and containment systems, follow prescribed operating controls, and undergo continuous air and water monitoring. Closure plans are defined from the outset, with post-closure obligations often lasting more than 30 years after a landfill stops accepting waste.

Everything is designed around two objectives: protecting the surrounding environment and maximizing airspace. That airspace, the permitted volume of waste a landfill is allowed to accept, is the ultimate determinant of the asset's value. It's a finite, depleting inventory, and how efficiently it's managed largely determines the long-term economics of the site.

Permitting authority is fragmented across multiple layers of government. Federal standards are implemented and enforced by state environmental agencies, while local zoning boards and land-use authorities control whether new landfills can be built or existing ones expanded. Together, these overlapping approvals effectively cap disposal capacity in each region. Securing permits often takes a decade or more, involving extensive environmental impact studies, financial assurance requirements, and public hearings where community opposition can lead to litigation and multi-year delays. As a result, operators overwhelmingly prefer expanding existing sites rather than attempting to permit new ones.

After decades of operations, when an area's permitted landfill capacity is filled and closed, there is no guarantee that new capacity will replace it. In fact, the trend in many markets is toward declining disposal capacity, where existing landfills close while community opposition and regulatory complexity prevent new development. Therefore, the remaining permitted airspace is progressively more valuable.

These dynamics make disposal both indispensable and scarce. Every waste hauler needs access to landfill capacity, but owning it requires significant upfront capital and commitments that span permitting, operations, and decades of environmental liability. The imbalance between universal need and a finite set of permitted assets creates the industry's central bottleneck and its most durable barrier to entry.

The regulatory complexity described above has fundamentally reshaped the U.S. waste management industry. What was once a municipal service handled directly by local governments has increasingly shifted to private operators. The capital requirements, technical expertise, and long-term liabilities proved difficult for many municipalities to manage as standards tightened. Maintaining compliance across multiple jurisdictions requires dedicated legal, environmental, and operational systems: capabilities that are costly to build and only economically viable at scale. Today, municipalities typically retain responsibility for ensuring service but contract private operators to deliver it, creating a base of long-term agreements that contributes to the industry's stability.

This environment has produced a distinct industry structure where a relatively fragmented collection is paired with highly concentrated disposal. While thousands of small and regional haulers still operate, large integrated operators – led by Waste Management, Republic Services, and Waste Connections – increasingly dominate both ends, winning most municipal franchise agreements for collection routes while controlling the permitted landfills that all haulers ultimately depend on. That vertically integrated model, designed for national scale, has inevitably fueled consolidation, a theme as relevant earlier in the story as it is today.

An industry built entirely on regulatory frameworks might sound vulnerable to disruption or sudden policy shifts. But given the complexity we've outlined, these regulations function less as a source of risk and more as a competitive moat, reinforcing stability for established operators. Regulatory change tends to be incremental, unfolding over years and allowing those with scale and expertise to adapt while raising the bar for everyone else.

This is the environment WM operates in. The company's scale, asset footprint, and operating model are best understood as responses to this regulatory landscape and as a way to turn these constraints into durable competitive advantages.

People talk about disrupting this industry and this company but boy, we have a deep, wide competitive moat.— Jim Fish, CEO of WM

