Whether you seek to invest in one or not, there are great benefits to draw from studying serial acquirers. When you think of it, their objectives are very similar to those we as investors have: find exceptional companies that can grow with good profitability and cash flows while taking limited risks. Preferably leaders in their niches, with attractive positions in their value chains without being dependent on specific suppliers or customers, and have limited or no exposure to technological risk. And ideally, being able to buy them for reasonable prices. So, what really makes for an exceptional serial acquirer? Join us in taking a closer look at just that, using an amazing research study by REQ Capital, as well as concrete examples from some of the best serial acquirers out there.

Capital allocation, decentralization, and people

“The goal is not to have the longest train, but to arrive at the station first using the least fuel,” renowned Capital Cities/ABC manager Tom Murphy once said. It perfectly describes one of the key aspects of successful serial acquirers – prioritizing efficiency over mere expansion when allocating capital. At large, his approach to running businesses, deeply synergistic with that of Warren Buffett, can simply be described as any capital allocation-minded investor’s wet dream. But there is more to successful serial acquiring than just capital allocation.

In December 2023, our friends over at REQ Capital published an insane 300+ page research study on serial acquirers. It is a must-read. In the study, in addition to the previously mentioned importance of capital allocation, REQ lists decentralization and people as the other two most important sources for extraordinary performance.

So, there is 1) capital allocation, 2) decentralization, and 3) people. But how does this take form in real life – at the offices and shop floors, or “gemba” as the Japanese would call it? Naturally, as investors, we would preferably go to see for ourselves and talk to management, but until that opportunity arises, there is much that can be done from the comfort of our desktops. A great starting point is the research platform Quartr Pro. It essentially aggregates all first-party information from public companies in one place, like reports, slide presentations, and earnings calls and their transcripts, and offers features on top of this. For example, an AI-powered chat basing its answers on this first-party information, as well as time-saving search capabilities.

This enables us to quickly scan all public companies’ reports, slide presentations, and earnings call transcripts in seconds. By 1) prompting the AI Chat and having it explain how different companies are communicating about these different aspects, and 2) searching for various keywords ourselves.

We will get to that, with concrete examples from an international blend of some of the best serial acquirers out there. But first, let’s try to more thoroughly understand successful serial acquirers with the help of the REQ study.

Sign up for Edge

Get curated quality company deep dives every other week.

Why serial acquirers?

First of all, as evident in the study, the long-term share price of Nordic serial acquirers in REQ’s company universe has vastly outperformed the MSCI World Index, OMX Allshare Sweden, and even Berkshire Hathaway. The companies included are Assa Abloy, Addtech, Bergman & Beving, Lagercrantz, Nibe, and Atlas Copco among others, and collectively, the shares of these companies have performed with an average growth rate of 19.4% over the last 20 years.

Source: REQ Caital’s Deep Dive Into Acquisition-Driven Compounders. Slide 12.

What is a serial acquirer?

According to REQ, a serial acquirer is a company that generates strong free cash flows and uses that strong free cash flow to acquire small, often family-owned, private firms. Swedish Bergman & Beving is one of the original Scandinavian serial acquirers and serves as a quintessential example of what a serial acquirer is. The company has over 100 years of experience in acquiring and developing sustainable, profitable companies. Its strategy is based on long-term ownership and achieving market-leading positions in niches it is currently active in through organic growth and acquisitions, as well as in additional niches through acquisitions.

Bergman & Beving labels what it does as “small-scale business on a large scale.” Its organization is purposely built around fully independent subsidiaries, and thus, it seeks the advantages of smaller, more agile businesses – combined with the benefits of being a larger-scale operation. As for management, its philosophy is leaving operational matters and tactics to the management teams on the operating level – where the knowledge is. This is the decentralization aspect of it all, and it seems like a common trait among successful serial acquirers to follow the David Ogilvy saying: “Don’t hire a dog, then do the barking yourself.”

