)

Edge13 Jun 2025

Airbnb: The Hospitality Giant Without Property

Airbnb has grown from an idea to help the Co-Founders make rent, to one of the most dominant companies in the global hospitality industry.

Push a button, get a ride. That vision became the start of what would eventually reshape urban transport, challenge regulators worldwide, and turn Uber into a verb recognized across the globe. Now, Uber's ecosystem moves not just people but also meals, groceries, and goods, coordinating millions of earners and hundreds of millions of consumers – in tens of billions of trips. From rogue disruptor to integrated partner, this is the story of Uber.

For centuries, people have relied on taxi-like services. From horse-drawn carriages rattling over cobblestone streets to yellow cabs jammed bumper-to-bumper in Midtown rush hour. The concept has always been the same: pay someone to take you where you need to go.

The commercialization of the automobile in the early 20th century formalized this practice into the modern taxi industry, a regulated system of licensed operators authorized to pick up passengers on demand. Access to that right, however, was often deliberately limited.

In New York City, medallion licenses (granting the owner the right to operate a taxi) were capped and often traded for hundreds of thousands of dollars. In London, black cabs held exclusivity over the city's taxi market, and joining their ranks required mastering “The Knowledge,” a famously rigorous test requiring aspiring drivers to memorize every street, landmark, and optimal route across the (massive) city, in a process that often takes years.

Across the world, the system was built on scarcity and mastery, not scale. This made full sense in an era when a driver's value was defined by their ability to recall a city's layout from memory. Without that expertise, they simply couldn't do the job.

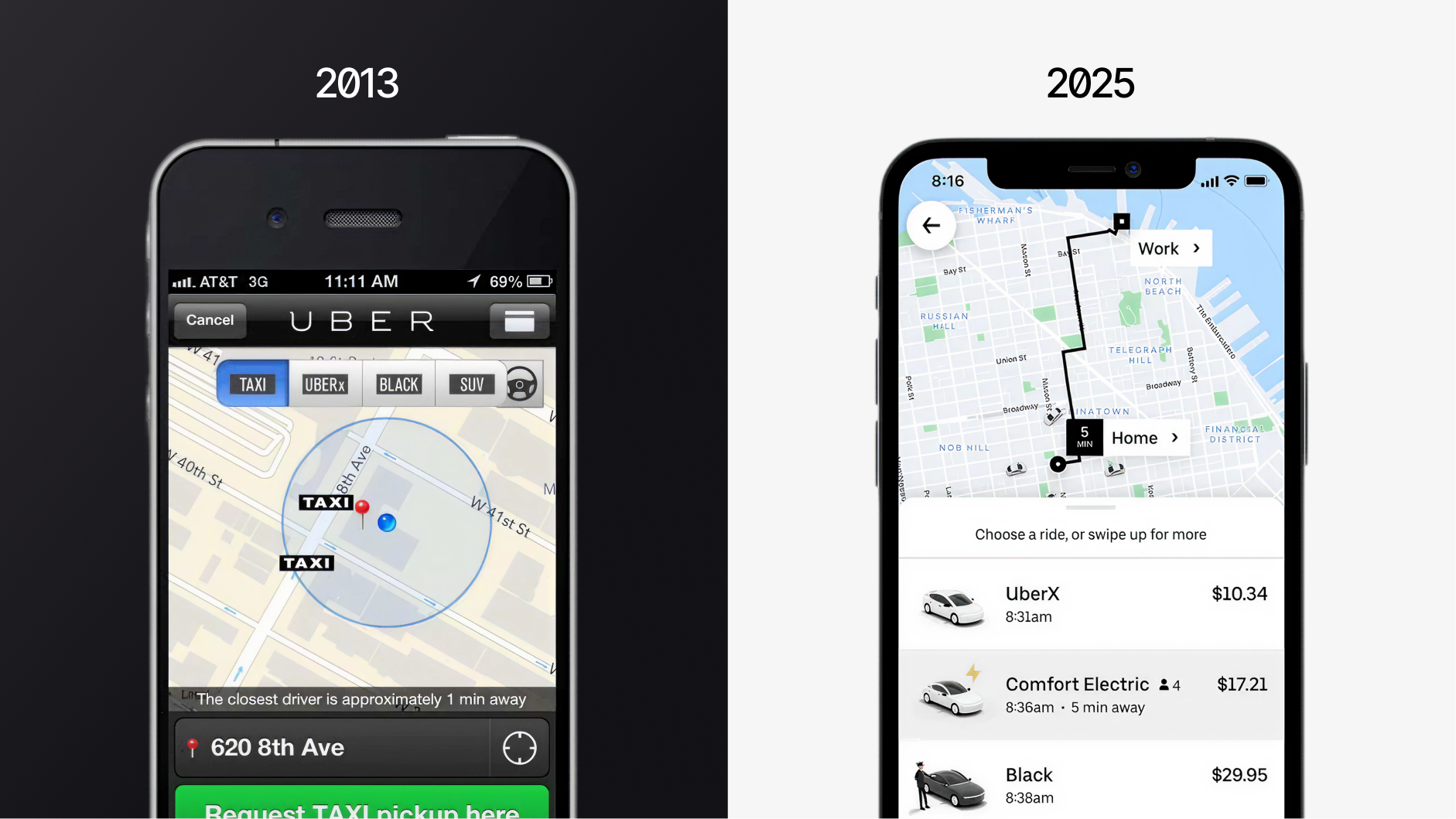

Then technology rewrote the rules. GPS and digital maps, through a single smartphone app, suddenly replaced years of training. The supply of potential drivers no longer had to depend on a finite amount of licenses or memorization; with technology, everyone was a master, and scarcity was no longer inevitable. Some entrepreneurs saw the opening.

Two of those were Garrett Camp and Travis Kalanick, both seasoned entrepreneurs. Camp had co-founded StumbleUpon, later acquired by eBay, while Kalanick had spent more than a decade across startups before using proceeds from an exit to fund new ventures.

In 2009, they launched “UberCab” on a simple premise: ordering a ride should be as easy as tapping a button. A year later, the app went live in the Bay Area with a small fleet of licensed black-car drivers, eager to impress the tech enthusiasts in Silicon Valley. Initially, fares were roughly double standard taxi rates, but as driver supply grew, pricing began to shift from premium to discount.

Almost immediately, the consequences of their “launch first, ask later” approach surfaced. San Francisco authorities issued a cease-and-desist order, arguing that the word “cab” misrepresented the service. It was an early glimpse of what would become Uber's defining theme over the coming years: brilliantly executed disruption on one side, careless defiance on the other.