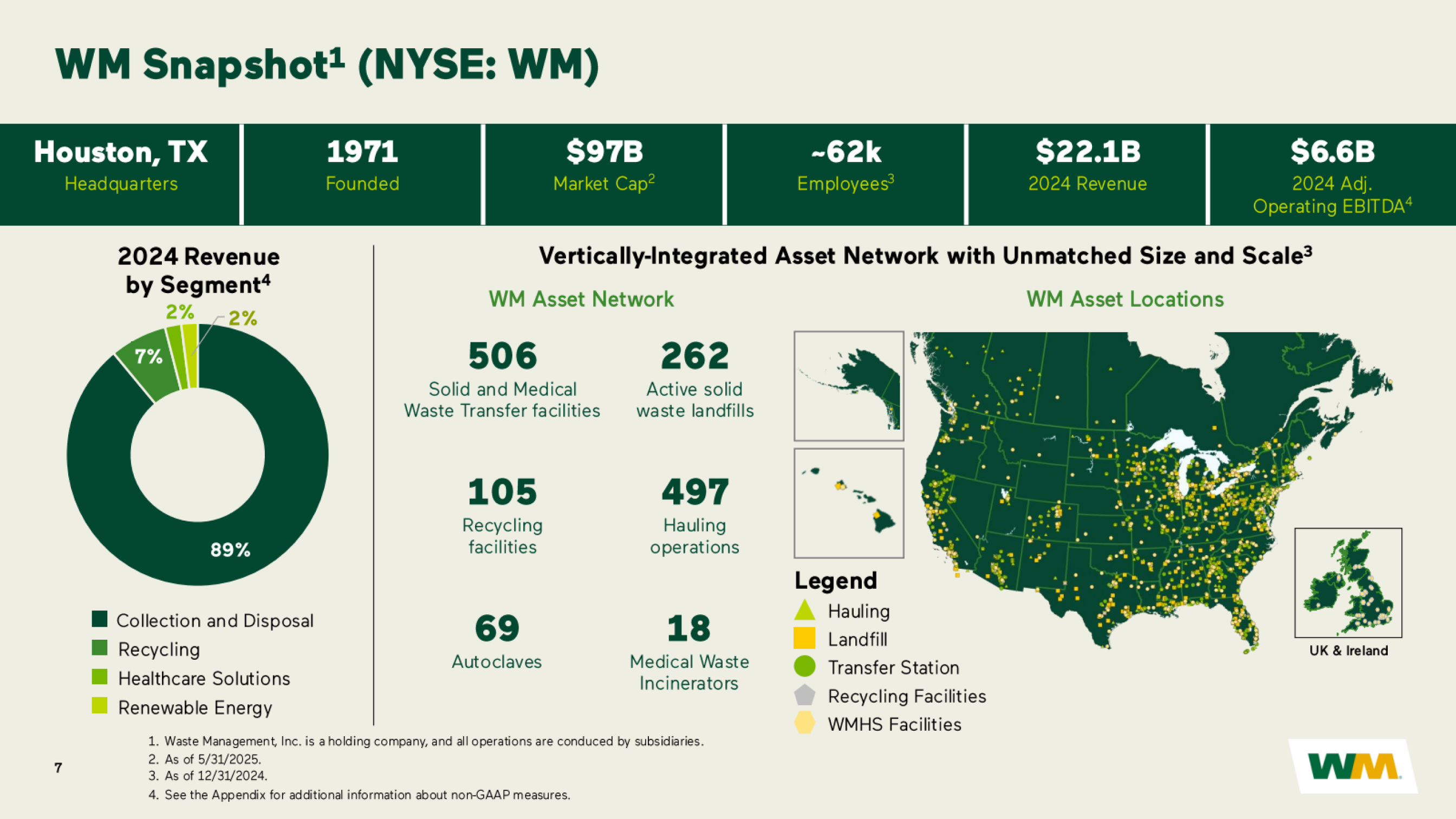

In 2026, Waste Management sits at the center of North America's waste infrastructure, operating a vertically integrated model designed to capture value at every stage of the waste lifecycle. The company owns or operates 257 solid waste landfills and four secure hazardous waste landfills, representing the largest network throughout the United States and Canada. Supporting that final disposal are 339 transfer stations and 105 recycling facilities, while landfill gas-to-energy projects operate at 102 of the company's landfills.

That footprint supports a business generating $24.8B in trailing twelve-month revenue as of Q3 2025. Collection is the engine of the model, providing the bulk of revenue across commercial, industrial, and residential customers, while disposal-related activities complete its value chain with its owned landfills and transfer infrastructure. Beyond core solid waste, recycling, renewable energy, and healthcare waste are smaller in absolute terms, but they expand the platform's breadth and represent important sources of long-term strategic value.

)

The strength of this model lies in how the revenue streams connect. Central to that connection is internalization, the routing of waste collected by WM's own trucks through its own network of transfer stations and landfills rather than relying on third-party disposal. Vertical control allows the company to earn margin at multiple points along the chain: collection, transfer, transportation, and ultimately landfill tipping. Each incremental improvement in internalization turns what would otherwise be an external cost into retained margin within WM's system.

WM's operations span the United States and Canada, organized into two geographic segments: the East Tier (Eastern U.S., Great Lakes, and most Canadian provinces) and the West Tier (Western U.S., upper Midwest, and British Columbia).

As mentioned earlier, WM entered Canada in the early 1970s and has expanded steadily since. While Canada operates under a different regulatory framework, the underlying structure is similar: provincial agencies implement federal environmental standards while municipal authorities control land use and franchising. Geographic proximity creates operational advantages as well, allowing waste collected near the border to flow to the closest WM disposal facility on either side, improving internalization and asset utilization across the network.