The typical Bergman & Beving company is ideally small or mid-sized (turnover of €5-20 million), a market leader, and has potential for expansion within a growing niche. Preferably, the companies are well-managed with a proven track record of generating strong cash flows and healthy profits in the range of EBIT margins of 15% or more. As for the types of niches, the company defines an attractive niche as 1) limited in size, 2) subject to high barriers to entry, 3) subject to stable growth over time, and 4) sustainable from an ESG perspective.

Then, once one of these well-managed companies is acquired, Bergman & Beving have the motto of, “If it ain’t broken don’t fix it.” The companies are more often than not kept running business as usual. Meaning the profile, company name, and locations are retained. Think of it, the companies being acquired are oftentimes very small in the context. Imagine a behemoth like Bergman & Beving coming in and acquiring a company in your hometown – probably an important employer in the area and an enabler in the prosperity of the town – only to start poking around at everything, changing the name, and possibly laying off someone you care about. Perhaps most importantly, doing this with what is likely the founder’s life’s work.

This is not first class business, certainly not in a first-class way. Bergman & Beving instead focuses on developing the organization based on existing employees, customers, suppliers, and partners. They retain well-functioning processes and systems and, while not forcing synergies with other group companies, they inform about what opportunities might exist. Then they continue building a more solid position in each niche by acquiring other additional companies; something the company calls the Nordic Fortress.

Generalists and specialists

Successful serial acquirers can be specialists or generalists. That is, either they focus on just acquiring companies in one specific niche or sector. Or they are more tilted towards making acquisitions regardless of what type of company it is – as long as the acquisition criteria are met.

Source: REQ Caital’s Deep Dive Into Acquisition-Driven Compounders. Slide 23.

Aforementioned Bergman & Beving is an example of a generalist, and according to REQ, these are characterized by not targeting any specific geographic or sector. They focus on acquiring companies across multiple verticals that may have recurring characteristics or be entirely unrelated. This approach allows for expanded growth opportunities and the development of domain expertise, while still not being confined to any specific sector or geographic area. They prioritize investing in solid businesses regardless of industry, valuing good business fundamentals and potential returns over strict synergy requirements.

Specialists, on the other hand, focus on specific niches or sectors, often centralizing operations to leverage cost synergies and scale economies. According to REQ, these often develop expertise within their respective sectors. An optimal position for a specialist acquirer is becoming the “buyer of choice,” or “preferred buyer,” which in essence means becoming the buyer that potential sellers in the specific sector prioritize going to. Swedish NIBE is an example of a specialist acquirer in the sustainable energy solutions sector. This means that the company through its Climate Solutions, Element, and Stoves segments, has deep domain expertise in this sector. To make the “buyer of choice” stamp more clear, imagine you are considering selling your stove manufacturing company – your life’s work – who would you like to sell it to? 1) A company specializing in that exact space, with a proven track record of owning and developing companies just like yours, or 2) just any other actor who pays the most, with the possibility of risking your colleagues’ jobs, and potentially your entire firm’s reputation. Our guess is that most founders would go with the former.

In his 2009 letter to shareholders, Mark Leonard of Constellation Software lays out the benefits and drawbacks of concentrating on fewer verticals – in essence, becoming more of a specialist acquirer:

“An alternative strategy that we’ve discussed with the board, is concentrating our activities in a fewer number of larger verticals. This would likely mean paying higher multiples for larger acquisitions and paying strategic premiums to accelerate the number of tuck-in acquisitions that we do in any one vertical. Despite the higher multiples (and hence lower returns on investment) associated with such acquisitions, we’d end up with fewer and larger businesses and Constellation would be easier to manage and understand.

We’ve decided to continue with our original “many verticals” strategy, but we are monitoring our ability to keep on scaling up the number of verticals in which we compete. Management are not currently feeling overtaxed, and hate the prospect of paying premiums for larger businesses and tuck-in acquisitions. So for the time being, at least, our shareholders and board will have to contend with increased complexity, and our management will focus on maximizing the long term return on capital.”

While the specialist and generalist acquirers differ on many aspects, REQ lists the following traits that are common for both:

Free cash flow, not debt, to fund acquisitions.