By 2011, with Kalanick as CEO, the company began scaling beyond California. Backed by fresh venture capital and rebranded as “Uber Technologies”, it rolled out rapidly across U.S. cities, launching in places like New York, Seattle, and Chicago.

From the get-go, non-compliance with taxi regulations was a core part of the Uber playbook. Apart from this disregard, its launching strategy was simple but successful: underprice taxis by heavily subsidizing rides, while also offering lucrative economic incentives for drivers to ensure that users never had to wait long for a ride. By doing so, they boosted both demand and supply to reach meaningful liquidity. And then, they moved on to the next market.

Requirements for commercial licenses and exhaustive inspections were bypassed, but growth hardly slowed. By the end of 2011, Uber was already international, launching in Paris, then Toronto, London, and Mexico City in quick succession. In the years that followed, the company spread across continents, making its presence felt in nearly every major city around the world.

Although market conditions and regulations differed vastly, the blueprint was identical for every market: launch fast, generate rider demand, and onboard drivers quicker than regulators could respond. It was a formula that rapidly gained market share and just as rapidly drew opposition. While consumers loved the service for its convenience and transparent pricing, taxi unions called Uber an existential threat, and city officials continued to accuse it of operating outside the law.

To illustrate the scope of the opposition, regulatory bodies in France, Spain, Italy, Germany, and the Netherlands had all banned Uber from operating by the mid-2010s. But even so, the company continued to operate while opposing the decision. And in the case that an Uber driver was given a fine for using the service, Uber offered to pay it. The company knew its approach pushed past local rules but had fully embraced Zuckerberg's motto to “move fast and break things”, brushing aside every naysayer in its path (Business Insider, 2014).

Although Uber was not shy to operate without a license, it was also constantly lobbying so that the regulatory lights would turn green on the service. Having met resistance across every single city it had expanded to, Uber was prepared to handle all of these different challenges. Time and again, the same cycle repeated: launch, get banned, fight back, then force a compromise through negotiation as consumer demand tipped the scales. In city after city, what often began as prohibition ended in reluctant acceptance.

The reason was obvious: the service was loved. Uber created new earning opportunities while giving riders a faster, cheaper, and more reliable way to move through cities. Even as taxi services and lawmakers cast Uber as a villain, relentless public demand kept it among the most downloaded apps in the world.

Uber wasn't alone in chasing the opportunity. Lyft followed a similar model in the U.S., though with a friendlier brand and more cooperative stance toward regulators. In Asia, China's DiDi and Southeast Asia's Grab scaled quickly by tailoring to local dynamics, while Bolt emerged as a regional contender in Europe. Across all of these markets, subsidies and incentives remained the competitive playbook, a costly race that continued for years (and still does to some extent). To put this into perspective, Uber alone raised $20 billion as a private company to stay on top of it.

Although each regional competitor carved out strongholds, none matched Uber's global ambition. The company's aggressive approach and first-mover advantage made it the most recognized name in ride-hailing, slowly turning it into a verb. No matter which service people use, they say they are “taking an Uber.”

By early 2017, Uber was live in more than 70 countries and 450 cities. Under Kalanick, it had become one of Silicon Valley's most disruptive startups, far past unicorn status, and arguably the decade's most talked-about growth story.

Although revenue was growing at an explosive pace, profitability was nowhere in sight. Uber was burning billions annually, fully committed to expansion at any cost, convinced that taking market share was the only thing that mattered and that in the future its scale would ultimately determine its fate.

While ride-hailing remained its core, the company's ambitions were already extending beyond. In 2014, it had launched UberFRESH, a bet on food delivery that was still in its infancy but hinted at the breadth of what was to come. Uber's momentum truly seemed unstoppable.

Uber's aggressive expansion wouldn't have been possible without Kalanick, but by 2017, his leadership style and the culture it produced were under growing fire. Externally, regulators and rivals had long criticized Uber's reckless push into new markets. But by early 2017, it also became evident that there were issues inside the company as well. These issues came to the surface after a whistleblower stepped forward.

Among the accusations were systemic sexual harassment, ignored complaints, and a toxic culture that protected high-performing offenders. For a company already known for its rule-breaking, learning that the same traits defined its internal culture was a devastating blow. Public focus increasingly turned to Kalanick himself, portrayed as the embodiment of Uber's disruptive ethos.

At the same time, a New York Times investigation exposed a secret program called Greyball. The story revealed that Uber had, since 2014, been using a program designed to identify regulators and law enforcement officials in cities where the service was restricted and then deliberately show them a fake version of the app to evade detection. This, of course, elevated the criticism of Uber to new heights and raised serious ethical and legal questions about its operations.

And as if that weren't enough, in February 2017, Alphabet's Waymo sued Uber for allegedly stealing autonomous vehicle trade secrets.

Obviously, it was a full-blown PR crisis for the company. Accusations of sexism, disregard for regulation, and winner-take-all aggressiveness had become central to the company's public image. It was clear, unless something changed quickly, moving fast might break Uber itself.

That spring and early summer at Uber's headquarters were incredibly intense. After the wave of scandals and the release of a detailed internal report prompted by the whistleblower account, a group of major investors collectively demanded Kalanick's resignation.

In June of 2017, he stepped down as CEO of Uber, setting off months of turmoil over his remaining influence.

The departure was anything but orderly. His resignation followed weeks of boardroom conflict, with Benchmark Capital (one of Uber's largest and earliest shareholders) and other backers staging a coup to force him out. Kalanick, still on the board, even attempted to fill vacant seats unilaterally on his way out, sparking lawsuits and months of internal power struggles. That struggle only ended later in 2017, when SoftBank's $9 billion investment expanded the board and curtailed Kalanick's control, marking the true end of his reign at Uber.

While this was unfolding, Uber's board searched for a successor. After weighing several high-profile candidates, they landed on what many saw as a surprise choice: Dara Khosrowshahi. As CEO of Expedia, he had spent over a decade scaling the company into one of the world's leading online travel platforms, earning a reputation as a thoughtful operator capable of managing complex global businesses. In other words: exactly what Uber needed.

Still, Dara had no plans to leave Expedia and turned down an approach from a headhunter – one who had been sent his way by Daniel Ek. The Spotify founder had credibility on the matter: his own company had evolved from an outlaw fighting record labels to a well-established partner of the music industry. If anyone understood how a messy disruptor could become an indispensable institution, it was him.

