)

)

)

Business philosophy30 May 2024

The Rise of Athleisure

A closer look at the athleisure trend from a business standpoint, the driving factors behind its rise in popularity, and the companies involved.

It all began with a runner chasing a feeling. Fifteen years later, that pursuit of another running sensation forms the foundation of a Swiss premium sportswear brand that now stretches from marathon racing to tennis and everyday wear. What started as a garden-hose experiment has become one of the fastest-growing names in the industry. This is the story of On.

The story of On begins with a competitive runner from the Swiss Alps named Olivier Bernhard. For nearly two decades, he competed among the global elite of endurance racing, winning three duathlon world titles and multiple Ironman races. By the mid-2000s, he was nearing the end of that run.

As he began winding down his racing career and transitioned into coaching, a side project started to take shape that grew directly out of his experience in its later years. Persistent aches, especially around his Achilles, and a sense that there was “room for another running sensation” (Behind the Brand, 2022) made him wonder if a different kind of sole could change that. So he started experimenting.

Working with a like-minded Swiss engineer named George, Bernhard began experimenting with radically different sole constructions. In one early prototype, George sent back a pair of Nike shoes with pieces of cut-up garden hose glued vertically along the sole. The shoes looked absurd, but when Bernhard took them out for a test run, he was surprised by how good they felt. Sensing that the idea had real potential, he immediately began listing adjustments he wanted to try.

The improvised hose shoe delivered something he hadn't felt before: a soft, forgiving landing followed by a distinct, springy push-off. It made him wonder what a fully developed version of that idea could become. Could this strange, ugly prototype be refined into a lightweight shoe that reduced impact on joints while preserving speed? Could it even help prevent some of the injuries that had shortened his career?

Over the next few years, Bertrand and George iterated obsessively in pursuit of the perfect running shoe. Once the shoe came closer to what he had envisioned in terms of performance, Bernhard took it to the heart of the industry: Nike, Adidas, and Puma. One after the other rejected him. In hindsight, Bernhard has admitted that he fully understands why the big players turned him down. The prototype still looked ridiculous and was nowhere near ready for commercialization.

But the rejections didn't shake Bernhard's belief in the shoe. Instead, he decided to do it on his own and build a shoe company from the ground up. Around this time, he approached his former agent, Caspar Coppetti, and asked him to try the shoe. After some initial skepticism had been washed away by a trial run, Coppetti started to share Bernhard's conviction. The pair then approached their friend David Allemann, who brought deep business experience and shared their passion for the outdoors. He, too, became convinced of the potential.

In January 2010, the trio founded On, each investing $150,000 and agreeing to forfeit their shares if they took another job within the next three years.

Named for the sensation that it made runners feel “switched on,” the trio set out to turn the strange prototype into something a serious athlete would actually buy. Bernhard and a small team of engineers worked closely with countless runners who tested early versions and provided feedback. Slowly but surely, that tweaking pursuit in search of a new running sensation would name the company's tagline that lives to this day: running on clouds.

What had begun as a garden hose glued to a Nike sole evolved into discrete “clouds” under the midsole. On acquired the underlying technology from George, and refined it into something both functional and manufacturable. The goal remained the same: more power on push-off, more cushioning on landing. That system became CloudTec, circular rubber elements on the outsole that compressed on impact and then locked into a firmer platform for toe-off. It still didn't look like any other running shoe, but it finally looked intentional.

Beyond the sole, the team wanted a design language that matched the innovation underneath. They hired a designer with no footwear background, confidently viewing the lack of industry experience as an advantage and opportunity. Together, they sketched a minimal, clean, and technical aesthetic, far from the loud styles that dominated running in the early 2010s. The result felt different and durable. After arranging partnerships with specialist suppliers and manufacturers in China, they moved into production. The first shoe, the Cloudsurfer, launched shortly thereafter.

From day one, the founders aimed far beyond Switzerland. As David Allemann explained in Entrepreneur (2022), “You can't think of a running shoe brand as local, just as you can't now think of an electric car company that way. It was very clear to us: if we want to have a fighting chance, we have to build a global brand from the start.”

That mindset shaped their go-to-market approach. Instead of chasing broad consumer awareness, they targeted the communities they knew best: endurance athletes, coaches, and specialty running retailers. If those groups adopted the shoe, they believed broader demand would follow organically and hold up more sustainably.

A catalyst for expansion came “a couple of days after we founded the company,” when the team took five or six samples to ISPO, one of Europe's leading sporting goods trade shows. On won the ISPO BrandNew Award and, as Caspar Coppetti later recalled on How I Built This (2024), “We left the show with over half a million Swiss francs in orders.” That early validation gave On instant credibility with retailers and brought in liquidity to support the expansion that was to come.

With that early momentum, the team brought its shoes to races across Europe, pitched specialty retailers, and set up at expos. The approach worked. Word spread quickly, and within a few years, On had established itself in Europe's key running markets, while gradually entering selected partnerships with wholesalers in the U.S. As the specialist network expanded, the company added another channel as it launched its own e-commerce platform across most of its markets.

Building on the Cloudsurfer's success, the lineup expanded with models like the Cloudrunner and the Cloudracer. They shared the unmistakable CloudTec sole but offered distinct performance profiles, helping the brand appeal to a broader spectrum of endurance athletes.

By 2013, On was growing quickly across its key markets. That year, the company hired Marc Maurer as COO and Martin Hoffmann as CFO. These two leaders would help shape the next decade as On put more structure behind its momentum, from supply chain and finance to international expansion.