Ability to invest additional capital at high rates of return.

Source: REQ Capital’s Deep Dive Into Acquisition-Driven Compounders. Slide 30.

So then, as REQ defines capital allocation, decentralization, and people as three key enablers for successful serial acquirers, how does this really take form more concrete? Let’s see what we found on these themes using Quartr Pro, starting with capital allocation.

Capital allocation

In the whitepaper called Capital Allocation, Michael Mauboussin and Dan Callahan from Morgan Stanley highlight how the primary task for managers is creating value over the long term. This is done through efficient capital allocation. That is, considering different uses of inputs such as capital and labor, and making them output more than they cost over the long term. In other words, choosing between different opportunities and executing on the most attractive ones.

Buffett lays out in his 1987 letter to shareholders how important it is for managers to be great capital allocators using this example:

“After ten years on the job, a CEO whose company annually retains earnings equal to 10% of net worth will have been responsible for the deployment of more than 60% of all the capital at work in the business.”

In the same letter, he also writes about how managers often lack this capability, which according to him is not surprising:

“Most bosses rise to the top because they have excelled in an area such as marketing, production, engineering, administration or, sometimes, institutional policies. Once they become CEOs, they face new responsibilities. They now must make capital allocation decisions, a critical job that they may have never tackled and that is not easily mastered. To stretch the point, it’s as if the final step for a highly-talented musician was not to perform at Carnegie Hall but, instead, to be named Chairman of the Federal Reserve.”

REQ does not oppose and consequently points out how it is of utmost importance for managers to have proper capital allocation strategies. This allows for evaluating opportunities more systematically and makes sure time and resources always are allocated to where they create the most value. So, whether capital is spent on M&A, organic growth initiatives, dividends, share buybacks, or paying down debt, the focus should always be on creating the most long-term value per share.