Soon thereafter, during a night out, Ek confronted and persuaded Dara to reconsider the offer, as later recalled in a 2023 interview with the Uber CEO on Acquired:

“He looks at me with those piercing Scandinavian eyes. He's like, 'Dara, since when is life about having fun? It's about having impact. This is important. You can do this.'”

That push convinced Dara to leave Expedia and rebuild Uber.

Dara's arrival was the first step needed to set Uber on a new course. The company was still defined by the old culture, and while leadership could change overnight, reshaping values would take time.

After a few months on the job, Dara publicly announced that Uber's old “Values” (created by Kalanick and included classics such as “Super pumped” and “Always be hustlin'”) had been replaced by eight “Cultural Norms”, developed together with employees all across the organization. While some of the previous remained, they were rephrased and polished to be more inclusive and a bit less testosterone-fueled.

In his announcement, Dara praised the company's accomplishments but insisted that a different approach was needed for the future:

“It's that forward-leaning, fearless approach that has underpinned much of Uber's success and has attracted many employees, including me, to the company. But it's also clear that the culture and approach that got Uber where it is today is not what will get us to the next level. As we move from an era of growth at all costs to one of responsible growth, our culture needs to evolve.” (LinkedIn, 2017)

Of the new principles, one stood out as a direct signal to regulators, employees, and the public alike:

We do the right thing. Period.— Dara Khosrowshahi, CEO of Uber.

It was a deliberate page-turn from years of defiance and non-compliance. In the years that followed, diplomacy became the focus. Where Uber had once fought cities, it now sought to work with them, sharing data with transit authorities, piloting local partnerships, and adjusting services to fit local norms. At the same time, Dara drove governance and operational changes inside the company, bringing in experienced leaders to the management team. Together, these moves gradually shifted Uber's image from rogue disruptor to partner.

Before we continue, a quick detour on Uber's regulatory approach. It should be emphasized, the company has never enjoyed the luxury of launching with an automatic, everlasting license to operate across any of its markets. But with Dara, the intent to comply changed fundamentally. When the company has faced denials of license or negative publicity in recent years, its response has been cooperative rather than combative. Uber now clearly does the right thing.

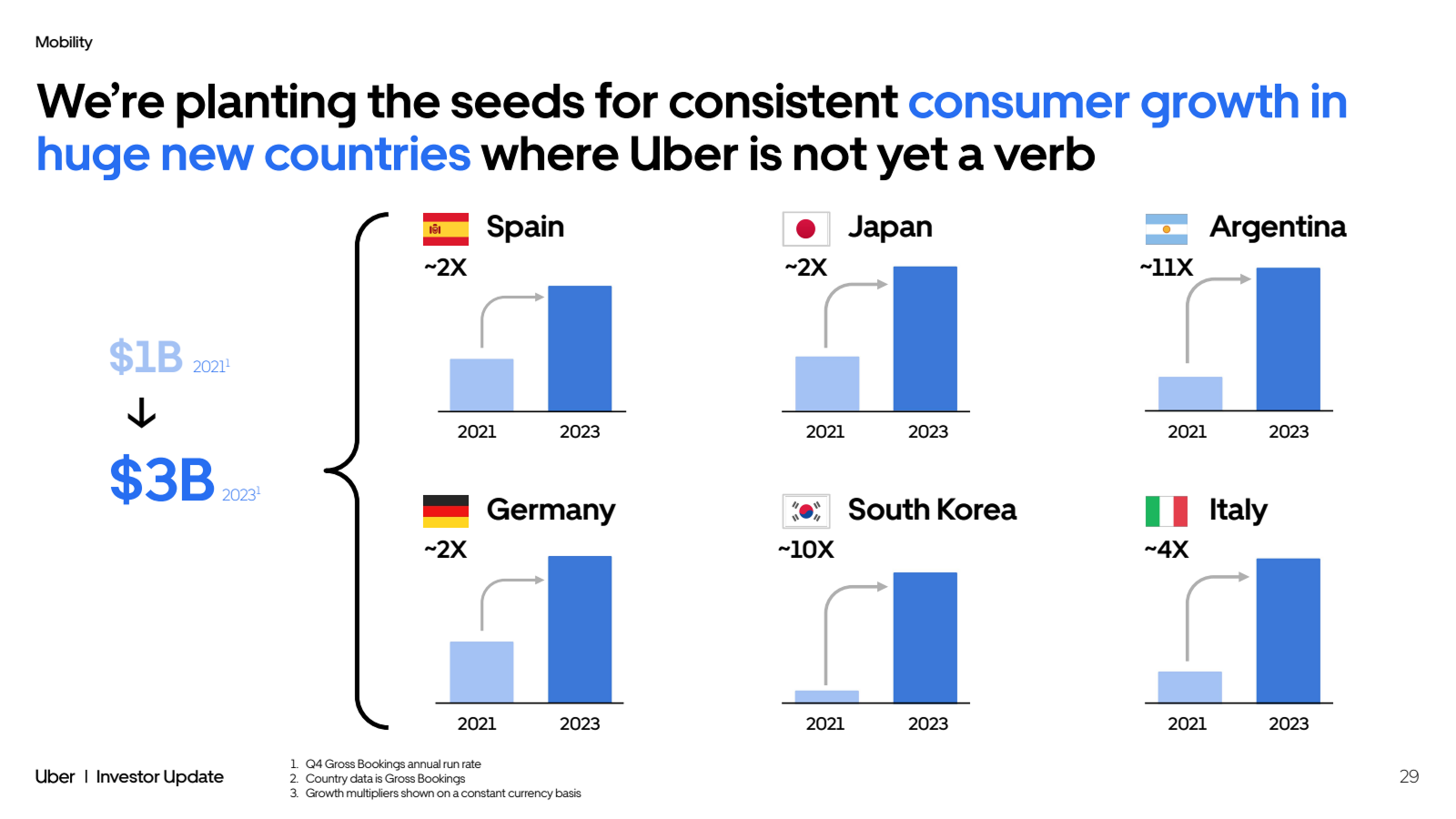

Today, Uber operates in more than 15,000 cities across over 70 countries. Entering new geographies means navigating complex licensing regimes, lengthy permit approvals, and, in some cases, modifying the core business model itself. As of today, in several markets such as Argentina, Germany, Italy, Japan, South Korea, and Spain, Uber's ridesharing business is blocked, capped, or required to adapt to stringent restrictions. Long story short: regulations continue to shape how Uber can operate.