Its first real breakthrough came that same year, when Belgian triathlete Frederick van Lierde won the Ironman World Championship in Kona, Hawaii. During the closing marathon of his eight-hour race, he was wearing an unreleased On prototype. Bernhard later described how he spent those final miles “praying and sweating like hell” that the shoes wouldn't fall apart (How I Built This, 2024). When van Lierde crossed the finish line, the young brand earned a level of performance credibility it could never have bought with marketing.

Expansion continued through the mid-2010s, as On extended its presence across Europe, North America, and Asia. During these years, it opened a U.S. headquarters in Portland and its first Asian office in Yokohama, strengthening local distribution while keeping product, design, and brand direction centralized in Zurich.

With the release of the Cloud in 2014, adoption continued to grow. More and more athletes were discovering how On could improve their performance, but the Cloud also started to draw in people beyond the running community. Compared with earlier models, it pushed On's design language a step further with an even lower profile and a shape that fit more naturally into everyday wear, yet still featured the distinctive CloudTec pods that guaranteed its performance. At the time, attracting beyond runners wasn't the founders' intention. As Caspar Coppetti recalled in How I Built This (2024), On's identity was firmly rooted in performance running:

“We were going to be a running company, and actually, it pissed us off when somebody was wearing our high-tech products in the street with jeans. It really bugged us. It's like buying a Porsche and going shopping.”

But consumer behaviour was shifting, and On could see it firsthand. In 2016, the company seized the opportunity to expand into a wider variety of shoes, but also into apparel. That step meant it would no longer be “just” a performance running brand. In doing so, On mirrored a path that giants like Nike and Adidas had taken decades earlier: first establish credibility in performance footwear, then extend to the full body. From a running shoe brand to a sportswear company.

The years that followed continued in that direction with a broader assortment, more use cases, and a wider customer base. New shoes arrived, including the Cloud X, explicitly marketed as “made for everything”, alongside the Cloudventure, Cloudflyer, Cloudflow, and Cloudswift. Around what On calls its footwear franchises, On built a head-to-toe offering: technical tops, jackets, and tights designed as a lightweight layering system, later joined by more casual pieces that pushed the brand deeper into the everyday wardrobe.

By the late 2010s, On had come a long way. The company was selling millions of pairs annually, dominating specialty running channels in Switzerland and Germany, and gaining momentum in North America. In its first decade, it had nearly doubled revenue every year and had sales operations in more than 50 countries.

As it entered the next decade, On was on a clear upward path. Then the world changed in ways that would accelerate its rise and reshape the industry around it.

Before moving into the next chapter of the story, it's worth stepping back to look more closely at the On brand.

What sells running shoes? Quality and performance, of course, are the foundation. But just after that comes the strength of the brand, which is often the deciding factor for many consumers. Once a product has proved itself, the brand takes over. It makes the first impression, creates a sense of belonging, and shapes the set of associations a customer identifies with. The bestselling running shoes have mastered both. At that point, the purchase is less about discovery and more about seeking out a specific brand.

From the beginning, On invested heavily in both sides of that equation. The product came first, shaped by passionate runners and refined through years of obsessive testing. The brand came later, but has ever since they began sketching on the first Cloudsurfer, been equally important. Its distinctive CloudTec technology covers both quality and brand, serving as both an engineering solution and a marketing asset. It was divisive, but that was the point. The product had to do more than perform; it had to be recognized as something different.

That technology was the foundation of its growing portfolio of product franchises, each building a distinct identity within the broader brand. The design language, always prefixed with "Cloud", became a clear part of the identity. Many of these franchises made their debut years ago but continue to drive growth through iterative updates rather than replacement. By doing so, they can last beyond the typical seasonal product launch cycles. As co-founder and co-Chairman, David Allemann explained at On's Q4 2024 earnings call:

"These aren't just shoes, they're brands in their own right, allowing us to connect with diverse communities and tastes, building lasting loyalty."

The company's marketing strategy has differed from the traditional sportswear playbook. Just like how it approached consumer awareness in the early days, prioritizing organic spread of On rather than pouring money into advertising. On established itself on the biggest running scenes because the product earned it, not because it was the loudest or had the deepest pockets. That strategy has worked remarkably well over both the short and long term, as years of earned awareness have compounded into a level of brand equity few consumer companies achieve in such a short period of time.

Athletes played a central role in that compounding. After Frederick van Lierde's Ironman win in 2013, more elite names followed. By the mid-2010s, Spanish triathlon legend Javier Gómez Noya was racing in On, and British Tim Don set a then-Ironman world-best time in 2017 wearing the Cloudflow. Each performance reinforced the legitimacy of a brand still expanding far beyond the Swiss Alps.

The strategy of backing top athletes became even more explicit in 2020, when On launched the On Athletics Club (OAC), a dedicated professional training group for some of the most promising young endurance athletes. With OAC, On set out to build a distinctive team spirit and offer 360-degree support in what is otherwise an individual sport environment. The initiative has quickly become one of the company's most powerful brand engines. Based in Boulder, Colorado, and later expanded to Europe and Oceania, the model is simple: support the athletes, create high-performance environments, and let victories in On shoes do the marketing.

The link between performance and brand was on full display at the New York City Marathon in November 2025, when Hellen Obiri, racing in the Cloudboom Strike Lightspray, regained her title and set a new course record with a 2:19:51 win. The Cloudboom Strike Lightspray is built on On's Helion HF superfoam platform, a higher-energy evolution of its cushioning concept with a full-length, carbon-assisted midsole.

The shoe is topped with a LightSpray upper, an ultra-light, seamless shell sprayed by a robotic system directly onto a form. Together, the midsole and upper represent a leap beyond On's original CloudTec design, engineered specifically for marathon racing.