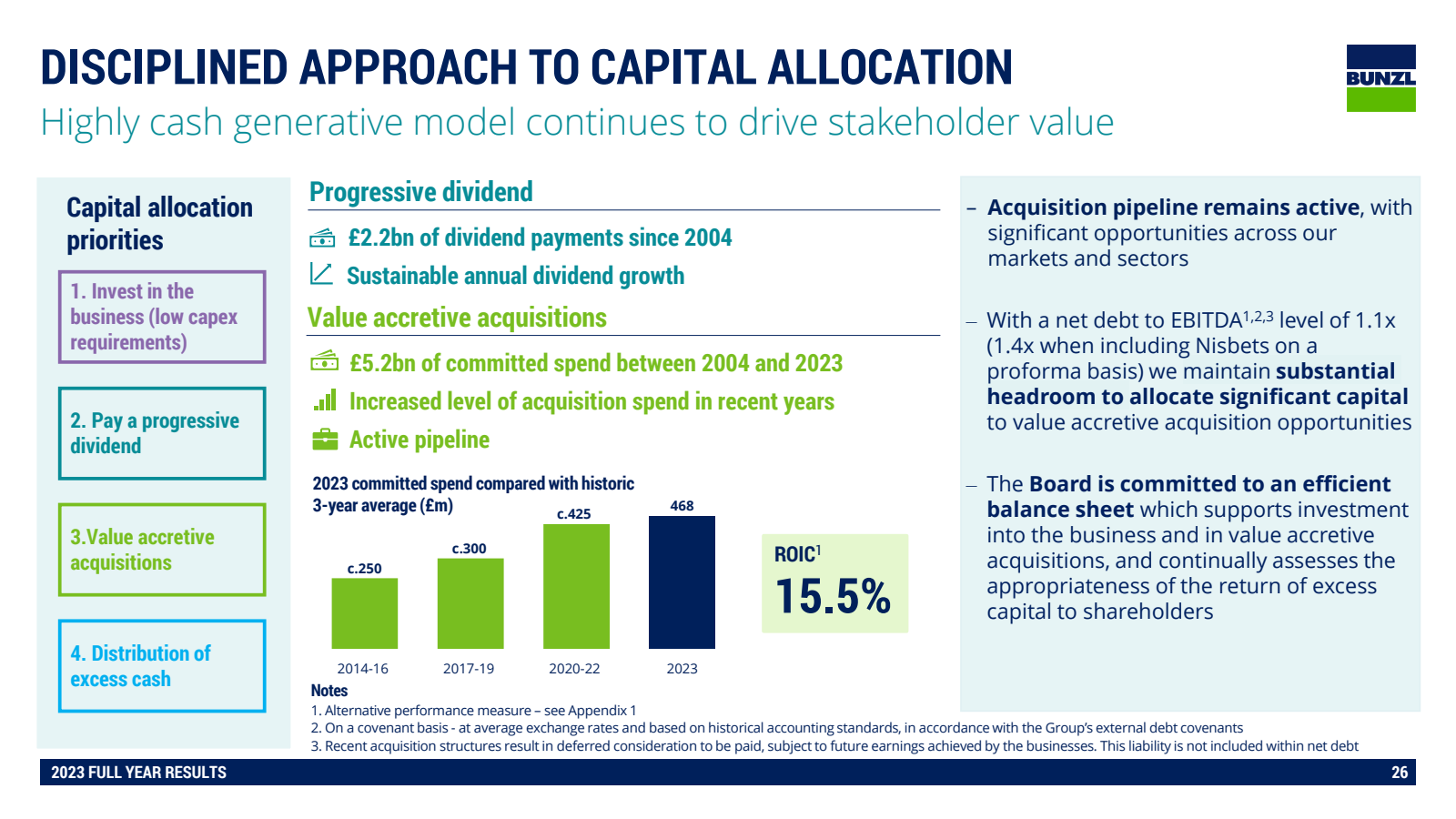

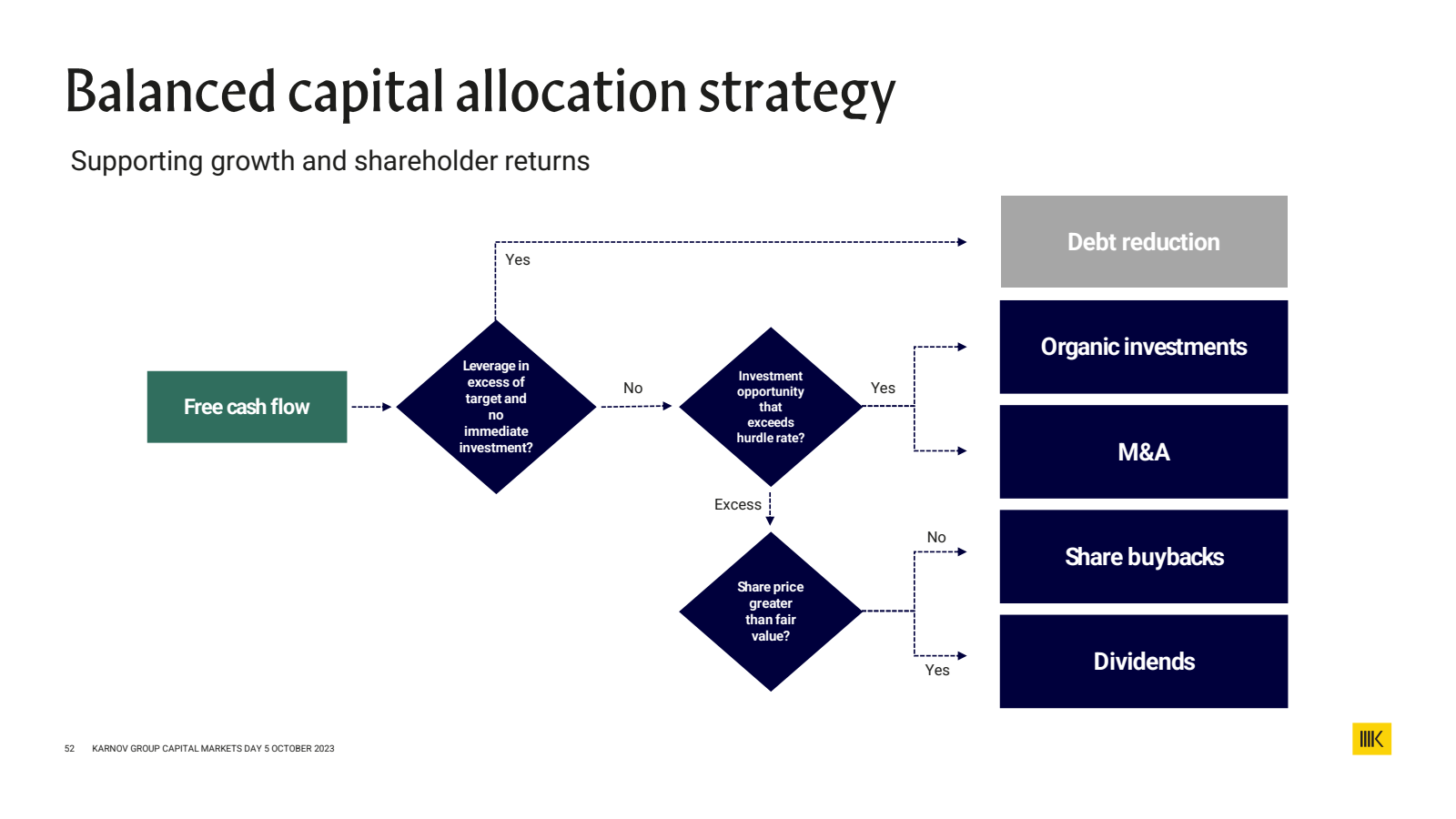

Here are two slides where Bunzl and Karnov Group showcase their approaches to capital allocation:

Source: Quartr Pro – Karnov Group CMD 2023 slide presentation. Slide 52.

And here are some quotes from earnings calls on capital allocation:

How the case of capital allocation is somewhat of an art but how it can be taught:

I think if the folks are enumerate enough to run a business and to understand the ins and outs of an operation, they can understand how a new operation could run. Now maybe they have the bias of believing that they could run anything if their own operations are running really quite smoothly. But I think that over time we're able to teach them and they could learn. It's not -- I mean it's a bit of an art and it's a bit of a science, but given the metrics that we give them, it's hard to not get it really quickly. Again as Mark said, we have our M&A session every year. We talk to our M&A guys pretty regularly, weekly. And the general managers get the feedback from me on a regular basis as well and we get together every quarter. So that feedback loop is always there and I think the information is disseminated well enough that our guys can pick it up.

– Bernard Azarouth, CIO at Constellation Software, Q2 2017.

On different capital allocation priorities:

