Oracle is back at the center of the tech conversation. For nearly fifty years, it evolved from a fast-moving innovator into the dependable backbone of enterprise software, powering everything from government databases to healthcare systems. Then came September 2025, and over the course of an earnings call, the narrative changed. This is the story of Larry Ellison's Oracle, its decades-long transformation, and how it built a cloud tailor-made for the age of AI.

Key insights

Innovation and growth: An early bet on SQL and portability fueled Oracle's growth in the 1980s and made its database the standard for enterprise data systems worldwide.

Vertical expansion: Through the years, Oracle transitioned from its database core to an enterprise suite of applications, eventually offering the full stack after decades of acquisitions.

Cloud strategy: Oracle has differentiated its cloud infrastructure with standardized architecture, flexible public and dedicated deployments, and embedded database services in partner clouds.

AI positioning: Its Q1 2026 earnings announcement came with massive multi-year AI commitments, shifting the focus and narrative from enterprise backbone to AI partner.

Larry Ellison: Co-founder, longtime CEO, and now CTO and Chairman – Ellison is synonymous with Oracle's success and its transformation into the company it is today.

Cloudy skies ahead

We begin this story on September 9, 2025, and Oracle has just reported its Q1 2026 results. A company long seen as the infrastructure layer of enterprise IT suddenly was in the AI spotlight. After-hours trading hinted at what was coming.

As the market closed on September 10, Oracle had jumped 35%, adding roughly $200B in market value, in one of the biggest single-day moves on record. The reason? A tidal wave of demand from the most sought-after customers of our time: the builders of large language models (LLMs).

Since the introduction of ChatGPT from OpenAI in late 2022, LLMs have sent disruptive waves across digital workflows worldwide. The transformation has rewritten processes, displaced workflows, and in some cases replaced workers altogether, all while stock markets have reacted with an enthusiasm reminiscent of the dot-com boom.

Relentless prompting from billions of connected devices has prompted an unprecedented build-out of compute infrastructure. The result is a value chain with names such as NVIDIA, AMD, Broadcom, and TSMC driving the semiconductor side and Microsoft, Alphabet, and Amazon racing to expand cloud and AI capacity. And now, Oracle has earned itself a place as a core part of that chain.

The company's Q1 2026 order book stunned everyone. Commitments totaling hundreds of billions of dollars, locked in through long-term cloud contracts with some of the world's most ambitious AI developers. The kind of numbers that instantly repositioned Oracle in the eyes of investors and competitors.

“Eventually, AI will change everything. But right now, AI is fundamentally transforming Oracle and the rest of the computer industry, though not everyone fully grasps the extent of the tsunami that is approaching.”

To understand how Oracle got here, we need to retrace the steps that led to today.

Larry Ellison and the founding of Oracle

While Oracle had three co-founders, the company's identity is inseparable from only one of these: Larry Ellison. Born in New York and raised in Chicago, Ellison worked as a programmer in California after brief stints at two universities.

In the mid-1970s, he joined Ampex, a data-storage company focused on large memory systems. It was here that he first crossed paths with Oracle's other co-founders, Bob Miner and Ed Oates. In 1977, the trio struck out on their own, forming Software Development Laboratories (SDL), initially acting as a consulting agency.

Soon after, they came across an IBM research paper by Edgar F. Codd describing the relational database model, a new system that allowed businesses to store and retrieve data far more efficiently than before. Building on Codd's theory, IBM researchers designed a new programming language for querying such databases, called SQL (Structured Query Language). IBM was still experimenting with the concept internally, so no commercial product existed yet. If SDL could build something on SQL and ship it earlier, while making it compatible with IBM systems, they might just be able to seize a head start.

At the time, large enterprises typically ran enormous computer systems that were costly to operate and required teams of specialists to manage. The database SDL built broke with those constraints: sold as software – first on magnetic tape and later on floppy disks for on-premises install – it could run on existing minicomputers, organize data into tables, and allow information to be searched, updated, and linked in ways older systems simply couldn't. In hindsight, the path seems straightforward. At the time, commercial viability was far from assured.

When you innovate, you've got to be prepared for everyone telling you you're nuts.— Larry Ellison

The first major customer to test out their system was the CIA, which wanted a relational database to manage classified information, under the project name “Oracle.” The project was a success, proving that its relational database could handle sensitive, large-scale workloads and gave it instant credibility.

By 1979, with Ellison as the clear-cut CEO, the company rebranded as Relational Software Inc. and was selling what it called the world's first commercial relational database: Oracle. In a few years, the project that had named the product, also named the company itself. Similar to the CIA, many of its early customers were government contracts, including the U.S Air Force and the FDA. Delivering to the standards of these institutions and their critical workloads, built recognition and momentum through the early 1980s.

In 1983, Oracle released Version 3, a portable database across platforms. Unlike rivals tied to specific systems, this update enabled Oracle to run on all the usual hardware and operating systems, whether it was a mainframe, minicomputer, or a PC, further driving adoption of its database. The combination of portability and Oracle's early bet on SQL meant that when the language became the industry standard in the mid-1980s, the company was perfectly positioned to take market share.