On the Q3 2025 earnings call, co-founder and co-Chairman, Caspar Coppetti called Obiri's win “the ultimate proof point” for the company's newest technology and explicitly connected it to consumer demand: “All the things we do around running, like Hellen Obiri winning the New York City Marathon, these things translate into more demand from consumers.”

As the product portfolio broadened, so did the ambassador mix. Beyond pure performance running, On has increasingly added athletes in adjacent disciplines and, more recently, a small number of lifestyle-leaning collaborators outside sports. These moves have widened the brand's reach while remaining focused on performance. We'll return to that balance later.

Meanwhile, On entered another performance arena by launching its tennis vertical. By the late 2010s, the company had expanded into a dedicated tennis footwear and apparel line, which ever since has grown significantly and attracted major names including Iga Swiatek, João Fonseca, and Ben Shelton – whose 2023 U.S. Open run helped drive nearly 4x year-over-year growth in U.S. direct-to-consumer (DTC) tennis apparel for that quarter (sourced through Quartr Pro).

The origin of that tennis push, though, didn't come from inside the company. It came from the best possible source for a Swiss performance brand. And one whose name fitted perfectly with its premium aspirations and Swiss roots: Roger Federer.

Premium is an emotion formed in the minds of our fans.— Martin Hoffmann

The Federer story is now part of On's internal mythology, not just because of the name attached to it but because of how much it would end up changing the course of the company. After buying a pair of shoes on his own, he reached out to meet the team behind them. A dinner in Zurich eventually led to his joining the company in 2019, first as an investor, then as a creative partner on what would become the ROGER line.

His involvement gave On instant global visibility beyond running and helped anchor its emerging tennis vertical in the most credible way possible. Since then, he has played a meaningful role in shaping that franchise, which has grown into one of On's most successful. As a side note, the roughly 3% stake Federer acquired is reported to exceed the prize money from his legendary tennis career.

Federer was a natural fit. He embodied the qualities On wanted the brand to project and, of course, he shared its Swiss background. From the beginning, On's Alpine origin has been part of its identity, signalling precision, quality, and technical credibility. Beyond the occasional confusion with Sweden, Switzerland tends to evoke images of innovative craftsmanship, luxury watches, well-run banks, and snow-covered mountains.

On leaned into its Swissness early and made it tangible throughout its operations, consumer-facing offer, and company branding. As Thilo Brunner, On's Global Head of Design, explained at the company's 2023 Investor Day:

“...Swiss design has been known for being quite rational, boiling down things to a very -- to the very essence and to be quite minimal, yet playful in a functional sense. And this always has been the case, whether it's been with product design, typography, architecture, and it happens very consciously, and we take this very seriously at On.”

That mindset traces all the way back to Olivier Bernhard's first garden hose prototypes. The tools and scale have changed, but the philosophy hasn't. Innovation is still anchored in Zurich, where engineering, design, development, and testing take place in-house. Although manufacturing is outsourced to third-party partners (footwear produced primarily in Vietnam, and apparel and accessories sourced across Vietnam, Slovenia, Portugal, Turkey, and China), the Swiss foundation remains the compass for every product that reaches a shelf.

On's premium brand comes with a premium brand strategy running across its entire operations. The company has maintained minimal discounting from the start, using that pricing power to fuel its brand equity and signal scarcity. Distribution follows the same logic, where wholesale partners are selected carefully, with strict expectations for presentation, pricing, and environment. In an industry where many brands lean on discounts to chase volume, On's approach has set it apart.

While many historic luxury brands became premium through decades of accumulated heritage, On attempted the reverse by establishing a premium positioning instantly. Its ambition “to be the most premium global sportswear brand” is clearly more than just a branding message, but an operating principle shaping everything from product development to pricing to distribution.

Our commitment to full price sales is first and foremost, the commitment to build the brand long term.— Martin Hoffmann

In 2020, the pandemic accelerated trends that On was already positioned to capture. Gyms closed, indoor sports halted, commute patterns disappeared, and suddenly, billions of people's habits were disrupted.

“We believe that health and sport will become even more important to the consumers moving forward. I believe very few people globally have not thought about their own health almost on a daily basis in the last 6 to 8 weeks. So the move towards a more health and exercise-oriented global population has been accelerated through corona.”

– Kasper Rørsted, former CEO of Adidas, at its Q1 2020 earnings call.

Running became an accessible, outdoor, and, importantly, individual activity to lean into. But not only did running surge, so did hiking and other outdoor activities. Former Under Armour CEO Patrik Frisk summed it up well at its Q1 2020 earnings call:

“... while many things are on lockdown, inspiration, wellness and fitness are most certainly not quarantined.”

Shoe sales across brands climbed sharply, and athleisure – sportswear worn as everyday attire – became the default wardrobe. Lockdowns turned homes into workspaces, and the line between performance and casualwear blurred. Consumers who had never run a mile gravitated toward running shoes because they were comfortable, versatile, and signalled a certain lifestyle. Almost every company selling into this category benefited.

“We see an even more pronounced fashion shift towards leisure. The increase in workplace flexibility is here to stay. And the majority of companies plan more and more permanent remote working. And of course, when you sit at home, you don't wear your suit, you don't wear your tie, but you tend to wear sneakers from adidas or hoodies, and that is definitely helping paving the future way for us.”

– Kasper Rørsted, former CEO of Adidas, at its Q2 2020 earnings call.

Nike and Adidas were the two largest beneficiaries, thanks to their broad head-to-toe assortments. But they were far from alone. Lululemon, Under Armour, Hoka, New Balance, ASICS, and others also rode the wave.