Nowhere is this clearer than in New York City, one of Uber's most important yet most heavily regulated markets. Ever since Uber first launched there in 2011, it has faced constant tension with regulators and the entrenched taxi industry. Under Dara's watch, the city introduced sweeping new rules in 2018. These included minimum per-mile and per-minute pay standards for drivers and a freeze on new vehicle licenses. The measures have constrained Uber's driver supply and raised its operating costs, forcing the company to adapt in the key city.

Initially, Uber fought bitterly against these rules. But in recent years, it has shifted toward collaboration. In 2023, a $328 million settlement with the New York Attorney General established a minimum earnings guarantee and other worker protections while still allowing drivers to use multiple apps. That same year, Uber integrated New York's iconic yellow cabs into its platform, completing a striking transformation from open warfare with taxis to building them into the ecosystem.

The New York experience captures Uber's regulatory reality today. Market access remains dynamic and complex, but the company's willingness to engage, compromise, and adapt has allowed it to keep operating in critical cities where, a decade earlier, its survival would have been doubtful. Regulation has gone from an existential threat to a daily cost of doing business, and Uber's ability to manage it is now a competitive necessity rather than a question of defiance.

Back to Dara's transformation of Uber. With new personnel in place, the company proactively reshaped its foundations. Stronger HR policies, the settlement of legal disputes, and a renewed emphasis on rider safety all signaled that Uber was, in fact, changing.

In terms of its operations, Uber began changing its approach in markets where it had previously “burned cash” in an effort to win at all costs. Rather than continuing costly battles, it exited certain regions, partnered in others, and merged with competitors where appropriate. The guiding principle was clear: Uber would stay only in markets where it could become the leader or had a credible path to get there, while taking equity stakes to remain exposed in many of those it left.

At the same time, leadership started reassessing the sprawling side ventures launched under Kalanick, from self-driving cars and flying taxis to bike and scooter sharing, most of which had consumed billions of dollars without clear payoff. Under Dara's watch, many of these were scaled back, spun off, or sold. Together, these moves reflected a shift toward discipline and resource optimization.

There was one exception: Uber Eats. Rather than winding it down, Dara gave the food-delivery arm more attention and investment. Within a few years, it would prove to be one of Uber's most valuable growth engines. We'll return to that story shortly.

By 2019, Uber was slowly but steadily beginning to live up to Dara's promise that it had to evolve. Regulatory battles were giving way to diplomacy, and while profitability still seemed distant, the company appeared far more disciplined and future-focused. So when Uber went public with a market cap around $70 billion in May that year, the headline-grabbing chaos of its earlier years already felt a world away.

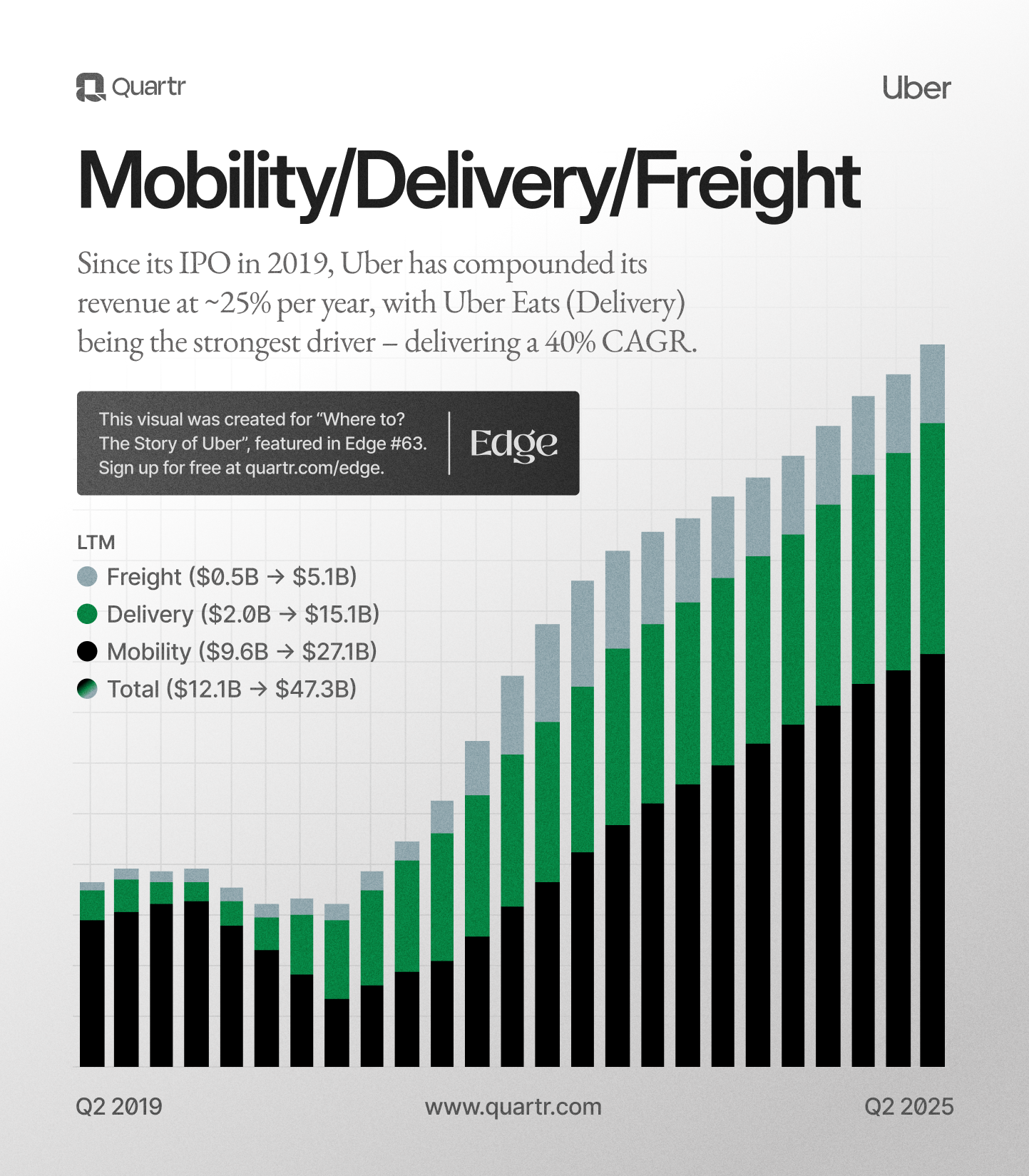

Uber of 2025 is a global platform that orchestrates supply and demand across multiple marketplaces. At its core, it connects drivers with riders, restaurants with consumers, and shippers with carriers. Its two largest businesses, Mobility and Delivery, account for nearly all revenue.