Oracle's co-founders and first hire, from left to right: Ed Oates, Bruce Scott, Bob Miner, and Larry Ellison.

Momentum and expansion

By the mid-1980s, Oracle was growing dramatically, adding corporate clients alongside government ones, and expanding abroad through distributors. Through these years, the company became known for its aggressive sales culture. Its commission-based sales organizations' ambition to finalize deals quickly often meant promising features still in development or even pre-development. Although the approach drew criticism (and later caused problems), it helped fuel its hypergrowth.

While Oracle's software was being adopted by clients in banking, telecom, and pharmaceuticals, the company increased revenue at an explosive pace. From roughly $5 million in FY1983, it ended FY1986 with $55 million in revenue, just as it completed an IPO on the Nasdaq exchange. By the close of its first full year as a listed company, in FY1987, Oracle had doubled its revenue in nine of its first ten years.

That same year, Oracle ramped up international expansion, selling its database to more than 4,500 end users in 55 countries, consistently rolling out product updates that supported larger, more complex workloads across varied environments. Around this time, IBM, whose research inspired Oracle's direction, had rolled out its DB2 database and was competing head-to-head as a robust option.

This was an early sign of a dynamic that would become recurring in the decades to come: competing with powerful incumbents with deeper positions and foundations than Oracle's. The company's culture thrived with that challenge. Bold, aggressive, and driven by Ellison's constant push to keep the company in the conversation with the industry's biggest names.

By decade's end, revenue had grown nearly 10x from its IPO just a few years earlier, ending FY1989 with well over $500 million and with $82 million in profit. It seemed like nothing could stop Oracle, and with the decade of the internet beginning, it looked positioned to build on its success. But cracks were starting to show beneath the surface.

“One day I get a call from one of our largest customers, located in the northeastern United States. He tells me, 'Larry, we've decided to buy all of our Oracle software from Oracle Brazil.' I said, 'But you're headquartered in Connecticut, Connecticut's not part of Brazil. Why are you doing that?' He said, 'They gave us the best price.' Shit. Everything is so duplicative and decentralized, the right hand doesn't know what the left hand is doing. We're competing against ourselves. This is embarrassing.”

– Softwar: An Intimate Portrait of Larry Ellison and Oracle, Matthew Symonds & Larry Ellison (2004).

Paying the price

Oracle's 1980s surge hit a wall in 1990. The company's reckless sales culture was well known, and now it appeared that this had led to improper revenue recognition and misstated results. Deals were often booked before software was delivered or fully paid for, and some amounts never even materialized as revenue. In August, Oracle restated its financials for three of the previous four quarters, acknowledging that reported growth had been overstated.

Troubles deepened in September. Oracle lowered its growth guidance, announced a 10% workforce reduction, and felt pressured to arrange a line of credit to steady the business. The shake-up extended to the top, with Oracle replacing its CFO to restore discipline and put the company on a more stable path going forward.

The stock market was honest and brutal in its judgment of the events. In just a few months, Oracle's stock lost around 80% of its value. The turbulence – with restatements, slowing growth, and its first annual loss – carried into the following year, but Oracle endured. With no debt weighing down its balance sheet and sales slowly beginning to recover, it could finally put the crisis behind it.

You pay a price for growing too rapidly.— Larry Ellison

The enterprise expansion era

As the early-1990s challenges played out in public, Oracle was slowly beginning to widen its product focus. Having started an applications division some years earlier and recently launched a packaged accounting software program, it was now preparing to expand vertically, adding new business modules on top of its already successful database offering.

Over these years, Oracle rolled out applications for human resources, manufacturing, and supply chain management, gradually assembling what would eventually become a full enterprise applications suite. Much like SAP, the German software company that had already established itself in the 1980s as a leader in integrated enterprise applications, Oracle's strategy was to build business software tightly integrated with its own technology stack.

Through it all, Oracle's database division remained its foundation, competing fiercely with IBM, Sybase (acquired by SAP in 2010), and increasingly Microsoft. With that last-mentioned competitor in mind, Ellison and Oracle also began pivoting some attention to a new frontier in computing that was taking shape.

In 1996, he unveiled the “Network Computer,” a roughly $500, stripped-down machine pitched to undercut Window's position. Backed by partners like Sun Microsystems and Netscape, it promised cheaper corporate computing by shifting data and applications to servers running Oracle software (later referred to by Ellison as inventing the cloud). The concept drew headlines but never reached full commercial stage as PCs quickly proved to become more affordable and powerful. By 1998, Ellison admitted Oracle had overestimated the potential of the NC, accepting that the PC had won.

Although it never cracked the Microsoft/Intel monopoly in hardware, Oracle thrived in the internet era of software. It recast its database and applications for web workloads and expanded into building online B2B marketplaces, using its stack to power sourcing, auctions, and order management for large corporations.

If the internet turns out not to be the future of computing, we're toast. But if it is, we're golden.— Larry Ellison

Coupled with roughly 20% annual revenue growth in the run-up to the new millennium, its internet ambitions sent Oracle's stock soaring, up nearly 600% in a single year at the dot-com peak. When the bubble burst, its shares collapsed along with everyone else, but Oracle entered the 2000s with a broader footprint and a central role in enterprise IT.