On was part of that group. From a pre-pandemic baseline, revenue grew by roughly 60% in 2020 and then another 70% in 2021. In the midst of this momentum, On completed an IPO in September 2021. Just over a decade after its founding, the company had gone from niche upstart to the public market stage, listing at a market cap of around $7 billion. By the end of the first trading day, the stock was up nearly 50%.

Notably, the early executive team – Olivier Bernhard, David Allemann, Caspar Coppetti, Marc Maurer, and Martin Hoffmann – retained control through a dual-class share structure. They held roughly 15% of the shares but more than half of the voting power through Class B shares that carried 10 votes each. Transfer of those shares was restricted by a shareholders' agreement that gave the other early members a right of first refusal on any intended sales.

Now as a public company, On continued to benefit from the surge in demand, strengthening its e-commerce capabilities, scaling operations, and expanding its assortment. As stores reopened, its growing retail network was in place to catch the upswing. Apparel also began to play a larger role, but On navigated that shift carefully, maintaining the premium positioning that had defined the brand from the start.

The same pattern played out across the industry. The running trend stayed strong, and athleisure showed no sign of slowing. Large brands were performing well, smaller brands were growing fast, and consumers couldn't seem to get enough sportswear.

“These are times when strong brands get stronger. The structural tailwinds we're seeing, including permanent shifts towards digital, athletic wear, and health and wellness continue to offer us incredible opportunity.”

– Matthew Friend, CFO of Nike, at its Q2 2021 earnings call.

But the incredible opportunity would soon prove less permanent than it appeared. The entire sportswear industry had benefited from an expanded market created by a sudden shift in consumer behaviour. The real test would be which brands could sustain their momentum if and when the boom ended.

In hindsight, the pandemic years were a period of extraordinary tailwinds, and most consumer brands scaled production as if those conditions would continue. The initial problem was timing. Lockdowns disrupted manufacturing and logistics, creating supply bottlenecks. Companies simply couldn't meet demand and responded by ordering even more. The quotes below capture the mood of the moment (sourced through Quartr Pro):

“And our first quarter financial results would have been even stronger with more available inventory supply.” – Matthew Friend, CFO of Nike, at its 2021 AGM.

“... our brands are incredibly well positioned across the globe, but demand continues to outpace our current ability to supply it.” – Dave Powers, former CEO of Deckers Outdoor, at its Q3 2022 earnings call.

“If anything, we wish we had more stock given the strong demand for our products…” – Harm Ohlmeyer, CFO of Adidas, at its Q2 2021 earnings call.

“I continue to believe that demand for our brand is outpacing supply, and our business could have been even stronger without the supply chain challenges.” – Calvin McDonald, former CEO of Lululemon, at its Q3 2022 earnings call.

When the supply chain eventually began to improve and delayed shipments finally hit inventories, they did so into a market that was already starting to change. The prior years had been generous to almost every sportswear brand, but reality was now catching up as demand for the very products that had boomed during the pandemic began to soften.

First, consumer spending began to normalize. People redirected money toward experiences and refreshed their wardrobes in ways that didn't necessarily favour performance footwear or athleisure. Gyms reopened, outdoor training declined as a result, and inflation added another layer of friction by making discretionary purchases more considered.

All of this collided with lingering supply chain disruptions and over-ordering from the 2020-2022 period, producing a classic bullwhip effect: too much inventory, product landing at the wrong time, and a messy, drawn-out clean-up cycle of promotions and discounting across the industry.

Suddenly, brands were no longer competing in an expanding market. They were fighting for a share in one that had stopped growing, just as supply was at its peak. Under Armour's interim CEO, Colin Browne, summed up the events at its Q1 2023 earnings call:

“To be fair, we've seen some unusual shifts in the retail space over the past 2 years. In 2020, the world shut down for long periods, creating significant revenue headwinds. In contrast, 2021 saw incredibly high pent-up demand, which drove substantial revenue and historical margin gains across our sector. In 2022, following repercussions from last fall's lockdown, we believe an overabundance of product is about to hit the market, specifically as supply chain starts to recover from last year's disruptions.”

The challenges and consequences were severe for most companies that had thrived during the boom: elevated costs, lingering supply chain aftershocks, and margin compression. Discounting became widespread as the market turned sharply price-competitive. Yet amid this turbulence, not all brands were hit equally. A few managed to retain momentum.

In the footwear department, one of these was Hoka, owned by Deckers Outdoor. Hoka built its brand around maximal cushioning, thick-soled, distinctive shoes that appealed to both runners and everyday consumers. Like a certain Swiss company, it pursued premium pricing with limited discounting and entered the pandemic with strong momentum that carried through much of the difficult period that ensued.

But the brand that stood out most, in both pace and consistency, was On. It entered the 2020s with stronger momentum than almost any peer and, as cracks began to appear across the industry, proved unusually resilient. While larger brands were defending territory and working through excess product, On continued to take share. As CEO and CFO, Martin Hoffmann put it on the Q2 2022 earnings call:

“Despite the macro uncertainty, we currently do not see any signs of a slowing demand for On products.”

From its 2021 base, sales jumped 69% in 2022, 47% in 2023, and 29% in 2024. Some regions grew faster than others and contributed more to the total, but the momentum was clearly global. A large part of the strength came from the brand's positioning: controlled distribution, full-price discipline, and selective wholesale partners all reinforced its premium perception. When the broader market turned promotional, On didn't follow. It maintained pricing power even as retailers discounted aggressively around it. As former co-CEO, Marc Maurer explained at its Q4 2024 earnings call:

"We're less exposed to the normal competitive set that some of the other brands are and we're able to capture basically the potential that comes from our very unique position."