This North American focus is shared by the company's closest peers. Republic Services, with roughly $16.5B in revenue, operates exclusively in the United States, while Waste Connections, with approximately $9.4B in revenue, serves both U.S. and Canadian markets.

As WM learned during the turn of the century, replicating decades of infrastructure accumulation and regulatory relationships in markets with different frameworks offers very limited economic appeal. For capital-intensive operators where scale and internalization drive returns, competitive advantage lies in deepening control within existing markets – particularly as abundant consolidation opportunities remain across North America.

Collection services represent the front end of Waste Management's operations and the company's largest single revenue source at $15.4B on a trailing twelve-month basis as of Q3 2025, representing 62% of total revenue. The company operates roughly 15,500 collection vehicles across the United States and Canada, serving commercial, industrial, and residential customers daily.

Commercial customers includes offices, retail stores, restaurants, hotels, and schools, and represent the largest segment at 36% of Collection revenue. Industrial customers, encompassing manufacturing facilities, factories, and large-scale operations, account for 20%. Residential collection, serving households through either municipal franchise agreements or direct subscriptions, makes up 23% of Collection revenue. The remaining 21% comes from other collection services, primarily roll-off dumpsters, construction and demolition cleanup, municipal and public-space services, and other project-based or episodic work.

While service structures vary by customer type, the common feature across Collection is long-term contracting. Commercial and industrial customers typically enter three-year service agreements, with pricing based on factors such as collection frequency, container type, waste volume, distance to disposal facilities, and local market conditions. These contracts provide recurring, predictable revenue while allowing for periodic pricing adjustments.

Residential collection is governed largely by contracts or franchises granted by municipalities and regional authorities, typically lasting three to ten years, in line with state statutes. These agreements often grant WM exclusive rights to service all or part of a defined area. Alongside franchise-based service, the company also offers direct monthly subscriptions to individual households.

Collection has long been a labor-intensive business, but it is becoming more efficient through automation. WM has been reducing that cost by transitioning from traditional rear-load trucks, requiring both a driver and a helper, to automated side-loader vehicles operated by a single driver. The company has set a target of eliminating approximately 2,000 helper positions through this conversion from 2022 to 2026, achieved through attrition rather than layoffs, given the high turnover typical of these roles. As of mid-2024, it was roughly halfway through that target.

These vehicles eliminate the helper position and can service roughly 30% more homes per route than traditional rear-load trucks. Each conversion pays for itself in approximately one year through labor savings and productivity gains. Given that collection vehicles sit at the operational core of the business and labor has historically been the largest cost component, these productivity gains have a meaningful impact on margins over time.

Although Waste Management's landfills operations only make up roughly 15% of total revenue, it is unquestionably the company's most important asset, both literally and strategically. The barriers to building and operating landfills described earlier – the capital intensity, regulatory complexity, and decades-long obligations – form the economic foundation that makes existing landfills so valuable. WM's 257 solid waste landfills represent the largest disposal network in North America and serve as the center of gravity for its integrated business model.

Each day, these sites receive and compact waste to maximize the use of permitted airspace. As previously mentioned, every landfill is authorized to accept a defined volume of waste, measured in cubic yards and determined by its engineered final topography. The permitted airspace is monitored through regular surveys that compare the current profile of the landfill to its approved design.

The value of that asset is driven by scarcity, which translates directly into pricing power that varies widely by region. Disposal fees, commonly referred to as tipping fees, are charged per ton of waste accepted and reflect local conditions shaped by land availability, regulatory constraints, and competitive alternatives. Pricing also incorporates the capital required to build, operate, and eventually close a landfill, the type of waste being deposited, and prevailing market dynamics.

Tipping fees apply to both internalized and external volumes. When WM's own trucks deliver waste to WM-owned landfills, the tipping fee is an internal transfer that nets out at the consolidated level but improves margins by keeping disposal economics within the system rather than paying third parties. In addition, WM generates revenue by accepting waste from third-party haulers that lack their own disposal infrastructure.

These dynamics lead to sharp regional differences. In parts of the South and Midwest, where capacity is more abundant and land costs are lower, tipping fees may range from $30 to $40 per ton. In contrast, heavily constrained northeastern coastal markets can see fees exceed $100 per ton. The regulatory framework acts as a protective moat around existing capacity, making new landfill development extremely difficult in many markets and driving higher utilization and pricing at the remaining sites.