Ellison at the turn of the millennium, leading Oracle into the internet age.

Acquiring applications

By the early 2000s, although Oracle's database division remained its foundation, it was steadily layering applications on top of its database strength, aiming to be an end-to-end enterprise platform. After a largely organic build-out in the 1990s, the next phase was defined almost entirely by acquisitions.

From the mid-2000s onward, Oracle went on a dealmaking spree that reshaped the company. From large acquisitions of PeopleSoft and Siebel, adding human resources and customer relationship management, Oracle went out and acquired over 50 companies in a period of less than five years. With all of these, its application suite was being transformed and broadened to cover every enterprise vertical.

This acquisition strategy has continued all the way into recent years. In 2016, Oracle bought cloud-native ERP pioneer NetSuite (which Ellison had funded early on and remained the majority investor of), and in 2022, it made its largest deal ever with the $28B acquisition of Cerner, anchoring its position in healthcare IT.

Over time, these acquisitions shifted Oracle's profile from a company dominated by databases to one generating a larger share of its revenue from what was essentially a full software stack.

Becoming the Oracle of today

By the late 2000s, with Oracle competing across the full enterprise software stack, it was beginning to reshape its comprehensive offer, including the database, into the foundation of a cloud strategy.

As the concept of “the cloud” arrived in the latter half of the 2000s and early 2010s, a common misconception was that Larry Ellison was somehow “anti-cloud”. Although his skepticism was unmistakable, it was aimed at the buzzword, not the concept.

“The interesting thing about cloud computing is that we've redefined cloud computing to include everything that we already do. I can't think of anything that isn't cloud computing with all of these announcements. The computer industry is the only industry that is more fashion-driven than women's fashion. Maybe I'm an idiot, but I have no idea what anyone is talking about. What is it? It's complete gibberish. It's insane. When is this idiocy going to stop?”

– Larry Ellison, Wall Street Journal (2008).

If you ask Ellison himself, he was pursuing cloud-like technology long before the term was popularized. His effort with the Network Computer in the 1990s, which was cloud-like in theory, and his contributions to NetSuite, widely held as one of the earliest SaaS companies.

However, when the term cloud computing started gaining traction, it was not Ellison and Oracle that the conversation centered around. Instead, it was the big cloud players we now know as Amazon's AWS, Microsoft's Azure, and Alphabet's Google Cloud.

After a few years, Oracle finally launched its own cloud services. In June of 2012, Ellison revealed that the company had spent years rewriting many of its applications to run in the cloud, and was now launching Oracle Cloud with databases, Java, CRM, ERP, and marketing tools all available as a service.

Alongside the shift, Oracle continued with the aforementioned acquisition spree, adding stacks, both vertically for the enterprise suite, and horizontally strengthening its database and cloud businesses. Over this period, the database core kept advancing, increasing the number of customers that could run safely on the same system and introducing greater automation for management and security. Given how many core systems ran on Oracle's database and how it constantly kept improving, customers largely stayed with the foundation they relied on and trusted.

A different cloud strategy

Oracle's initial cloud strategy centered on its applications, rebuilding what customers already used and positioning the SaaS versions as the natural upgrade. Its Infrastructure service (OCI) arrived formally in 2016. By that time, the likes of AWS, Azure, and Google Cloud had already established hyperscale footprints and defensible moats that Oracle wouldn't breach for nearly a decade. Instead, its early share was mainly concentrated in existing Oracle applications or database workloads.

But throughout the years, it increasingly found ways to differentiate. Many of its customers, including banks and insurers that run mission-critical systems on Oracle databases, wanted those workloads in the cloud but couldn't afford to rebuild from scratch.

Oracle responded with a flexible approach to deployment. Instead of a one-size-fits-all public cloud, it offered the same stack wherever customers needed it: full regions delivered on-premises for regulated or latency-sensitive work, or smaller managed footprints behind the firewall. Additionally, it even began embedding database services inside partner hyperscalers' clouds, enabling customers to run Oracle databases directly within AWS, Azure, or Google Cloud.

By the early 2020s, OCI had become a standardized cloud platform. In summary, the design leaned into GPU-heavy infrastructure, mainly built around NVIDIA hardware on bare-metal servers with fast, tightly linked clusters. Just as important, the design became increasingly uniform, allowing Oracle to roll out new regions quickly.

During these years, TikTok's U.S. deployment on its cloud offered an early (but still as relevant), public proof that Oracle could handle compliance-heavy, high-stakes operations. Its propositions' strengths were built around this differentiated approach focused on performance per dollar, fast deployment, and a stack that behaved the same wherever it landed.

In parallel, Oracle pulled the database into AI use cases, adding native vector search/embeddings and allowing data to be close to compute so enterprises didn't have to overhaul core systems to adopt LLMs. Rather than chase breadth like the hyperscalers, Oracle targeted workloads with tight latency, data proximity, and compliance constraints. By 2025, its vertical integration, modular deployment options, and focus on compatibility had become clear advantages.