But those years brought significant challenges for On as well. Manufacturing lockdowns in Vietnam and China, supply chain difficulties, logistics delays, and other bottlenecks persisted through the first half of 2022. However, entering the period with strong sales momentum and a smaller scale than the industry giants helped it move quickly and decisively. On secured new production capacity in Indonesia, dual-sourced key materials, and redesigned its supply chain to navigate the worst disruptions. Throughout, management prioritized top-line momentum and retail partnerships over short-term profitability.

By mid-2022, the worst of the disruptions was behind On. Crucially, while many competitors were overwhelmed by excess inventory as demand softened, On's earlier supply constraints meant it avoided the glut entirely. Over the same period, it also continued to push beyond its original core. Apparel gained importance, and new verticals were launched as the company increasingly became a broader performance and lifestyle company, designed to speak to a much wider target group than before.

Through 2023, 2024, and into 2025, On continued to grow faster than the rest of the market. Importantly, it did so without compromising the premium positioning that set it apart from competitors caught in promotional cycles.

Before we get into On's business in 2025, it's worth taking a closer look at how the brand has broadened in recent years. That shift explains both what On has become and where it is heading.

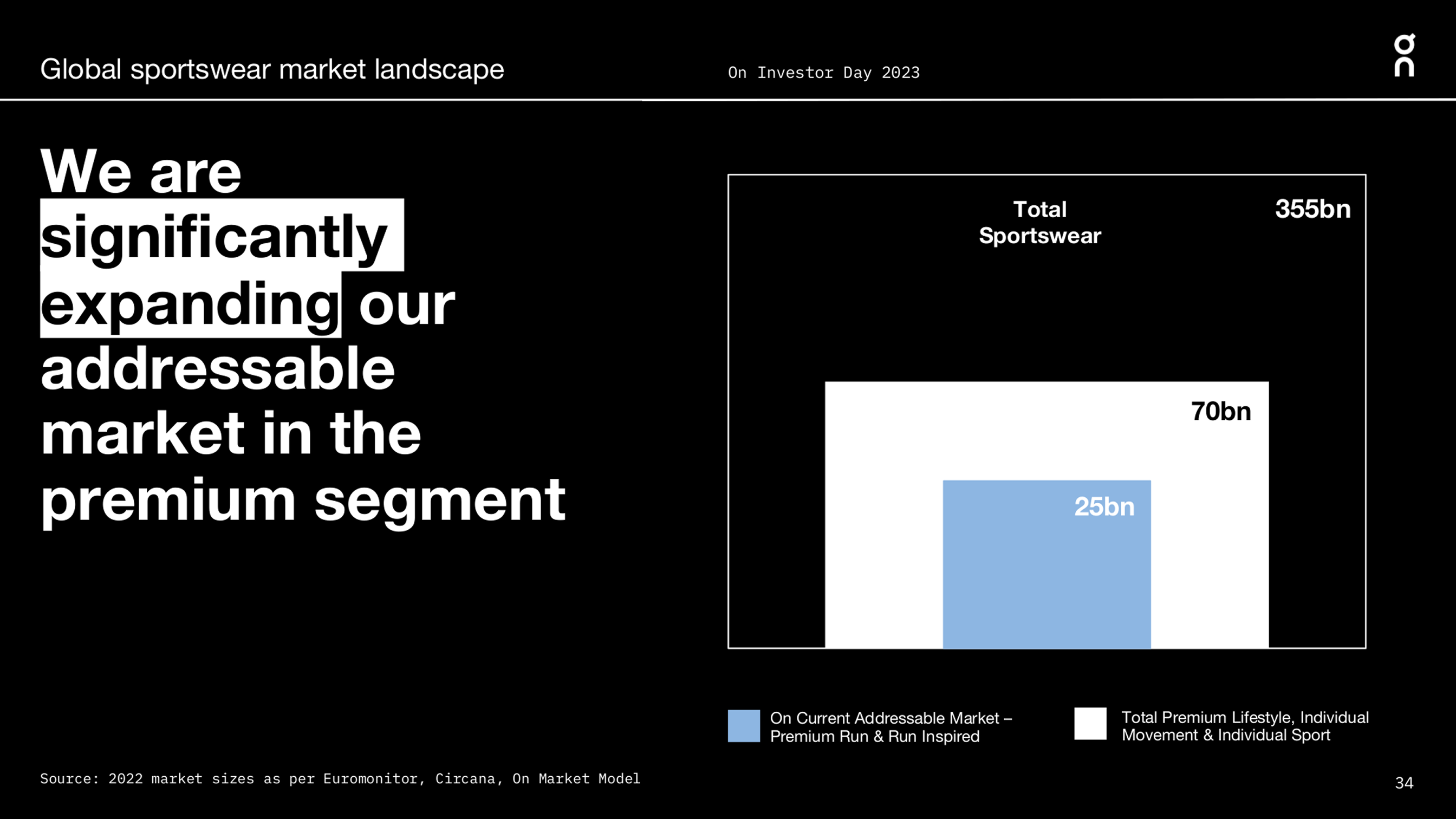

On has steadily expanded beyond its running-only identity. The transition began gradually as the company added new silhouettes and categories, but has accelerated meaningfully in recent years. At its 2023 Investor Day, management made the pivot explicit, outlining a vision to be “the most premium global sportswear brand.” The expansion of the addressable market highlighted the potential:

While running remains the core of both On's identity and its revenue, lifestyle footwear and apparel have become critical to its evolution. From the pandemic years, On's customer base widened while its product portfolio continued to expand. What changed was who could see themselves in that promise. On increasingly designed for more “performances,” each tied to specific communities. By intentionally building for these groups rather than hoping for incidental crossover, it could credibly occupy more parts of a customer's wardrobe and reach a broader demographic.