Beyond the $3.7B in disposal fees generated on a trailing twelve-month basis as of Q3 2025, many of these sites also generate incremental value through gas-to-energy, adding a sustainability-linked revenue layer to landfill assets. We'll return to this in more detail later.

Landfill airspace is a precious commodity.— Jim Fish, CEO of WM

Because of landfill scarcity, managing airspace to maximize landfill asset value is a constant strategic priority for Waste Management. At the site level, the company deploys technology to monitor gas production, leachate management, and critically, airspace utilization. These systems guide real-time decisions on waste placement, compaction, and routing to extract maximum capacity from permitted airspace, while maintaining environmental compliance.

The objective sounds simple but is operationally complex: fill every cubic yard of permitted space as densely and efficiently as possible, treating the landfill less as a dumping site and more as a three-dimensional inventory that must be optimized down to the last inch.

Over the long term, airspace management also means expanding existing landfills, either by adding adjacent acreage or increasing permitted height. While these expansions require navigating a similar multi-layered approval process described earlier, it's far more worthwhile than permitting entirely new sites.

Existing landfills already have infrastructure in place and, in many cases, established community acceptance. WM actively pursues expansions at multiple sites. This strategy has proven successful over the years, with the company receiving expansion permits at 12, 13, and 11 landfills over the past three years. As of year-end 2024, the company was seeking expansion permits at 18 sites.

Over the past decade, Landfill revenue has grown steadily from $2.9B in 2015, reaching $3.7B on a trailing twelve-month basis as of Q3 2025. That 28% growth is put into perspective as it was achieved with minimal expansion of the landfill footprint, as it only added 13 net new landfills during this period. Instead, it was the result of extracting more value from its existing asset base by obtaining expansion permits at current landfills, maintaining pricing discipline to drive higher revenue per ton, and implementing operational improvements such as enhancing airspace utilization.

As of year-end 2024, WM's landfills held an estimated 5.3 billion tons of remaining permitted capacity, representing a weighted average remaining life of approximately 39 years based on projected disposal volumes. That runway translates into decades of reliable cash flow from assets already in place, without the cost and risk associated with developing new sites. As industry-wide disposal capacity continues to decline, the value of that runway increases.

Approximately 400 U.S. landfills are expected to close by 2040, a substantial reduction from the current 2,000 active municipal solid waste sites. These market dynamics favor the large-scale operators, all well-positioned with nationwide operations and multi-decade permitted capacity runways. As landfill capacity becomes scarcer and new development remains challenging, the structural advantages of continued industry consolidation of the previous decades are likely to persist.

“Businesses love -- would love to be in the same position we're in, having a deep, wide moat around your business, makes it really tough for somebody to kind of make their way in and disrupt you. And people talk about disrupting this industry and this company but boy, we have a deep, wide competitive moat.”

– Jim Fish, CEO of Waste Management, at its 2025 Investor Day (sourced through Quartr Pro).

While Collection and Landfills generate the bulk of revenue and house the most visible assets, its Transfer segment serves as the connective tissue that allows Waste Management's system to function efficiently at scale. As of 2025, the company operates 339 transfer stations across the United States and Canada.

These facilities consolidate waste from multiple collection routes before loading it onto larger transfer trucks, rail containers, or barges that can transport significantly greater volumes per trip to distant landfills. This consolidation fundamentally changes the economics, allowing collection trucks to operate on short, local routes rather than driving 50-80 miles to a landfill and back, wasting fuel and tying up expensive equipment and labor in unproductive travel time.

Although transfer stations sit upstream of final disposal, they function in many ways like landfills. They serve as designated intake points for waste, accept material from both WM and third-party haulers. As of Q3 2025, WM's transfer network generated $1.5B in revenue on a trailing twelve-month basis, with pricing mechanisms similar to those of landfill operations.

Strategically, transfer stations are important to profitability due to their direct impact on internalization and their role in connecting WM's post-collection network. President and COO John Morris discussed that connecting tissue at its 2025 Investor Day:

“And one of the keys for us today, we internalize about 70% of our entire waste stream now. We view our ability to continue to do that and frankly, internalize more waste over the long term is going to be driven by the value of our post-collection network. How do we connect all the nodes on the post-collection network, those 350 T stations with the transportation network, which is truck, rail and water and get that and be able to access our sites for decades to come. And that's one of the things we're working on very diligently as we speak now.”