Oracle is already prospering in this new era of cloud computing and AI, and it's just the beginning.— Larry Ellison

On the other side of the transformation

Zooming out, from Oracle's 1980s hypergrowth and the last decade, the company evolved from innovator to applications provider. Acquisitions and a broader enterprise stack made Oracle a global leader, but many came to view it as a legacy IT vendor. Markets reflected that perception: after the dot-com peak, the stock didn't set durable new highs until 2017.

As the organization expanded and evolved, the management structure also changed. Larry Ellison stepped down as CEO in 2014 and became Executive Chairman and CTO, while Safra Catz and Mark Hurd ran operations as co-CEOs until 2019, when Catz became sole CEO.

In September 2025, Catz stepped down, and Oracle named two insiders, Clay Magouyrk (previously OCI) and Mike Sicilia (previously applications/industries), as co-CEOs, with Catz moving to Executive Vice Chairman. Through it all, Ellison's influence on the company's direction remained constant.

A visualization of Oracle's transformation over the decades.

Breaking down Oracle

Oracle of 2025 is still mainly that enterprise software provider, but as you know, quickly shifting the share of its business. Breaking down its FY2025 $57.4B in revenue, the main contributors are cloud applications, cloud infrastructure, and the traditional software base of licenses and support. The remaining part is comprised of hardware and service revenue associated with its segments.

The distinction between these isn't so much about different products as it is about deployment models. Many of the same systems are offered as Oracle-hosted cloud subscriptions or as licensed software that customers run on-premises. Most apps support both models; some are cloud-only, and certain legacy products remain on-premises only.

The core database

Before turning to applications and cloud in detail, it's worth tying back to Oracle's core database. Even as other segments have grown and taken the spotlight, the database has remained the organizing center of the model, strengthening each layer that has been added on top of or in connection to it. It shapes OCI's performance profile, binds and builds the foundations of its applications, and is now powering AI workloads that need data close to compute.

“We are the key enabler for enterprises to use their own data and AI models. No one else is doing that. [...] This is why our database business is going to grow dramatically. Think about it. You have to put all of your data into a database. So that database must be highly secure. It must be scalable. It must be economical. It must be reliable, 7 days a week, 24 hours a day. It has to be fault-tolerant. It can never break.

That's how Oracle got popular in the first place. But then it has to hold the data in a way that's consumable by the AI models. In other words, the data has to be vectorized and searchable by the AI models and you use that data to train up those models on your data? Who else is doing that. Let me answer the question, nobody.”

The resilience of Oracle's database was highlighted at its September 2024 Financial Analyst Meeting, where it reported a 102% net dollar retention rate in its database support business over the prior four years, and that it was in continued use at 94% of Fortune 100 companies. As emphasized in the above quote and figures, although reshaped over decades, Oracle's core remains as relevant as ever.

The power of the full suite

Oracle's enterprise applications now cover the full corporate backbone with ERP, HCM, SCM, CRM, and more, all under one roof. Its wide set of applications handles over a billion calls and text messages every day, supporting its over five million subscribers. The breadth is wide, but what defines it is just that: most offerings are modular and designed to integrate, so customers can adopt individual pieces while knowing they will fit into a larger, unified system. That flexibility makes expansion within a customer more natural, reinforcing both lock-in and cross-sell.

The model is anchored in a vertically integrated stack that ties hardware, databases, and applications across multiple deployment models. That makes it particularly attractive for mission-critical workloads in industries where reliability and compliance are non-negotiable, like banking, healthcare, and government.

Its most important applications is the Oracle Fusion Cloud portfolio, which provides cloud solutions for ERP, HCM, supply chain, and customer-facing functions and NetSuite, a cloud-native suite for mid-market companies, covering financials, ERP, CRM, and e-commerce. Oracle Fusion Cloud ERP and NetSuite Cloud ERP, specifically and respectively, both account for roughly 25% of cloud application revenue (~7% of total revenue), making them the largest drivers in this segment.

Other offerings, such as Oracle Health, strengthened by its large acquisition of Cerner in 2022, Oracle Advertising, and other mainstay applications of PeopleSoft, JD Edwards, and Siebel, extend the suite further into specialized industries.

What unites all of these solutions is their stickiness and how that increases over time. The more mission-critical the workload, the harder it is to replace; adding adjacent modules increases switching costs and broadens the footprint. The same dynamic runs through Oracle's database, applications, and cloud infrastructure, with every additional layer added making it more indispensable for customers.

The growing Oracle cloud

Much has changed at Oracle since Ellison first announced that its applications had been rewritten for the cloud. The numbers tell the story: in FY2015, cloud made up just 9% of Oracle's revenue; by FY2020, that share had climbed to 26%. Today, although cloud applications and infrastructure on their own amount to a little less than half of revenue, including licenses and support of those segments brings it to over 75% of total revenue, and it's still growing faster than ever.

The majority of this half comes from applications. For new customers, deploying in the cloud has increasingly become the default choice, and for existing customers, workloads that once ran on-premises are slowly but steadily migrating.