Uber Freight contributes roughly 10% of revenue. It mirrors the marketplace model of its core segments but has yet to make an impact on the bottom line. For now, management gives it limited attention. Still, as we'll see later, businesses that once looked marginal have grown into core pillars before.

The company's scale is enormous. Uber operates in more than 15,000 cities, facilitating tens of billions of trips each year for hundreds of millions of consumers and roughly 9 million earners. By some measures, that makes Uber the largest private workforce coordinator in the world. Other gig-economy players, such as DoorDash, Instacart, or Airbnb, run similar models, but none operate with Uber's breadth.

Total gross bookings, a key measure of Uber's ecosystem scale and growth, have risen at a CAGR of over 23% from mid-2020 to mid-2025. Today, Mobility and Delivery contribute in roughly equal measure to that overall volume (with Freight making up only a small share). Additionally, platform engagement across its ecosystem has steadily improved: monthly trips per active consumer have risen from around five trips in 2020 to more than six trips in Q2 2025.

That increase may seem modest, but across 180 million active users, it represents hundreds of millions of additional trips each month and is a sign of improving stickiness. Taken together, these growth trends point to the compounding use of Uber's services and its ability to meet demand reliably at a global scale.

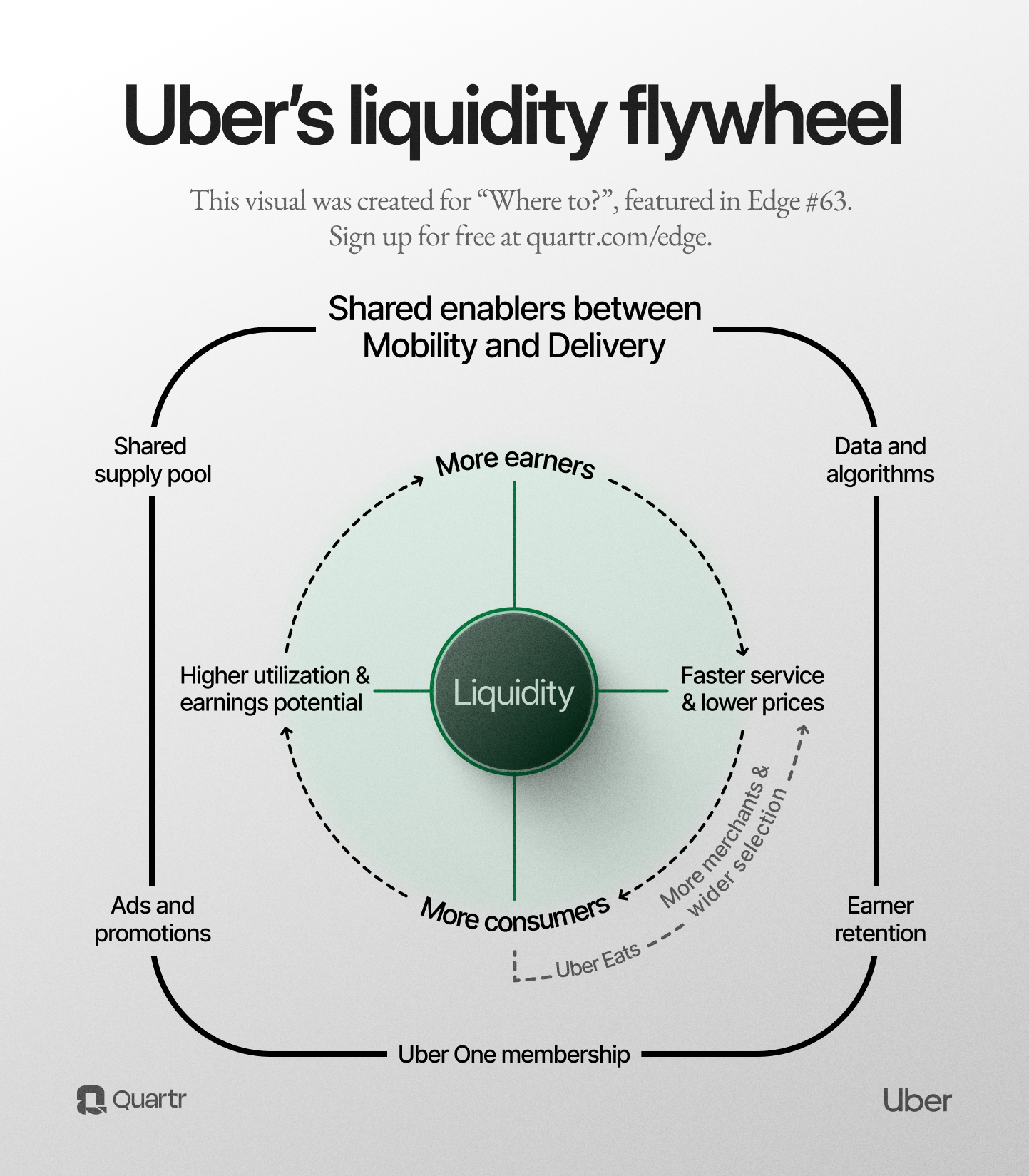

One of Uber's greatest strengths is the self-reinforcing flywheel built into its platform, and how that dynamic is replicated to create local network effects in city after city. More riders attract more drivers; more drivers shorten wait times and expand coverage; better service attracts more riders. But what truly sets Uber apart is the shared infrastructure beneath the surface. Every trip feeds into a massive dataset that strengthens its system, as Dara Khosrowshahi puts it:

“While it may not always be visible to the casual user or investor, this really is our secret sauce. Whether you're ordering a ride or a delivery much of the underlying tech and tech-enabled operations, identity, maps, payments, fraud detection, ordering, dispatching, pricing and more, they're all shared across Uber.”

– Uber's Investor Update 2024 (sourced through Quartr Pro).

The result is the core of Uber's network: a real-time matching system with liquidity at its heart. This is what creates the reliability riders expect and the steady volume drivers depend on. With each additional ride or delivery, the system becomes smarter and more resilient, compounding the flywheel and widening an algorithmic moat that competitors struggle to replicate.

Mobility has always been Uber's core. The segment has grown into the world's largest ride-hailing platform, connecting billions of riders with drivers each year across the globe. While the company has since expanded into delivery, freight, and advertising, ride-hailing remains the foundation of its marketplace business.