This infrastructure is particularly important in urban markets where direct haul economics often break down. In major metropolitan areas, landfills are typically located far from population centers due to land constraints and regulatory barriers. John Morris highlighted this dynamic at the Goldman Sachs Industrials and Materials Conference in 2023:

“The landfills, they're becoming fewer and further between, right, which means the ability to access those sites is going to be more reliant on a really resilient, robust transportation network. We do a ton of business with the city in New York here for the last 25 years. And if you live in the city here, you know that it all leaves by boat or by rail and it goes some place, and it takes a long time and a lot of miles to get there. The transfer piece and the strength of the network is becoming more and more important, especially in a major market like New York or Philadelphia or South Florida.”

Without transfer stations to consolidate waste for efficient long-haul transport, these dense urban markets would be economically impractical to serve. But their role extends well beyond dense cities. Across the network, transfer stations feed WM's landfills and enable internalization even in regions where direct haul distances are inefficient rather than impossible.

WM's investments in transfer infrastructure also tie directly into landfill value maximization. Waste routed through the transfer network can be directed to the landfill best positioned to accept it, based on remaining airspace, proximity, pricing, and long-term capacity planning. Higher-margin waste is preserved for scarcer, higher-value sites, while more commoditized volumes flow to landfills with ample capacity.

These investments have steadily increased WM's internalization rate, from roughly 66-68% between 2019 and 2023 to over 71% by mid-2025. Each incremental point of internalization lifts consolidated margins and cash flow by capturing value at multiple touchpoints rather than paying third parties.

To push internalization further, WM focuses on strengthening its network, where collected waste still lacks efficient access to owned disposal assets. Transfer infrastructure investments are evaluated based on their ability to “unlock” that waste, whether through new facilities, expanded consolidation capacity, or tuck-in acquisitions that add density in existing markets.

Roughly half a century ago, waste disposal often meant open dumps and unlined landfills with limited environmental safeguards, but as regulations tightened disposal became a controlled, engineered process built around monitoring and long-term compliance. Over time, those shifts, combined with technological advances, opened up new ways to extract value from waste.

Waste Management has over the years folded these newer use cases into its integrated system, with services beyond basic collection and disposal steadily becoming more meaningful parts of the offering. Partly because they generate incremental economics, but also because they allow WM to cover more of the waste and sustainability value chain for customers.

WM can bundle collection with tools and services that larger commercial and industrial customers increasingly expect, including data analytics (such as its WM elements platform), recycling brokerage, hazardous waste solutions, renewable energy, and sustainability reporting. And because the company operates across North America, it can deliver that package at scale for customers with multi-site footprints, without forcing them to employ different regional providers.

Ever since WM introduced these sustainability-oriented businesses into its offering, they have grown alongside the core operations. As of Q3 2025, Recycling Processing and Sales and WM Renewable Energy generated approximately $1.5B and $400M, respectively, in trailing twelve-month revenue, together representing about 8% of total company revenue. Although they remain limited compared to its core solid waste operations, their importance could be one to follow in the years to come.

Waste Management now operates 105 materials recovery facilities. These operations focus on processing mixed recyclables collected from residential curbside programs and commercial customers, sorting paper, cardboard, plastics, metals, and glass. Many of its newer MRFs rely heavily on automation implemented in recent years, including optical sorters, sensor-based systems, artificial intelligence-driven identification, and mechanical separation, to improve sorting accuracy, throughput, and labor efficiency. Once processed, materials are baled and sold into end markets as commodities.

Revenue in the segment comes from two sources: processing fees charged to municipalities and waste generators, and the sale of recovered materials. While processing fees provide a stable base, overall profitability can fluctuate significantly with commodity prices, making recycling structurally more volatile than collection or disposal.

Strategically, recycling plays an outsized role despite its smaller contribution to earnings. Many municipal contracts and franchise agreements mandate recycling as part of integrated waste services, and commercial customers increasingly evaluate providers on their ability to support diversion targets and sustainability goals. As has been the case for decades, providing recycling alongside its other services makes WM's entire offering more attractive overall.

As organic waste decomposes in landfills, it produces methane-rich biogas. Federal and state regulations have long required this gas to be captured and managed, but what was once flared off purely for compliance has become a valuable energy resource. Across 102 owned or operated landfills, Waste Management has built and operates gas collection and conversion infrastructure that captures methane and transforms it into usable energy, such as electricity, pipeline-quality renewable natural gas, and direct-use fuel for industrial customers.

