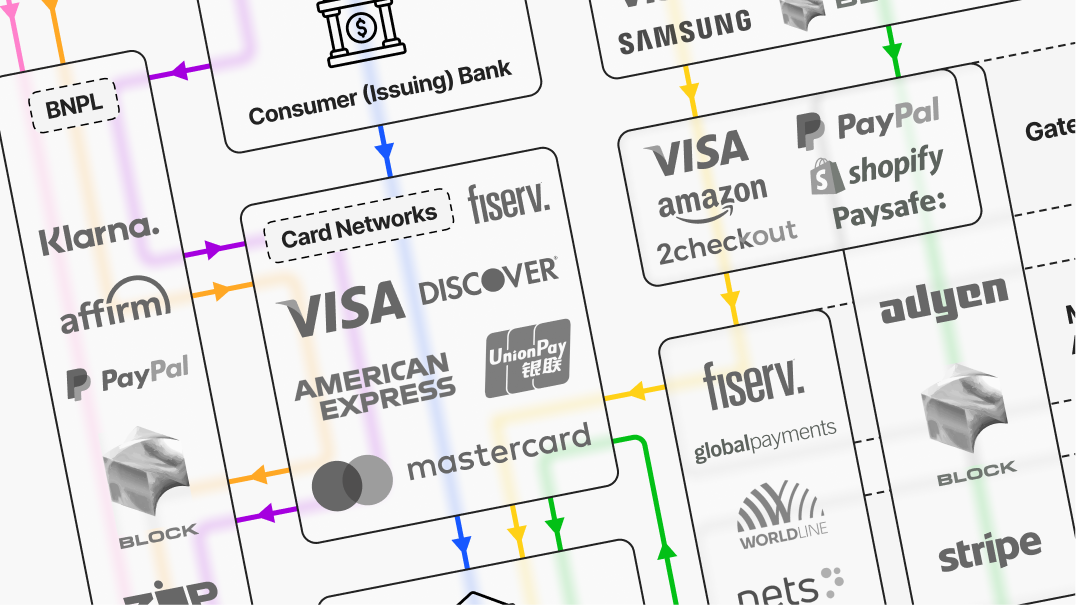

The payments industry is a complex and dynamic field involving multiple key players. These include customers, merchants, issuers, acquirers, card networks, and various other entities together forming the payments value chain. This article explores how these players interact and the roles of companies like Visa, Mastercard, Fiserv, Adyen, Amazon, and PayPal within this ecosystem.

The Five Key Participants in the Payment Value Chain

Merchants: These are businesses or individuals selling goods or services. To accept card payments, they must open a merchant account with an acquirer. This account is essential for processing payments and is used to register payables to the business. During a transaction, the merchant’s role is to initiate the payment process after the customer decides to make a purchase.

Acquirers: Also known as acquiring banks or financial institutions, acquirers provide merchants with the means to accept card payments. They play a crucial role in capturing transaction information and routing it through the appropriate card network to the cardholder’s issuing bank for approval. After payment collection, the acquirer settles the amount in the merchant account, which includes various fees and sales amounts.

Consumers: Often referred to as cardholders in the context of card payments, consumers are the end-users who initiate the payment process with the merchant. They benefit from the convenience of electronic payment methods for goods and services, both online and offline, and may participate in rewards and cashback programs.

Sign up for Edge

Get curated quality company deep dives every other week.

Issuers: Banks or financial institutions that issue credit and debit cards to consumers. They are responsible for providing customers with credit or debit accounts and making payments on their behalf. In the payment process, issuers manage payment authentication, approve or decline transactions, and ensure the transaction’s validity and the customer’s ability to pay.

Card Networks: These entities, often known as card brands, are involved in every card transaction, whether it’s a swipe, chip-and-pin, contactless, or card-not-present payment. Card networks like Visa, Mastercard, and others provide the infrastructure that makes card transactions possible. They are responsible for passing information and settling funds between the acquirer and the issuer and set standards and rules for transactions and disputes.

Other Integral Participants

Acquirer Processors: Acquirer processors provide the technical link between merchants, card networks, and acquirers. They handle payment processing from merchants through acquirers to card networks or alternative payment methods (APMs) like PayPal, ensuring transactions are authorized and settled. While distinct from acquirers, acquirer processors often work closely with them, handling technical aspects of transactions, including fraud and chargeback minimization, and creating payment databases.

Payment Service Providers (PSPs): PSPs, such as PayPal, connect merchants to the financial system, enabling them to accept various payment methods, including credit and debit cards. They manage the entire payment transaction from authorization to settlement and act on behalf of merchants. PSPs differ in their service offerings, with some providing basic services and others offering comprehensive support, including security, fraud protection, and regulatory compliance.