But the real acceleration is happening in infrastructure with Oracle Cloud Infrastructure (OCI), its IaaS offering, increasing most recently by 55% year-on-year in its Q1 FY2026. With the events of early September, it's more than likely a matter of quarters before it becomes the biggest revenue generator in the company.

From its launch in 2016, OCI has evolved from a late entrant to a differentiated platform rooted in Oracle's database heritage and flexible deployment model. It doesn't match AWS, Azure, or Google Cloud on sheer scale, but its standardized architecture is resonating with a widening set of enterprises and workloads.

“Oracle's future is bright in this new era of cloud computing. Oracle will be the #1 cloud database company. Oracle will be the #1 cloud applications company, and Oracle will be the #1 builder and operator of cloud infrastructure data centers.”

After a relatively flat stretch through much of the 2010s, Oracle's revenue has increased over the last few years, driven by the Cerner acquisition (adding about $5.9B to the topline in its first full year, FY2023) and accelerating cloud momentum. For FY2025, Oracle reported total revenue of $57.4B.

That topline number is projected to climb sharply in the years to follow, driven by the demand for OCI's services. At its 2025 Financial Analyst Meeting, Oracle announced a revenue target of $225B by FY2030, implying a CAGR of 31% over those five years.

Similar to revenue, profitability has remained flat, but anchored at high levels thanks to its strong software position. In the most recent years, EBIT was brought down in FY2022 by a one-time litigation fee to HP and in FY2023 by the Cerner acquisition, but has been on the rise since. Its FY2025 EBIT of $17.7B takes its margin to 30.8%.

As said, of its FY2025 revenue, over 75% came from subscriptions, which include both cloud services (SaaS and IaaS) and ongoing support for all its licensed software. The remaining ~25% comes from services, including consulting and advanced customer support; cloud and on-premise licenses (new license sales recognized up front), and finally, hardware.

Due to Oracle's previous segment distinction, there is limited thorough insight into the long-term performance of its SaaS and IaaS offerings. However, in FY2025, its SaaS offerings totaled $14.3B (~25% of total revenue), increasing by 10% year-over-year. During the same period, IaaS (OCI) grew by 50% to $10.2B, now accounting for a little less than 20% of the total.

Going forward, for both of these segments, the migration from on-premise support to the cloud is a key opportunity. What makes the shift powerful is the step-up in revenue Oracle realizes on migration. Applications support converts to cloud at a 4x ARR multiple, while infrastructure support converts at a 5x ARR multiple. In 2024, management estimated that this uplift represented an $85B incremental opportunity just from upgrading existing customers.

Those multiples can look steep from a customer perspective. But cloud isn't a like-for-like swap: Oracle is absorbing all those costs in hosting, operations, and upgrades that customers would otherwise manage themselves. At its September 2024 Financial Analyst Meeting, Oracle noted that 89% of application workloads and 95% of infrastructure workloads remain on-premise. In other words, the migration has barely begun, leaving a vast revenue opportunity still ahead.

Shifting opportunities

From the acquisition-heavy 2000s to where Oracle is today, the capital allocation cycle has transitioned to aggressive share repurchasing and on to its recent buildout-focused CapEx. While acquisitions to its enterprise suite have continued throughout, the emphasis has moved toward organic growth.

Since 2009, Oracle has paid quarterly dividends that have steadily increased over the years. Over the last decade or so, the company has also been consistent in its buybacks. After maintaining steady levels in the early 2010s, Oracle significantly ramped up the pace in FY2013.

This continued for several years at notably high levels, eventually peaking in FY2019, when the company bought back nearly 15% of total shares outstanding in just that year. Around that time, then CEO Safra Catz was asked about the pace of buybacks versus other uses of cash:

“We think our stock is an unbelievable buy, so we are buying it back. And I'm not going to tell you exactly how much, but you can see I've got $20 billion in authorization, which I'll use up when I use it. But at these prices with our growing cash flows, with our earnings growing like they are, it seems like an amazing deal to buy our stocks, so we're putting our money where our mouth is, frankly.”

After continuing to run at high levels for a couple of years – and capitalizing on the low-interest-rate environment during the pandemic to issue debt that further supported buybacks – the company has reduced its repurchases in recent years. Instead, the focus of that excess cash has shifted to supporting the opportunities of OCI:

“So where do we expect OCI to go from here? Frankly, the only limiting factor is our ability to get the data centers, hand it over and filled up fast enough. This quarter alone, we're talking about hundreds of millions of dollars that we would have been able to recognize if our capacity was available. [...] And as you can see in my CapEx guidance, we expect OCI to just grow astronomically, frankly.”

At its Q1 FY2026 earnings call, Safra Catz summed up the impact of a decade of aggressive repurchases: “Over the last 10 years, we've reduced the shares outstanding by 1/3 at an average price of $55, which is, at this point, much less than 1/4 of our current stock price.” The “unbelievable buy” has clearly aged very well.

Although all shareholders have benefited, the largest beneficiary is Larry Ellison, whose ownership has increased as the float contracted, rising from around 26% to 40% during this decade – cementing his place among the world's wealthiest.