That energy is sold to utilities and industrial users, injected into natural gas pipelines, or used internally to power WM's own operations, including fueling its growing fleet of natural-gas trucks. Importantly, these systems continue operating long after a landfill closes, as gas generation persists for decades even without new waste being added.

The economics of landfill gas and RNG projects have improved materially in recent years, supported by the passage of the Inflation Reduction Act in 2022. Among other provisions, the legislation allows WM to qualify for federal investment tax credits, providing upfront capital support as new facilities are constructed. WM recognized approximately $145M of these credits across 2023 and 2024, and based on its current buildout plan, expects to receive roughly $220M in 2025 as it advances its RNG development pipeline.

Once operational, these facilities generate recurring revenue through what the industry refers to as a “credit stack”: a combination of environmental attributes such as Renewable Identification Numbers (RINs), Renewable Energy Certificates (RECs), and other incentives layered on top of the actual gas sales. Together, these factors have improved project returns and accelerated WM's pace of investment in RNG.

Importantly, management frames the opportunity as extending well beyond near-term tax credits. WM expects its sustainability investments (renewable energy and recycling) to generate approximately $800M in annual EBITDA by 2027, representing a significant increase from the $353M these segments generated in 2024. Much of the strategic appeal also lies in the disproportionate free cash flow conversion these businesses are expected to deliver relative to the rest of the portfolio. CEO James Fish provided context on this at the Raymond James & Associates' 46th Annual Institutional Investors Conference 2025:

“... one quick thing to add, and that is that -- just to put it in perspective, Devina talked about $800 million in EBITDA by 2027. That will be, likely -- we haven't given 2027 guidance yet, but it will likely be less than 10% of the total entity EBITDA. And here's the amazing part about that. And we -- Devina kind of laugh about this number a lot.

But if you think about what that converts to in terms of free cash flow, that $800 million, that's going to be less than 10% of the overall entity will probably convert to somewhere between 60% and 75% of free cash flow. So well above the kind of the 50% that we target for the rest of the business. So call it kind of $500 million to $600 million in free cash flow. In 2012, the entire corporation generated $829 million in free cash flow for the year. And now we're talking about something that's at least approaching that for less than 10% of the business. It's part of why we feel as good as we do about these investments we've made, this $3 billion that we're putting down in sustainability.”

The operating structure outlined above, shaped by regulation, landfill scarcity, and vertical integration, creates Waste Management's financial profile. Stable demand, long-term contracts, and control over disposal assets translate into predictable revenue and durable pricing power.

For the twelve months ended September 30, 2025, these operations generated $24.8B in revenue. After past scandals and structural missteps, the company's inherently stable model began to compound more visibly as operational discipline took hold heading into the 2010s. Rewind a decade from today, and revenue stood at $13B, implying a 6.7% CAGR achieved steadily through the pandemic, inflation, geopolitical disruption, and everything in between.

This topline expansion comes from two sources: low single-digit volume expansion and disciplined pricing. The company embeds automatic price escalators in many contracts tied to CPI or specific cost indices for fuel, labor, and disposal. But the more important driver is pricing power rooted in structural advantage. Disposal capacity is scarce, alternatives are limited in many markets, and switching providers becomes costly once customers are operationally integrated into a waste network.

WM leans into this position through what it calls yield management, increasing pricing based on the scarcity value of disposal and transfer capacity rather than simply passing through costs. In the third quarter of 2025, collection yield increased 4.2%, landfill yield 2.7%, and transfer station yield 5.6%. Historically, transfer pricing had been largely flat, but management has increasingly recognized that transfer capacity in constrained urban markets carries scarcity value similar to landfills themselves. As CEO, Jim Fish explained during the Q1 2023 earnings call:

"I'm not sure we've priced it that way over the years. You're seeing us price it that way. We recognize that these have a finite life to them."

Waste Management's integrated infrastructure leads to profitability growing faster than revenue. That operating leverage has driven EBITDA, which provides a clearer view for an asset-heavy business, from $3.4B in 2015 to $7.3B on a trailing twelve-month basis as of Q3 2025, representing a CAGR of 7.9%. EBITDA margins improved from 26.1% to 29.4% over this period.