Payment Gateways: These collect payment credentials from the merchant’s clients and forward them securely to PSPs or acquirers. They also act as intermediaries in electronic financial transactions, supporting both in-person and online businesses. They handle encryption of payment data, connection with payment processors, transaction authorization, data collection, and fraud detection. Gateways ensure secure, efficient, and accurate processing of various payment methods, including credit and debit cards and digital wallets.

Independent Sales Organizations (ISOs): ISOs act as intermediaries between acquirers and merchants, offering a range of payment services and products. Their primary function is merchant acquisition, and they may also conduct preliminary underwriting for merchant applications. ISOs provide ongoing training and support to merchants and operate within regulatory frameworks established by card networks like Visa and Mastercard.

Security Providers: With the rise of e-commerce, security providers play a critical role in reducing risk and securing transactions from fraud. They often employ advanced technologies such as artificial intelligence and big data analytics to enhance payment security.

Digital Wallets: Digital wallets allow consumers to digitally store and spend funds, including real money linked to payment cards, loyalty points, or discount coupons. They offer the convenience of cardless payments and store various items like boarding passes, movie tickets, and loyalty vouchers. Key players in this sector include Apple, Samsung, Google, Alibaba, Walmart, PayPal, Venmo, and Block’s Cash App. These wallets use technologies like open APIs and smart ledgers (blockchain) for better integration and management of digital payments.

Terminal Manufacturers and Vendors: Terminal Manufacturers and Vendors develop and distribute Point of Sale (POS) terminals for various sectors like retail, hospitality, and financial services. Their core function is designing and producing hardware that enables electronic payment processing. These companies offer a range of products including traditional card readers, mobile POS systems, and advanced smart terminals. They often provide software and API support to enhance the functionality of their devices. Additionally, they offer technical support and maintenance services to ensure the smooth operation of their terminals. These vendors must comply with industry standards and security protocols to ensure safe and reliable transactions.

The complexity can make it hard to grasp the ins and outs of this space, but let’s look at some concrete examples and explore the roles of key players like Visa, Mastercard, Fiserv, Adyen, Amazon, and PayPal within this chain.

Research anytime, anywhere

The #1 app for qualitative research. Live earnings calls, AI chat, transcripts, and more. All for free.

Visa and Mastercard, as card networks, are central to the payments ecosystem. They facilitate transactions among consumers, merchants, processors, and banks, overseeing processing activity, settling sales, and regulating compliance policies. They provide electronic networks for communication and transaction processing, charging fees to issuing and acquiring financial institutions. Unlike American Express and Discover (owned by Capital One), which issue their own cards and consolidate functions typically provided by merchant banks, card issuers, and card networks, Visa and Mastercard work with multiple independent entities on both the acquiring and issuing sides.

Fiserv functions as a payment, or credit card, processor. It works behind the scenes to provide payment processing services to merchants. This includes establishing merchant accounts, processing various card payments, managing processing, and implementing anti-fraud measures. Processors like Fiserv may be associated with acquiring banks or operate independently.

Adyen

Adyen serves as a full-stack payment gateway, offering a comprehensive platform for e-commerce companies that includes gateway services, risk management, and front-end processing. In 2019, Adyen expanded its services with Adyen Issuing, enhancing its in-store and online processing and gateway functionality. Adyen’s diverse roles include being a payment service provider, acquirer processor, owning an acquiring license, and even selling POS terminals, making it a versatile player in the payment value chain.

Amazon

Amazon Pay allows customers to use their existing Amazon accounts to make purchases on various retail sites. This service streamlines order management and payments across different websites, providing a familiar checkout experience through the Amazon interface. Amazon Pay ensures that eligible purchases are protected, and it offers convenience across devices including mobile and desktop.

PayPal

PayPal has through the years diversified its roles in the payments value chain. Originally a platform for online funds transfers, the company has grown through acquisitions like Braintree and Venmo. Braintree provides payment gateway and processing services, while Venmo offers peer-to-peer payment solutions. PayPal has also ventured into in-store payments, acquiring Paydiant to enable mobile wallet capabilities in merchants’ mobile apps and iZettle for modern in-person payment solutions.

In Conclusion

The payments value chain is a rich tapestry of interconnected entities, each playing a critical role in facilitating smooth financial transactions. Companies like Visa, Mastercard, Fiserv, Adyen, Amazon, and Paypal have carved out specific niches within this ecosystem, contributing to its evolution and efficiency. As technology advances, this landscape continues to grow more intricate, reflecting the ever-changing dynamics of the digital payment world.

)

)

)

)

)

)