Oracle's EPS growth and the reduction of shares outstanding from FY1995.

Building to deliver

The earlier discussed migration of workloads to the cloud shifts costs from customers to the provider. To deliver, Oracle has spent the past decade building out its cloud. This is primarily for its infrastructure offer, where it now has a global footprint of self-contained cloud “regions” that run the full OCI stack. These range from ~6-rack starters to embedded multicloud regions inside hyperscaler facilities.

The main differentiator compared to competitors is the deployment method. Oracle phases capacity against booked demand, leases facilities through building partners, and concentrates CapEx in GPUs and CPUs from NVIDIA and AMD, storage, and high-performance networking. This shows up in the numbers with lease commitments more than doubling in Q1 FY2026 from the prior quarter to $99.8B. This approach is generally more capital-efficient and faster to roll out: equipment is installed when needed, and upon customer acceptance (which can occur within weeks), it begins generating revenue.

“One is we just turned over a giant data hall to one of our customers. And the acceptance time could have been as long as a couple of months. It was 1 week. It was 1 week from the time we owned -- officially owned the equipment, and they were testing it to the time they started paying for it, 1 week. So we have an extraordinary team that's doing an extraordinary job of making sure that we get the equipment working very quickly and our customers can accept it.”

As of early 2025, Oracle's regions crossed the 100-mark (with 98 live as of Q1 FY2026), and guidance has followed with the IaaS demand having surged. Its modular, standardized “Gen 2” architecture is what makes this ramp possible. Uniform setup and repeatable procedures that let Oracle start small, replicate quickly, and expand footprints as utilization rises. High automation and favorable vendor terms further compress the time-to-capacity.

“The other thing is our cloud was designed not for hundreds of regions but for thousands or possibly even tens of thousands of data centers and regions.”

To support the long-term vision and the gradually increasing demand in the past, the ramp-up in CapEx has been considerable (and will not slow down anytime soon). The visual below shows the "astronomical" trajectory Catz referenced.

After staying flat during the 2010s, CapEx has increased dramatically the last few years.

AI's demand for compute, storage, and power hasn't gone unnoticed by anyone. Oracle's announcement of multi-year AI contracts was not only an ambitious RPO (Remaining Performance Obligations) of $455B but also marked its entry into an elevated CapEx cycle. We'll unpack the RPO in itself shortly, but for now, let's focus on what this means for CapEx.

“... CapEx is going to go up because the demand right now seems almost insatiable. I mean I don't know how to describe it. I've never seen anything remotely like this. I mean people are calling up and asking us, please, can you find us more capacity. We'll take it wherever. It's in Malaysia, we'll take it fine. We'll take it there. We got some wherever.”

To saturate this unprecedented wave of cloud infrastructure demand, CapEx will follow in the same direction. For FY2026, CapEx is expected to increase to approximately $35B, which would be 60% higher than the year before and more than three times higher than FY2024. Previously, its operating cash flow generation has covered its CapEx, but going forward, that will likely not hold.

Ellison briefly touched on this in the Q1 FY2026 earnings call, summarizing it confidently: “I think we're going to do very well on the finance side. We have advantages there as well.” To bridge any potential gap, management has discussed incremental debt, vendor financing for GPUs/networking, and partner-leased facilities. Importantly, as stressed, Oracle's deployment model is designed to keep the lag between spend and revenue short, so much of the CapEx ramp should be offset as new capacity comes online.

The demand is astronomical.— Larry Ellison

“A tsunami approaching”

On September 9, 2025, Oracle announced multi-year AI contracts with OpenAI, xAI, Meta, NVIDIA, AMD, Cohere, and others. The commitments were so large that OCI went from a roughly $10 billion business to a potentially $450-plus billion book to be delivered over several years. Ever since, and as new layers of this have been added, the question has been how it all will play out.

When ChatGPT burst onto the scene in late 2022, the immediate need was training compute: stacks of NVIDIA accelerators, stitched together with fast interconnect, housed at hyperscalers that already had the land, power, and operational muscle. Within months, a value chain began forming, supporting the model layer and creating an ecosystem around its capabilities.

A simplified overview of the AI value chain.

Through the years that followed, as other models emerged and that ecosystem grew, the scale of training exploded. Campuses measured in the hundreds of megawatts became a talking point, and “Stargate” turned into shorthand for giga-scale ambition. Although training remains the core, the worldwide adoption of LLMs is shifting the center of gravity toward inference (the day-to-day use of models), where latency, proximity to enterprise data, and compliance drive the architecture.

“Training AI models is a gigantic multitrillion-dollar market. It's hard to conceive of a technology market as large as that one. But if you look close, you can find one that's even larger. And it's the market for AI inferencing.”

So how does Oracle fit in here? Inferencing fits well into its value proposition, uniquely sitting as custodian of millions of databases, securely and reliably wired into popular LLMs. Oracle's independence is another part of the appeal, because unlike the hyperscalers that also build or back frontier models, Oracle isn't competing at the model layer. But the main factor was how the company's transformation over the last decade rewired it from a catch-up cloud into a focused operator built for specific, high-stakes workloads.