Athletes remain central to brand credibility, but On has increasingly paired athletic performance with cultural partnerships that resonate with younger, more diverse audiences. The collaboration with Zendaya, announced in early 2024, embodied that approach. She became a creative partner in 2024 and helped promote the Cloudtilt Moon alongside matching apparel. Similarly, Burna Boy joined the tennis lifestyle line, fronting a capsule that leaned more into music and street culture than performance tennis. As CEO and CFO, Martin Hoffmann explained on the Q3 2025 earnings call:

"So if you take Burna Boy and Zendaya, they speak to a Gen Z customer. If you take Hellen Obiri, she builds credibility with all kinds of runners. João Fonseca drives a hype in the brand in Brazil, and I could go on forever. But what is most important is that we are not fishing in the same pond as everyone else."

This generational focus is deliberate. On's broader assortment has attracted younger consumers at a growing rate. Hoffmann highlighted the shift at the Q4 2023 earnings call:

“… we are very encouraged about is that, with our expansion of the product assortment and especially bringing more silhouettes that speak to a younger customer. That's something that we very clearly see in our new customer acquisition. So, just looking at what is the share of customers that is below 30 years old. In 2021, that share was around 24%. Now in '23, the share was already at 29%.”

The transformation is unmistakable. On has moved from serving a niche audience of performance-driven runners to people who simply want court-inspired lifestyle clothing, and everything in between. The common thread is the promise to be the most premium option for “communities defined by how they move,” whether that's on running routes, tennis courts, gym floors, or city streets. David Allemann discussed the widening target group on the Q2 2025 earnings call:

“What we're seeing is that we are no longer just for early adopters. We are now resonating with a much wider audience from established runners to the very young. Our brand strength is over-indexing with Gen Z consumers.”

Heading into 2026, On is widely recognized, both as a brand and by the distinct look of its products. Yet, significant opportunity remains, as Hoffmann noted at the Q3 2025 earnings call:

"And so the first focus of what we are building is to increase our addressable market. I mean about 75% of the people in our markets don't know about On. So increasing the brand awareness is a key first step. But we are not using a shotgun approach to do this, but instead, we are extremely conscious about the different communities and customer groups we are targeting."

We are not fishing in the same pond as everyone else.— Martin Hoffmann

Footwear still drives the vast majority of the business, accounting for around 93% of the total 2.9B Swiss francs (CHF) in revenue in the twelve months to Q3 2025, equivalent to roughly $3.5B. Across its wide portfolio of shoes, nine footwear franchises each contribute to more than 5% of the total.

Many of these sit under the Cloud umbrella, with names like Cloudsurfer, Cloudmonster, Cloudrunner, among others. Only one major line forgoes the Cloud prefix: the ROGER franchise. Each franchise has its own design language, target use case, and loyal customer base.

On's offering is structured across five product verticals (all carrying the Performance label): running, outdoor, tennis, training, and all-day. These verticals have been added over time, with each extending beyond footwear into matching apparel collections. Running remains the core category, still contributing the majority of revenue and continuing to be the fastest-growing vertical.

Running shoes are a category where relationships can last for years. Once a runner finds a shoe that feels as good at mile five as it does at mile twenty and reliably delivers what they expect, switching is rare. For On, that kind of trust turns a single Cloudpulse or Cloudflow purchase into a long-term connection, driving repeat pairs and recommendations to other runners.

Since On introduced apparel in 2016, the category has grown steadily alongside footwear. In the twelve months to Q3 2025, apparel and accessory revenue reached CHF 191M, up 87% year-over-year and representing approximately 7% of total revenue. Each of On's five verticals features a broad range of apparel and accessories designed to complete the look. Running includes performance socks and caps, tennis adds courtside polos and skirts, and lifestyle extends to sling packs and beanies.

Apparel operates with its own design, development, and go-to-market approach, distinct from footwear. On sells hundreds of different apparel pieces across its verticals and, alongside the core range, has made collaborations a successful feature of the portfolio. As David Allemann explained on the Q4 2024 earnings call:

“So we really use these amazing ambassadors for pushing our apparel growth. And so I think that's going to be important as well for the future of apparel, that apparel really has a voice.”

While these drops often include footwear, apparel frequently commands the most attention and acts as a strategic tool for brand awareness and customer acquisition. Hoffmann touched on this at On's Q3 2025 earnings call:

“It's fundamentally reshaping how people view and enter our brand. It's becoming a key acquisition channel, attracting a growing share of first-time customers by also building lasting value as apparel shoppers buy more frequently and with bigger baskets.”

The company's collaboration with Spanish luxury house LOEWE (owned by LVMH) in 2025 exemplified how far the brand could stretch in the premium space, moving close to luxury territory. The capsule collection featuring the Cloudtilt retailed at $590 and "sold out almost entirely within days." Beyond its role in broadening the audience, apparel is also positioned to become an increasingly important contributor to margin expansion, a topic we'll return to later.

On operates through both wholesale and DTC, which consists of its e-commerce platform and its own store network. In 2019, the company was heavily weighted toward wholesale, with DTC representing roughly 25% of revenue. Boosted during the pandemic and steadily rising since, DTC reached 42% of the total in Q3 2025 on a trailing twelve-month basis.

)

DTC plays a strategic role because it is the only place where consumers can access the full On assortment. That makes the sales mix in DTC meaningfully different from wholesale. Management has indicated that apparel represents roughly 20% of DTC revenue, which, given that apparel accounts for only about 7% of the total, underscores how apparel is skewed toward On's own channels.