Yes, our #1 priority for capital allocation is to pour our capital on acquisitions and buy good businesses and make them better. That's generated a long-term return for our shareholders and it's a clear priority. At the end of last year, we had an opportunistic approach to buybacks, our stock had a significant market dislocation and we deployed a significant amount of capital and bought back some shares in the low 70s that looks like a good move at this time. And then the priority 3 for the capital allocation would be a modest, consistent dividend.

– David Zapico, CEO at AMETEK Inc., Q1 2019.

Also on different capital allocation priorities:

Now I'd like to remind you of our disciplined approach to capital allocation. Our priorities are: to invest our cash in the business to support organic growth and operational efficiencies, including investments in technology; to pay a progressive dividend; to self-fund value-accretive acquisitions; and where appropriate, distribute excess cash. Our progressive annual dividend growth policy has returned GBP 2.1 billion to shareholders since 2004. And we are committed to extending our 30-year track record of sustainable annual dividend growth. Acquisitions remain an important driver of growth within our compounding model having been responsible for approximately 2/3 of our historical revenue growth over the last 10 years. Overall, at the end of the first half, we had committed GBP 4.9 billion to acquisitions since 2004. Our successful track record of consolidating our fragmented markets through disciplined acquisitions is demonstrated by our good return on invested capital.