As explained earlier, rather than chasing generalized hyperscale, it standardized on prebuilt, GPU-heavy capacity and prioritized performance per dollar, a short path from install to customer acceptance, and the ability to replicate the same stack across multiple environments. Paired with keeping models near the data enterprises already rely on, the result is a technology that labs suddenly turned to.

“I know some of our competitors, they like to own buildings. That's not really our specialty. Our specialty is the unique technology, the unique networking, the storage, just the whole way we put these systems together.”

Oracle's backlog of north of $450B is clearly not revenue in 2025, but remaining performance obligations, contracted value the company is obligated to deliver but hasn't yet earned. It converts only as capacity is built, energized, and up and running for the customer.

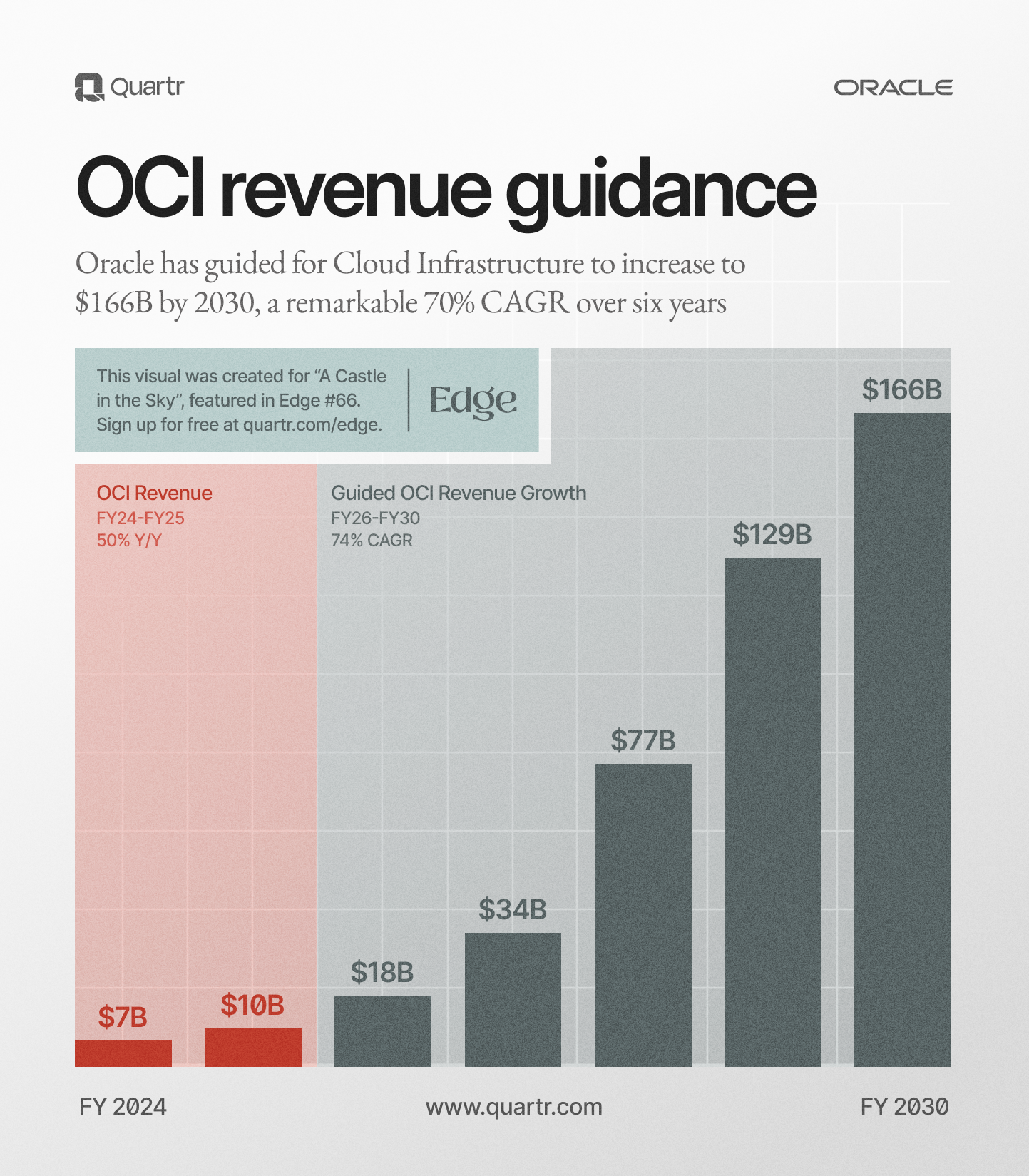

At the 2025 Financial Analyst Meeting, Oracle guided OCI to ramp from approximately $18B in FY2026 to $34B, $77B, $129B, and $166B over the following four years, with much of that already booked in the $455B RPO. Contracts blend subscriptions and metered usage, so revenue will follow service agreements and actual consumption of compute. Although years and assumptions between the conversion, the announced numbers have set expectations.