On's global store network has become an increasingly important part of its strategy, both as sales outlets and as branding hubs. As of late 2025, On operated around 60 global flagship stores in major cities like New York, London, Paris, Tokyo, Zurich, Milan, Hong Kong, Melbourne, and Chicago. Besides these, it operates approximately 30 smaller-format stores in its fast-growing Chinese market.

Even as DTC has expanded rapidly, wholesale has continued to perform strongly. While DTC is more apparel-heavy, wholesale is focused primarily on footwear. By the end of 2024, the company worked with over 10,500 retailers, including key accounts such as Foot Locker, JD Sports, Nordstrom, and DICK'S Sporting Goods. Despite that reach, significant white space remains even within those key accounts, as On is present in only about 40% of Foot Locker, JD, and DICK'S doors, leaving “a multiyear opportunity” still ahead.

On's wholesale expansion has been highly selective throughout. It only adds partners that align with its premium positioning and is willing to walk away if that alignment fades. Over the years, the company has closed doors that did not meet its standards for pricing, presentation, or brand environment.

It's not a negotiable for us to lower price points just to be more relevant to partners.— Martin Hoffmann

From its Swiss base, On has continued to broaden its footprint at a rapid pace. Entering 2026, it sells its products in more than 80 countries across the world. After years of shifting regional weightings, the overall geographic mix is gradually moving toward a more balanced profile.

)

The Americas, dominated by the U.S. (contributing to over 90% of that regional revenue), is On's largest market. In the twelve months to Q3 2025, the region accounted for 59% of total revenue, up from 51% in Q3 2021, both on a trailing twelve-month basis. That increase is a result of On's strategic focus on the U.S., a market that offers scale, strong wholesale partners, and consumers receptive to premium sportswear.

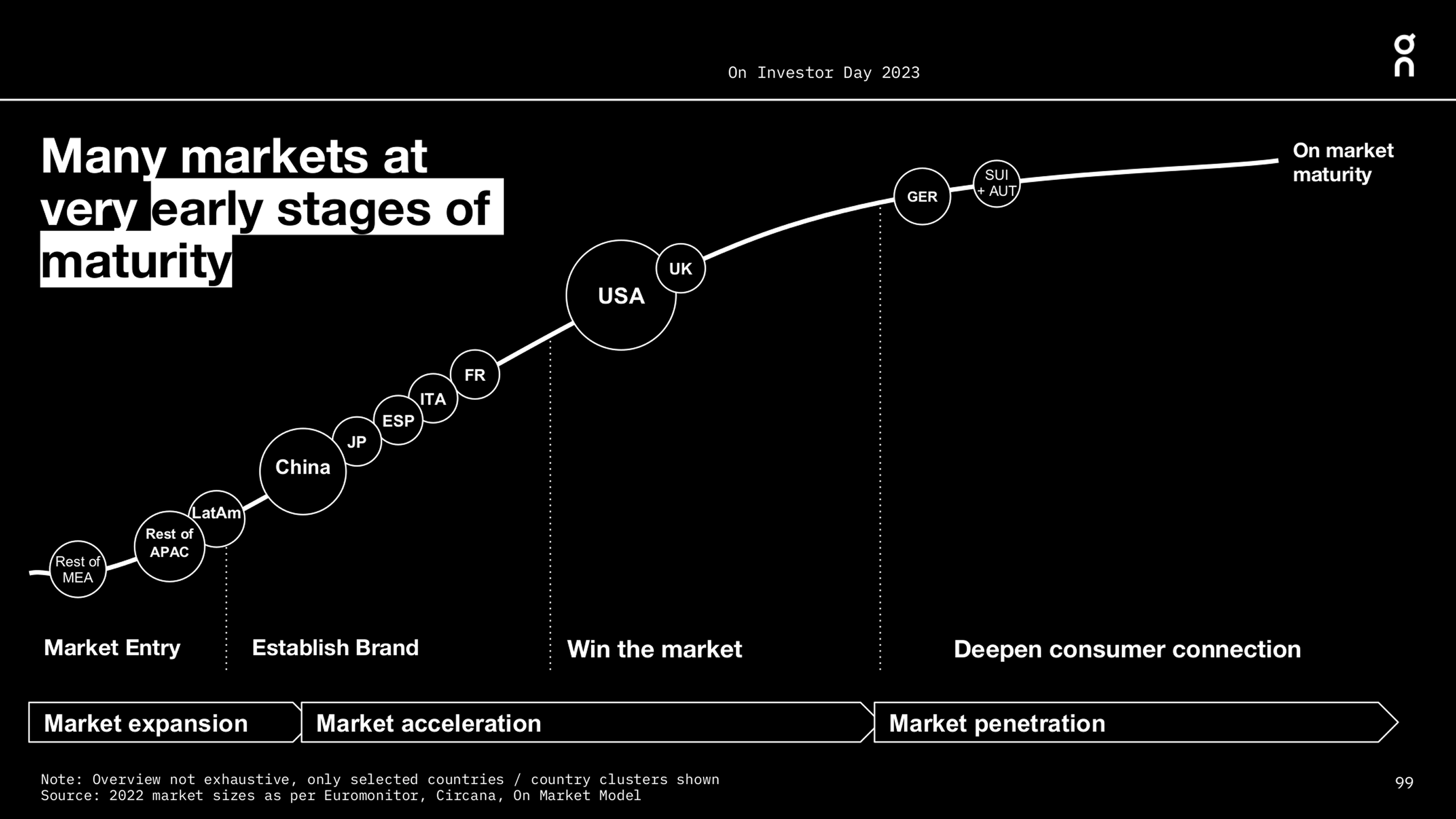

In EMEA, On is in a later stage of penetration but continues to grow strongly. Since the twelve months to Q3 2021, revenue in the region has almost tripled. Despite this, the region's share of total revenue declined from nearly 43% to 25% in the twelve months to Q3 2025. However, as is clear from its growth during that period, it was not because growth stalled, but because the Americas and Asia Pacific grew even faster.