Mobility's gross bookings have increased by a CAGR of over 17% from mid-2020 to mid-2025. Although this is lower than the company total (lifted by Delivery's CAGR of 33%), Mobility has shown strong acceleration recently, growing more than 18% versus the prior twelve months in Q2 2025.

Under the surface, Uber's model is straightforward: riders book trips through the app, drivers provide the rides, and Uber takes a percentage of each fare. That cut, the take rate, has hovered near 30% in recent years, though it varies by region, maturity, and product mix. Management has emphasized maintaining the take-rate at a disciplined, long-term, sustainable level for two reasons.

First, keeping the take-rate “as low as possible” builds loyalty among riders and drivers, making it harder for competitors to lure either side of the marketplace. Second, it forces internal efficiency, continually pushing Uber to cut costs and run the network more effectively. This approach echoes the principle of “scale economics shared,” popularized by investor Nick Sleep in his analysis of Costco: passing efficiency gains to users builds long-term defensibility.

Competition in ride-hailing remains intense but is fragmented, largely due to the nature of network effects. Unlike many other marketplace models where scale compounds globally, in ride-hailing (and delivery), liquidity forms locally. In the U.S., Lyft remains Uber's main rival while Bolt holds a strong position in many European markets.

In several markets across Latin America and East Asia, regional leaders such as DiDi and Grab dominate, both of which are now minority-owned by Uber. Guided by the more strategic and disciplined expansion strategy set out a few years ago, Uber today leads in most of its markets, including all of its ten largest by revenue.

Expansion remains a key growth driver. Uber plans to launch in “hundreds of new cities” in 2025, typically starting in dense urban centers before expanding to smaller markets. As noted, although much of Uber's “secret sauce” (shared infrastructure, data, and algorithms) can be replicated across markets, liquidity is intensely local. A well-functioning network in one city doesn't automatically translate into scale in the next. Each market requires its own critical mass of riders and drivers before network effects begin to compound.

The entry phase includes an investment period as the service launches. To seed both sides of the marketplace and reach sufficient liquidity, Uber often subsidizes drivers and riders heavily, at times paying out incentives that can equal or exceed the gross bookings generated on early trips. Other expansion costs include everything from adapting the app and payment methods to recruiting local staff and navigating compliance with country-specific regulations. These efforts weigh on margins in the short term but converge toward the broader company profile as penetration improves.

The opportunity for Uber to improve penetration in its already mature markets remains significant. Ride-hailing still accounts for only a small share of total miles traveled in most regions, and adoption continues to climb. In fact, the vast majority of Uber's top 20 cities are still growing at double-digit rates, highlighting how much headroom remains even in established markets. The potential impact can be substantial, as explained by Dara at its Q2 2024 earnings call:

“... if the United States was to move to the TAM penetration that we're seeing in the U.K., that's worth another $13 billion in gross bookings. So call it 8% to 8%-or-so of our current run rate just by moving the U.S. to the U.K. So we know the opportunity is there.”

Taken together, Uber not only pioneered ride-hailing with its Mobility business but has maintained its leadership role ever since. Over time, autonomous vehicles could reshape this segment in significant ways, a topic we'll return to later. But before that, we need to rewind to the pandemic years, when Uber Eats went from contributing about 20% of revenue to redefining the company's trajectory.

Uber's food delivery business began in 2014 as UberFRESH, initially a limited service offering curated lunch dishes from select restaurants. In 2015, it rebranded as Uber Eats and adopted the same city-by-city expansion strategy that was fueling its ride-hailing segment. Over time, Eats broadened from a premium, niche offering into a mass-market platform where consumers could order nearly anything from local restaurants.

By 2019, in its first year as a public company, Eats was showing strong growth, then contributing to 20% of total revenue. That quickly changed with the pandemic, with the global shutdown creating opposite pressures on Uber's two marketplaces. Mobility demand collapsed as people stayed home, while Delivery volumes spiked as consumers turned to apps for take-out meals.

As Uber closed 2020, Delivery had climbed to 35% of total revenue, and in 2021, it had grown to nearly 50%. Today, it continues to grow, though its share has normalized somewhat. Since its IPO in 2019, the Delivery segment's revenue has posted a CAGR at an impressive 40%.

For Uber, the rise of Eats completely reshaped the company. While it initially served as the perfect lifeline during the pandemic, Eats has become a cash-generating segment that has helped transform the company on its road to profitability. Equally important, operating two scaled marketplaces with overlapping customers, earners, and infrastructure has unlocked cross-platform synergies that have lifted both segments to new heights. We'll return to these synergies shortly.

At its core, the model mirrors Mobility with one additional stakeholder: customers order through the app, couriers fulfill the deliveries, and Uber takes a cut of each transaction. The scope has also broadened well beyond what the name reflects. Uber Eats now encompasses groceries, alcohol, pharmacy goods, and other everyday essentials, increasingly evolving into a broader on-demand everything-logistics network rather than just a food delivery app.

The take-rate here has averaged a little under 20% in recent years, somewhat lower than Mobility. Largely, this is because Delivery involves a more complex network of stakeholders, including restaurants, merchants, and couriers, compared to the simpler driver-rider dynamic in Mobility.

Like ride-hailing, Eats was initially built on heavy subsidies to capture share, but the economics have steadily improved. Greater courier utilization, order batching, and pricing rationalization have all contributed to Eats becoming a profitable addition to Uber.

Competition for delivery, however, remains intense. As with ride-hailing, delivery network effects are local, resulting in a fragmented race across regions. In the U.S., DoorDash is the leading player, with a larger share than Uber. DoorDash is also expanding internationally, having launched in over 30 countries through its acquisition of Wolt. Additionally, it is in the process of acquiring British Deliveroo, pending regulatory approval. And while these expansive efforts remain a limited portion compared to Uber's global scope and penetration, it will be interesting to follow going forward.

In Europe, competition is both fragmented and fierce, with regional players each holding a strong share in different markets. Rivals like just mentioned Deliveroo, but also Just Eat Takeaway, Delivery Hero, and others, all compete with Uber across Europe's delivery scene. The same goes for Latin America and Asia, where strong regional players often dominate. Even so, where Uber Eats maintains a presence, it has secured leading positions in most of its largest markets.