– Richard Howes, CFO at Bunzl, H1 2023.

What the key factors can be when evaluating M&A opportunities:

So what are we then looking for? Well, I think it has been clear from previous presentations as well. We know what we are looking for really. This is a sort of a track record that goes way back. We know when we meet companies if this is going to be an Indutrade company. And the key parameter is really the one in the middle because it's always linked to the entrepreneurs and the management and the key individuals of the companies. They have to match the Indutrade core values. And typically, it's also linked to them buying into our business model. That is actually one of the key differentiators for us versus competition from an investment or an acquisition point of view.

– Jonas Halvord, Head of Acquisitions & Business Development at Indutrade, CMD 2022.

And here William N. Thorndike teaches us in his book “The Outsiders” to approach capital allocation more broadly, using Henry Singleton’s approach as an example. Touching on how to not only look at how the company’s financial resources are allocated but also how the people are allocated:

“If you think of capital allocation more broadly as resource allocation and include the deployment of human resources, you find again that Singleton had a highly differentiated approach. Specifically, he believed in an extreme form of organizational decentralization with a wafer-thin corporate staff at headquarters and operational responsibility and authority concentrated in the general managers of the business units. This was very different from the approach of his peers, who typically had elaborate headquarters staffs replete with vice presidents and MBAs.”

People

As for people, REQ lists how companies that are founder-led, by down-to-earth and pragmatic people who have investors’ mindsets, form a great foundation that might be worth looking closer into. These people seldom give short-term guidance or make excuses for bad performance, and prioritize employees first, then customers, and lastly shareholders. It is also important that management have skin in the game, making their incentives aligned with those of the shareholders.

Research anytime, anywhere

The #1 app for qualitative research. Live earnings calls, AI chat, transcripts, and more. All for free.

Another common denominator of people operating successful serial acquirers is the long-term mindset. Many managers of these companies consider building them the work of their lives, and they very seldom quit because of any other reasons than the inevitable retirement. For example, the current CEO of Indutrade, Bo Annvik, is only the third CEO the company’s had over its almost 50-year history.

Here are some incredible quotes that epitomize what one would like management to sound like. HEICO really sets the bar for leaders in general, and for management communication in particular:

On the extreme long-termism and culture of HEICO:

If we want to build this market share like we're doing, the only way to do it is to build it long term and to really have that level of trust. And frankly, that's how we incentivize our people. I mean, Victor and I each have a whole bunch of businesses that we go and we visit. We know the people, not only running them, but we know the people in charge of the different departments, all the way down very often to people on the shop floor. And we understand who has a long-term culture and who fits with the way we do things and who just plays games. So that's honestly the why and why this happens and we're -- this management team has been here for 33 years. I don't -- I can't think of many management teams, and I certainly can't think of any off the tip of my tongue that have been there for 33 years and plan on being there decades longer.

– Eric Mendelson, Co-President & Director at HEICO, Q1 2023.

Reaping the benefits of what they put in place over 30 years ago:

I think we're just very efficient. We've got a great team. The thing that's interesting is I think that these margins are a result of, frankly, what we did a decade and 2 decades ago. They're not as a result of what we've done in the last year or two when you treat your customers, right, you treat your people right? You get into a virtuous cycle, and I think that's very much where we are. And I think we're reaping the benefits of the long-term culture that we put into place over 20 years ago, 30 years ago, and that's what's driving these numbers.

– Eric Mendelson, Co-President & Director at HEICO, Q1 2023.

Autonomy as a motivating feature:

When you've got really talented people who are running these businesses, who have really mastered their businesses, we find that by giving them autonomy, that's a very intrinsically motivating feature. And that's not something that exists in many companies. If you look at HEICO overall across all of HEICO, we've got roughly 100 business heads and for a company of our size to have 100 people of this talent and skill set where they performed so well and they really enjoy what they do because of way that they're treated, I think that's the real synergy here. It's not going to be from knocking out little costs here and there.

– Eric Mendelson, Co-President & Director at HEICO, Q1 2023.