This dynamic was illustrated in a slide at On's 2023 Investor Day, which mapped each region along a market maturity curve. While the most established markets are transitioning from hypergrowth to more normalized expansion, newer markets are now entering the acceleration phase that early regions experienced years ago.

Asia Pacific has clearly moved into that acceleration phase. On a trailing twelve-month basis, Asia Pacific generated 6% of total revenue as of Q3 2021, rising to approximately 16% by Q3 2025.

The Chinese market, which On launched in 2018, stands out within that region. On's premium positioning resonates strongly in China, where a growing middle class and younger consumers are drawn to technical, design-led brands that signal taste and status. Since the pandemic, its Chinese division has delivered consecutive periods of triple-digit growth, driven by both “massive same-store growth” in an expanding retail network and fast-growing e-commerce.

Even after the rapid growth since that 2023 Investor Day slide, the opportunity ahead remains substantial, as Hoffmann noted at its Q3 2025 earnings call: "In China, I think On is very much at the beginning of the journey."

On's financial performance unsurprisingly mirrors the story followed throughout this article. Its revenue in the twelve months to Q3 2025 was CHF 2.9B, implying a CAGR of 45% since Q3 2021. Zooming in on its most recent performance, its trailing twelve months revenue grew by 35% year-over-year, showing that the pace is not slowing down.

Over that same period, adjusted EBITDA has increased from approximately CHF 96M to CHF 535M, growing at a 54% CAGR, with adjusted EBITDA margin expanding from 13.3% to 18.6%. Adjusted EBITDA excludes costs such as share-based compensation (especially elevated after its IPO) as well as non-cash items, including depreciation and foreign exchange effects. Despite those limitations, it remains a useful lens on the profitability of On's underlying operations.

The numbers are the output of everything we've already seen: a distinctive product concept, focused expansion from its Swiss roots, and a brand that has managed to grow quickly while maintaining a disciplined pricing strategy.

)

On's gross margin profile makes its premium strategy visible. While Nike typically operates at around 43-46% and Adidas at 48-52%, On has held close to 60% in recent years. Of course, any comparison across brands comes with caveats: scale, category mix, sourcing footprints, and regional exposures differ meaningfully. But even allowing for those differences, the margin gap highlights the strength of On's model.

“I mean I think on the gross profit margin, it's just super important to understand that the premium business that we are building is the driver behind the gross profit margin. And of course, building a premium business also requires incredible discipline in your inventory management in order to protect the high share of full price sales.

So this is the essence of what we are building. And you have already seen the power of that business model coming to life in the last 2 years with our gross profit margin expanding constantly. And this has really been the result of the pricing power, the full price discipline, a more D2C focused channel mix, operational improvements and then also economies of scale.”

– Martin Hoffmann, CEO & CFO of On, at its Q3 2025 earnings call.

If we place its recent performance against the company's 2023 Investor Day goals, the scale of its overachievement becomes clearer. Back then, management outlined a path to CHF 3.55B in revenue by 2026 (implying a 26% CAGR), alongside a +60% gross margin and +18% adjusted EBITDA margin.

As of late 2025, On is already running materially ahead of that plan, having delivered two consecutive years of 33-34% constant-currency growth, and reaching an adjusted EBITDA margin above 18% a full year earlier than anticipated. Gross margin guidance of roughly 62.5% for 2025 also sits comfortably above the original long-term target, even after absorbing tariff impacts.

Back in 2023, On also communicated its long-term ambitions post-2026, with the main headlines being 20-25% revenue growth and a +20% adjusted EBITDA margin. Those goals were rooted in the same strategy that has guided the company since the early days, including its premium positioning, selective distribution, and creating successful franchises. But also in the newer sources of expansion, such as broader product verticals, deeper regional penetration, and a widening target group.

One of the clearest levers going forward is apparel, both as a customer acquisition engine and as a future contributor to margin expansion. As noted earlier, apparel currently accounts for approximately 7% of revenue. Over the long term, On is aiming to raise that share to over 10%, which, given that apparel is far more DTC-heavy than footwear, should support gross margin as more of the retailer markup is captured in its own channels.

The category is still early and lacks the scale of footwear, explaining its limited profitability so far. But as it grows and more of it flows through On's own channels, management expects apparel to become a meaningful margin driver. As Martin Hoffmann explained on the Q3 2025 earnings call:

“... our apparel business is expected to drive also a superior margin profile into the brand. So we are not only adding additional customers, but also additional profitability.”

The aforementioned figures underline how far On has come in a relatively short time. The challenge in this next chapter is balancing that targeted growth in share and awareness with the premium brand and strategy that made On what it is.

On began with Olivier Bernhard chasing a softer landing and a sharper push-off, experimenting with cut-up garden hoses in the Swiss Alps. Today, that pursuit has led to record-breaking marathon shoes, LOEWE collaborations, and court-inspired lifestyle pieces linked to Roger Federer and Burna Boy. As it turned out, there was room for another running sensation.

Explore our platforms

Leading companies and financial institutions worldwide rely on Quartr to make better decisions faster.

Desktop

API

)

)