The demand is concentrated among a handful of frontier labs and platform players, with unprofitable OpenAI being the standout contributor. According to the Wall Street Journal, citing people familiar with the matter, OpenAI is said to account for a total of $300B of the volume. For all its scale, OpenAI and many of these labs are subject to shifting roadmaps, funding windows, and governance. Depending on who you ask, that could be a source of fragility.

That dynamic is, of course, most pronounced with the aforementioned company behind ChatGPT. Historically, it was funded by Microsoft and ran primarily on its Azure platform, but by mid-2024, it extended capacity onto OCI and has also added lanes with the other hyperscalers. Several of its partnerships through the value chain (most notably Microsoft, NVIDIA, and AMD) blend supplier capital, prepays, and equity-linked incentives, structures that speed access to compute but also tighter coupling between counterparties. As long as liquidity remains abundant and OpenAI's ambitious projections stay on track, Oracle can trust its partners' commitment to deliver on the $300B RPO.

Oracle's position helps here. With its broad global enterprise footprint and public-sector ties, it has room to redirect capacity toward enterprise inference and database-adjacent AI if a lab slows. That backstop isn't free or instantaneous, but it lowers the odds of truly stranded assets.

Let's move on to the supply side and whether Oracle can deliver to demand. Its CapEx is set to be deployed through a clear playbook: standardized regions dropped into leased shells, installed as late as possible because Oracle “puts in that equipment only when it's time and usually very quickly,” as Safra Catz put it. However, constraints can still apply.

Since ChatGPT's debut, NVIDIA has been the center of gravity in the AI buildout. The Jensen Huang puzzle piece is still as relevant today, and that goes for its role for Oracle as well. Although Oracle is adding a second lane with GPUs from AMD, the densest training and highest-throughput inference at most labs still utilizes NVIDIA's ecosystem.

NVIDIA's superior position in this AI buildout and the scarcity of its chips have been constant during these last years. While it has made it the largest company by market cap in the world, its dependency and desirability have bordered on theatrical. Recently, Larry Ellison recited how a dinner conversation between himself, Jensen Huang, and Elon Musk had unfolded:

“Please take our money, please take our money. [...] No, no, take more of it. You're not taking out enough that we need you to take more of our money, please.”

As for whether that dependence is a real risk: for now, it's mostly a timing risk, not an existential one. While AMD eases the reliance, it doesn't erase the constraint.

Converting the +$450B

Over time, the price customers pay for a unit of compute tends to decline as models, tooling, and orchestration mature, while delivery costs should fall even faster as infrastructure is optimized. As Microsoft CTO, Kevin Scott, noted at the Goldman Sachs Communacopia + Technology Conference in 2024 (sourced through Quartr Pro):

“... back in May [2024] [...] GPT-4 had gotten 12x cheaper like per token to do inference on than at launch time [in March 2023]. And so part of that is because the hardware had gotten a lot better. And part of it is because the infrastructure had been tuned within an inch of its life [...]

And I think this is just going to continue over time. So the important thing to realize is things are already getting on a price performance basis, like way cheaper than they were. And there's super good stuff coming from hardware to system software to algorithms that should keep that trend moving.”

The other side of the assumption of declining costs is utilization, conversion, and how efficiently that translates for Oracle as it scales. Along with the revenue guidance for OCI (visualized below) from its 2025 Financial Analyst Meeting, the company also touched on the margin profile for these large commitments. Management pointed to gross margins in the ~30–40% range for OCI's AI customers (ramp-up costs included).

Oracle's past revenue and guidance for OCI for the years ahead.

Still, over the length of the four-year RPOs, things can radically change: model designs shift, inference becomes cheaper, and the way chips are connected in data centers continues to improve. What looks state-of-the-art today can feel heavy a few quarters from now. The DeepSeek chapter was a reminder of how quickly narratives can turn and (briefly) reprice assumptions about where workloads should run.

Although Oracle's standardization and the ability to redirect can soften the immediate impact of adverse events, this highlights again another risk with its counterparties and the shape of these commitments.

Will it be worth it for Oracle? This is infrastructure economics: CapEx up front, paid back over years as the service delivers. The answer hinges on a few simple questions. Do the largest deals convert into healthy margins as clusters move from installation to full load? Does utilization keep the expected pace as training increasingly transitions to steadier inference? And does the hardware being installed today maintain performance through the depreciation cycle to keep unit costs falling faster than prices?

Together, these and more factors will determine margins and the cash flow that follows. Time will tell.

None of these uncertainties questions the demand. If Oracle delivers capacity on schedule and the magnitude of compute follows expectations, the booked ambition has a clear path to conversion at scale. Its engineering choices created the opening, and now consistent conversion defines the success. Execute, and Oracle can cement its place in AI infrastructure.

I've never seen an opportunity on this scale before.— Larry Ellison

Closing thoughts

The announcement of September 9, 2025, clearly changed the trajectory of Oracle. Where it leads remains to be seen. Oracle's story has many successful chapters with Ellison as the constant theme, driving the company forward. We'll end by paraphrasing the legend himself: If its AI ambitions disappoint, they're toast. But if everything lines up, they're golden.

)

)

)

)

)

)

)