Decentralization

We apologize for all the Buffett quotes, but sometimes (more like oftentimes) there simply is nothing more fitting. In his 1982 letter, he writes:

“The five people who work here with me – Joan Atherton, Mike Goldberg, Gladys Kaiser, Verne McKenzie and Bill Scott – outproduce corporate groups many times their number. A compact organization lets all of us spend our time managing the business rather than managing each other.”

While this perhaps is on the extreme end, having small and nimble HQ staff and decentralizing the decision-making is seemingly the case for most successful serial acquirers.

Here is Mark Leonard in his 2012 letter, giving us insights into how Constellation Software is managing its head office, and how they continue to keep the staff slim:

We have a 14 employee head office staff composed primarily of finance, accounting, acquisition, tax and legal personnel. Head office provides the Operating Groups with capital allocation assistance and decisions, and tries to disseminate some best practices, a few clear rules, a bit of coaching, and coughs up the occasional partly trained employee for the Operating Groups. Compliance, investor relations, and handling the finance function round out the head office duties. Whenever we feel stretched at head office, we download more of our work to the Operating Groups.

Here is also Mark Leonard, explaining in his 2009 letter how they – while having some best practices to share with the acquired companies – leave much of the authority at the operating level:

“We’ve handled our geometric growth to date by largely abdicating management to the general managers of each of our vertical businesses. We have a very thin overlay of infrastructure at CSI. We count on the fact that with each new acquisition will come general managers who are steeped in their verticals… veterans who have built industry leading (albeit small) vertical market software businesses with great economics. Having owned more than a hundred vertical market software businesses, we also have some best practices that we can share. We coach the managers of our newly acquired businesses in how to grow their businesses and make them even better. As long as we compensate these managers appropriately, and are not tempted to meddle too much, then I think we can scale Constellation for many years to come.”

William N. Thorndike also puts it beautifully:

“There is a fundamental humility to decentralization, an admission that headquarters does not have all the answers and that much of the real value is created by local managers in the field.”

Now lastly, let’s discover some more incredible earnings call quotes found using Quartr Pro, from HEICO, Constellation Software, AddLife, AQ Group, and Lagercrantz. Notice how Mark Leonard speaks about even decentralizing the capital allocation aspect of the business, something that likely is a very important factor in how Constellation is able to keep successfully acquiring companies despite its scale:

HEICO gives tremendous authority and responsibility to people at the operating level, instead of making decisions from 1,000 or 2,000 miles away:

We understand the relationship between the owner of the company and his workforce, his team members. That goes a long way, and we understand how that all works. And that's the HEICO culture. The other thing is we give tremendous authority and responsibility to the operating person. We believe that the person running the -- his organization knows more about his team members, his labor force, his customers, his manufacturer, everything else than somebody in a corporate office, 1,000 or 2,000 miles away. So again, it's the authority that we give them and people who are very talented, respect the fact that we give them that authority. Talented people normally do not like somebody breathing down their neck and over supervising them. What are you doing? What are you doing?

– Laurans Mendelson, Co-President & Director at HEICO, Q4 2022.

Leonard explaining how the operating managers of Constellation Software essentially already are making capital allocation decisions daily, and how they are taught to also apply it in M&A:

Any operating manager inside of a company like Constellation does do capital allocation every day as they do R&D, sales and marketing on initiatives, because those initiatives don't pay off for 5 to 10 years. And so they are, by their very nature, investing now for a payoff many years down the road, and that's the same thing that you do when you do an acquisition. It's just a make-or-buy decision. And so I think we've got people who are naturally predisposed to be capital allocators because they've been in the software business with very long-time horizons, and we're just teaching them some of the nuances that come along with mergers and acquisitions, and that's why we're off site today. About 1/3 of the people here are business unit managers who are trying to figure out how they can deploy their capital, so that they end up running something bigger and hopefully more successful.

– Mark Leonard, Founder & President at Constellation Software, Q3 2015.