Margin expansion has come from several sources. Cost efficiencies across operations, particularly through automation and technology investments that have reduced labor intensity across collection, have played an important role. Additionally, WM has become more selective about contract economics, exiting or repricing low-margin arrangements and prioritizing growth in commercial and industrial segments.

Another leading driver has been internalization: the ability to capture margin at multiple points along the value chain. As mentioned earlier, WM's internalization rate has increased from roughly 66% in the mid-2010s to over 71% by 2025. Continued investment in transfer infrastructure alongside selective M&A has been central to that progress, allowing more collected waste to be routed through WM's own network rather than third-party facilities.

The $7.2B Stericycle acquisition in 2024 added a parallel business with similar structural characteristics to WM's core operations. This represented a broader extension of its traditional tuck-in acquisitions, which we'll cover in more detail soon. Stericycle, now known as WM Healthcare Solutions, specializes in regulated medical waste collection and disposal for healthcare facilities, operating across North America but also in the U.K., Ireland, and several continental European countries.

Healthcare waste operates under comparable dynamics as the core business: non-cyclical demand, high regulatory barriers, and opportunities to cross-sell services to existing customers. Then-CFO Devina Rankin focused on that latter opportunity at its Q3 2025 earnings call:

“But the health care sector was one of those where we were underrepresented relative to our share in other important segments of our customer base. And we've seen great success in leveraging, I would say, the WMHS customer base in order to extend traditional solid waste performance across that national accounts platform.

And then we've also seen success the other way, where we've taken Legacy WM customers and thought about shred opportunities or even using the Healthcare Solutions platform in order to deepen the customer relationship. I think what's really important there is that when you become that single source provider for a customer, that customer relationship will be longer and provide incremental value.”

After closing its first full year of operations under WM, the new segment contributed $3.2B in revenue over the trailing twelve months ended Q3 2025, roughly 14% of company revenue. While the segment had an immediate meaningful impact on total revenue, profitability remains limited with integration ongoing.

Sustaining WM's asset-heavy operating model requires meaningful ongoing reinvestment. For the twelve months ended September 30, 2025, that translated into $2.4B of CapEx, primarily to maintain its fleet, landfills, and processing infrastructure. Despite the need for continuous reinvestments, the company generated approximately $2.6B in free cash flow, implying a 52% conversion rate, consistent with historical levels.

Looking ahead, it will be interesting to follow whether WM's sustainability segments can have the outsized impact on its financials that the company has guided for. If they do convert “somewhere between 60% and 75% of free cash flow” and deliver approximately “$500 million to $600 million in free cash flow,” the answer is likely yes.

)

As consistent as its services is Waste Management's approach to capital allocation. The company follows a clear hierarchy that prioritizes stability, reinvestment, and disciplined growth – a framework Devina Rankin outlined at its 2025 Investor Day:

“It is equally important to WM that we provide a long-term sustainable increase in the dividend. It's also important for us that we grow organically and reinvest in the future. … Then beyond that, once we've taken care of the dividend and we've taken care of that strong organic reinvestment, we focus on M&A. … Share repurchases is really [...] where the money goes once we've done everything else.”

First, WM has paid dividends continuously since 1998. As of 2025, the company has increased its payout for 22 consecutive years, earning Dividend Aristocrat status. Alongside dividends, capital is directed toward reinforcing the network itself. That includes organic investments aimed at optimizing airspace utilization, increasing internalization, and positioning it ahead of potential disposal capacity constraints over the long term.

Mergers and acquisitions represent the next layer of capital deployment. WM primarily focuses on tuck-in transactions that densify collection routes or expand disposal capacity within existing markets. In practice, this has meant a steady stream of small- to mid-sized acquisitions of local haulers whose operations complement its own. By acquiring collection routes in markets where it already operates transfer stations and landfills, WM internalizes volumes, converts external disposal fees into internal margin, and captures immediate route-density synergies without requiring incremental infrastructure buildout.

Taking care of garbage may sound like a simple business. But as you know by this point, that's far from the truth. For Waste Management, it means owning and operating an immense physical network of 257 landfills, 339 transfer stations, more than 15,500 trucks, and an expanding set of recycling facilities, gas conversion assets, and hazardous-waste operations serving industrial and healthcare customers. Running that system efficiently under dense regulation at every step is what turns waste management from a basic service into a deeply complex but remarkably durable business. WM has, not without a few bumps along the way, learned to master the entire value chain and extract value at every step.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)