The opportunity remains vast. Food delivery penetration continues to rise globally, with adjacent categories expanding the addressable market even further. Dara expanded on this at Uber's Q2 2024 earnings call:

“So what we're seeing in terms of delivery is the long-term growth is incredibly promising and especially our ability to expand into the adjacent category of grocer and retail. The grocer and retail TAM is actually bigger than the online food delivery TAM, so not only do we believe we've got a long runway in online food delivery, but we're just getting started as it relates to grocer and retail.”

What sets Uber apart from most competitors is the duality of its marketplace. Few companies can take you home from work, deliver your groceries, and bring you dinner all within the same ecosystem. This breadth creates a unique opportunity to fuel both marketplaces while deepening relationships with consumers and earners alike. Crucially, while liquidity builds city by city, the infrastructure and technology behind these marketplaces is replicable and global, powering Mobility and Delivery through the same underlying systems.

Uber currently operates through two apps, Uber and Uber Eats. The apps are partially integrated: users of the Mobility app can access Delivery, making it a gateway into the broader ecosystem. The company continues to debate whether to consolidate them into a single “super app,” but even in their current form, the overlap is meaningful. During Q2 2025, 12% of Delivery's gross bookings were generated through the Mobility app, and in Q1 2025, 30% of Delivery's first trips originated there.

The company's strategy centers on building multiproduct consumers, compounding value through loyalty. As Dara Khosrowshahi explained on the Q2 2025 earnings call:

“So we have to make sure that we are cross-promoting one service to the other mobility to our each business or each business to grocery, grocery user to retail in a way that is targeted and in a way that is adding value for the consumer. And the only way to get there is through super, super aggressive experimentation. The great news is that the -- those who kind of use both sides, both Mobility and Delivery, their retention rates are higher, they are 35% higher than single business consumers. They generate 3x the gross bookings and profits in single business consumers as well.”

Another lever is Uber One, the membership program launched in 2021. For about $50 per year, members gain incentives that encourage them to stay inside the Uber ecosystem rather than switching to a single-segment rival app. Uber One bundles benefits across rides and delivery, including $0 delivery fees, discounts on eligible orders, credits on rides, and exclusive deals.

The program has scaled quickly since its launch. As of Q2 2025, Uber One counts 36 million members, growing approximately 60% year-over-year. Uber One members accounts for over 40% of combined Mobility and Delivery gross bookings.

Synergies extend beyond consumers, as having two marketplaces lowers the cost of attracting and retaining earners. Uber estimates that moving couriers into ride-hailing, or vice versa, costs less than half as much as recruiting new earners through traditional channels. Drivers who cross-platform, splitting time between Mobility and Delivery, show higher retention and utilization than those tied to a single service. This matters for attracting supply, as predictable access to trips creates greater overall earning opportunities.

That dynamic is especially important in a gig economy defined by multi-homing, where earners often 'dual app,' toggling between Uber, Lyft, DoorDash, and others to maximize income. Since exclusivity is neither enforceable nor desirable, Uber instead focuses on being the preferred choice. By offering both ride-hailing and delivery under one roof, it reduces the likelihood of losing earners to rivals.

If you've followed Uber, listened to Elon Musk pitch Tesla's robotaxi ambitions, or tracked Waymo's cautious expansion in recent years, you haven't missed the intensifying debate around autonomous vehicles (AVs). Few topics in transportation have attracted as much attention, or as many conflicting views about timing, business models, and long-term impact.

Uber has been part of that debate from the start. Under Travis Kalanick, the company poured billions into building its own self-driving unit, determined to control the full stack. But progress was slow, losses piled up, and the approach proved unsustainable. When Dara Khosrowshahi took over, he reset the strategy by selling off its self-driving division in 2020, refocusing on what Uber does best. Not building AVs itself, but positioning as the distribution network, ready to partner with whichever providers emerge.

As of September 2025, Uber has 20 autonomous partners across Mobility, Delivery, and Freight. These range from pure AV specialists like Waymo, Nuro, Avride (owned by Nebius Group), and Baidu to established automakers such as Volkswagen and Volvo. The nature of these agreements varies widely by partner, ranging from equity investments and vehicle commitments to direct fleet integrations and distribution deals with established OEMs.

In some cases, such as the Lucid deal in July 2025, the arrangement was a strategic equity investment paired with a commitment to bring thousands of Lucid's upcoming autonomous-ready SUVs onto Uber's network, with vehicles expected to be deployed through fleet partners rather than owned outright by Uber.

According to Dara, many capital providers are yet to see the economics of the marketplace, and while we are getting closer to this, Uber can play an important role. In the Q2 2025 earnings call, he reflected on Uber's willingness to prove this and be a catalytic force:

“So once we prove out the revenue model, how much these cars can generate on a per day basis, there will be plenty of financing to go around, third-party financing. We've talked to private equity players. We've talked to banks, et cetera. And while it will take some time, we're very confident that these assets are going to be financeable. And for us, we believe it's a competitive advantage for us to be able to use a relatively modest part of our cash flow to fund kind of the catalyst to get things started here.”

With Waymo, the integration is structured as a platform partnership where its autonomous vehicles are made available through the Uber app in Austin and Atlanta, while also being available through Waymo's own app. In San Francisco, Waymo operates exclusively through its own app, while in Miami, it is expected to work with Moove (where Uber holds a minority stake) but keep the Waymo brand. Like Uber, Alphabet is experimenting cautiously across markets. As CEO, Sundar Pichai explained in its Q1 2025 earnings call:

“... I think we've been laser focused and will continue to be on building the world's best driver. And I think doing that well really gives you a variety of optionality in business models across geographies, et cetera. It'll also require a successful ecosystem of partners, and we can't possibly do it all ourselves. [...] we are widely exploring [the different alternatives]...”

In April 2025, Uber announced a partnership with Volkswagen. This deal was structured as a long-term OEM integration, with Volkswagen's forthcoming ID. Buzz autonomous fleet to be made available on Uber's platform once commercial deployment begins later in the decade. At the company's Q2 2025 earnings call, Dara hinted that more agreements of this magnitude are likely:

“We are talking to all of the major OEMs in the space, and we're confident that over the next couple of years, we will have OEM partners.”

Though Mobility understandably draws the most attention, Uber's autonomy efforts also extend to Delivery and Freight. In Delivery, partnerships typically take the form of smaller projects focused on last-mile robotics, while in Freight, they center on collaborations with trucking specialists still refining their technology. Across all three segments, the structure of each deal reflects both partner maturity and Uber's own priorities.