The power of decentralized capital allocation, making the M&A problems at the head office go away:

So the best way to answer it is to say you have a culture of not managing and monitoring. What we really want are a collection of small teams that are self-managing, run by trusted individuals with experience and integrity. And gathering together 200 leaders that have those characteristics and getting them to run business units is a nontrivial task, but it's also one that, as that high wheel starts going and working, tends to be a thing of beauty. You have one business unit manager, and if they can buy an equivalent business in the next 3 to 5 years and coach it to perform as well as the one that they're currently running, then all of my M&A problems go away. All of my integration problems go away, and it becomes an organization where you just need the ability to reach into the occasional faltering business unit and provide coaching or sometimes replacement managers. But for the most part, it's self-managing and self-maintaining. And that's what we hope to get to. What it does require is that those operating managers become capital allocators, so a task of teaching capital allocation to people who perhaps have come up through the ranks and that has not been their natural activity.

– Mark Leonard, Founder & President at Constellation Software, Q3 2015.

Great insight into how a local manager at AddLife thinks about Decentralization:

I'm responsible for Finland and the Baltic countries, if we look at the market environment, business culture, competitors, their strategies in Finland and compared to that with Estonia and Lithuania, they are completely different. So we need a lot of local knowledge to operate in that environment. So even though AddLife does have a lot of business understanding market intelligence in the headquarters, I would say, it's the decentralized model that is really the key to the success. When we can decide ourselves locally based on the information we have in the teams, we can actually be very agile and fast in making the decisions. And then the outcome is that we are a few steps ahead of the competition. And those are crucial steps quite often. And I would also like to emphasize that from the motivation perspective, the decentralized model is excellent for the whole company, the management and the whole team when we have the freedom to make important business-related decisions locally. And of course, carry the responsibility of the consequences. It really increases commitment. And in the end, it's really great if you deliver good results to say proudly that it was our team who really did it.

– Jussi Kurittu, Managing Director at Triolab (an AddLife subsidiary), CMD 2023.

Another quote from AddLife, this one from the CEO perspective:

We will, by all means, stay with the decentralized structure, no centralized ERP system for sure. That is the completely wrong way, the way we look at things. We want the companies to drive their business based on their local knowledge, their product knowledge, their deep understanding of the organization and culture that is working really, really well. We support them in that, of course, but we will not drive that from a central level.

– Fredrik Dalborg, President & CEO at AddLife, CMD 2023.

Being quick to adapt to an ever-changing world thanks to a highly decentralized model:

So I think we have a very strong business model. It has been working for 30 years, and we have been through -- we have been working with high competition for a very long time. We have a very broad customer base with -- I believe it's more than 4,000 customers. So I think the business model works. It's proven, and we will continue to work as before. A lot of things are happening in the world, but I think we are very quick to adapt to those changes, thanks to our highly decentralized business model. So now I'm not worried, actually.

– James Ahrgren, President & CEO at AQ Group, Q3 2023.

Lagercrantz is interestingly also looking to decentralize the capital allocation aspect of its business, down to the divisional level:

We will still run things in a very decentralized way where the company level is still the most important. So each company by company and working very independently in each of the companies, trying to encourage people and empower people to do good things for us out of the different companies. But we will also build some increased capacity when it comes to different things, so especially M&A on a divisional level. We have been doing that for a couple of years now, but there's a little bit left to be done there. But otherwise, we will get the divisions fully sort of operational to really go and be a strong sort of driver of the divisions' sort of growth and profitability development over time.

– Jörgen Wigh, President & CEO at Lagercrantz Group, Q2 2024.

Wrapping up

At its core, the philosophy of these serial acquirers mirrors the sage advice of Tom Murphy, emphasizing efficiency and the strategic use of resources over expansion for its own sake. This approach is not just about acquiring companies; it’s about nurturing them, leveraging their strengths, and integrating them into a broader ecosystem without stifling their independence or innovation. The REQ study brings to light that the best serial acquirers, from various backgrounds and industries, share common traits: a keen eye for capital allocation, a decentralized structure that empowers local management, and a deep respect for the human element in business.

)

)

)

)

)

)