Together, these examples highlight how widely Uber's partnerships can vary depending on the partner's size, maturity, and focus. As the largest global mobility marketplace, it is positioned as the natural distribution partner for AV companies, offering access to demand, pricing functions, routing, and a consumer base already comfortable with Uber.

“You'll see a [ panoply ] of models, but we are confident that based on our platform, based on our ability to balance kind of supply and demand, peaks and valleys, we think we'll be the leading third-party platform out there. And with a market that is going to grow and expand the way AV promises to, I think, we’ll be a winner, but we won't be the only winner.”

– Dara Khosrowshahi, at Uber's Q2 2025 earnings call.

For now, the U.S. is the launchpad for autonomous vehicle development and deployment. It combines deep pools of venture and corporate capital with relatively permissive state-level regulation, and a handful of dense urban markets where both demand and technical complexity can be proven. The rest of the world is watching closely, with the expectation that approaches validated in the U.S. will ultimately be applied on a global scale.

Although AVs are live in a few cities and more launches are planned, mass commercialization is still a long way off. In the Q4 2024 earnings call, Dara touched on this and what it will take for the AV revolution to reach scale:

“…we think that the commercialization of the technology is going to take way, way longer. And by the time that the technology commercializes all over the world and in the U.S., you're going to see many, many more players get over the finish line as it relates to technology. And just stepping back for a second and this applies for the U.S. and applies all over the world. There are 5 factors that you need, all of which need to come together for scale commercialization of this business…”

Those five factors are:

Regulations: National, state, and local.

Consistently superhuman safety records: The AV has to be “multiple times better than the human”.

Cost-effective hardware platform: The cost of hardware platforms must come down from the hundreds to the tens of thousands of dollars.

First-rate on-the-ground operations: Infrastructure and fleet management, such as recharging, cleaning, and lost item handling.

High utilization network: Capable of managing the variable demand and flexible supply.

The fifth factor is where Uber enters the picture, as concluded by Dara:

“You need all 5 to come together. And we think the only way that all 5 can come together is Uber partnered up with the AV ecosystem.”

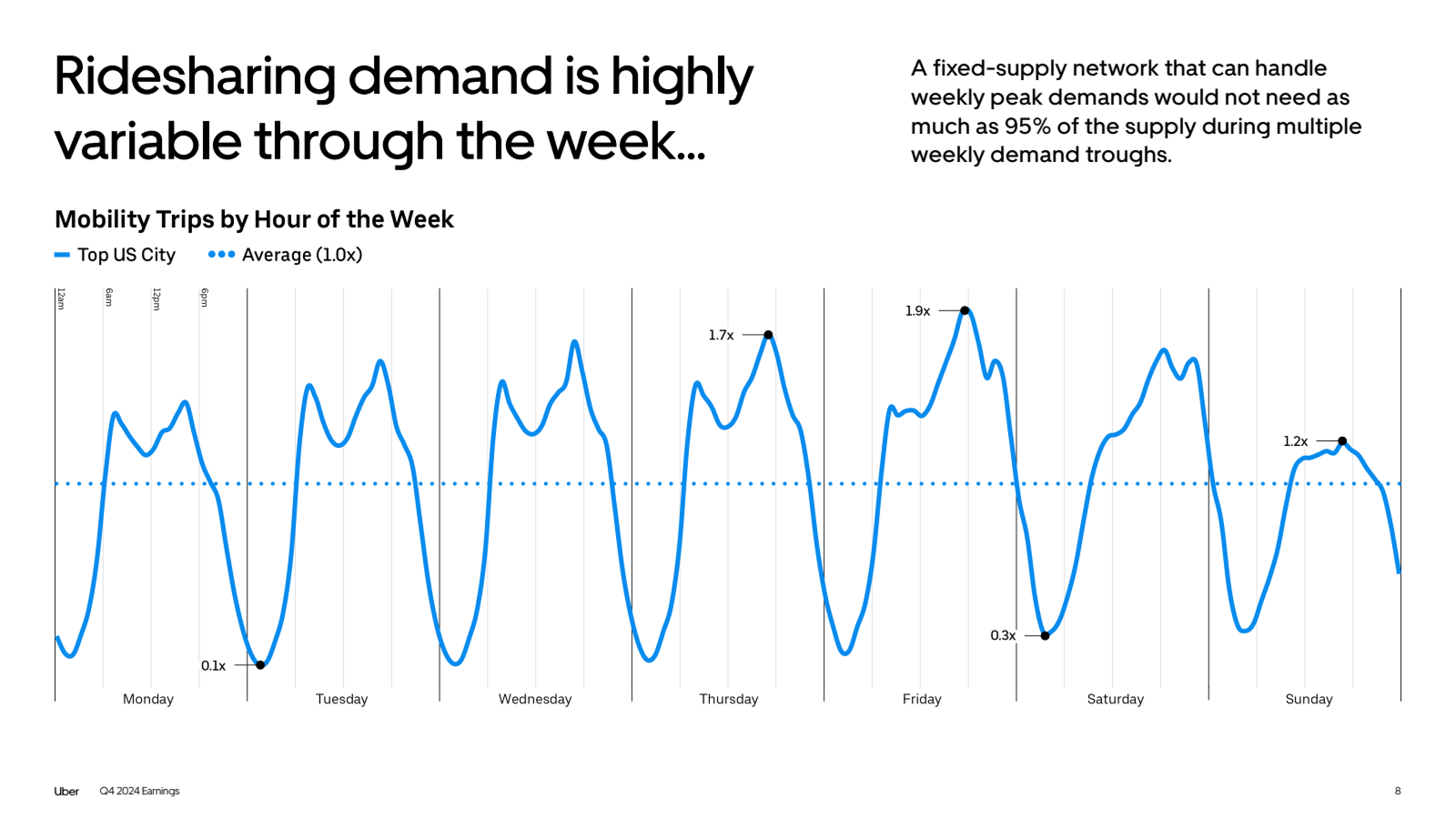

Uber's unmatched global scale and real-time matching algorithms give it a unique ability to balance the swings of real-world demand. In a major U.S. city, trip volumes can fluctuate from 0.1x to 1.9x within a single week, with further variation across cities and seasons. If AV fleets were built to cover peak demand alone, most vehicles would sit idle during off-hours, which would be financially unsustainable for operators.

Uber's hybrid model solves that problem: autonomous vehicles can cover the steady baseline, while human drivers absorb the peaks.

But the crucial point is that Uber already runs this system successfully at scale. Its platform coordinates billions of trips each year, fueled by data, algorithms, and infrastructure that no AV company could replicate quickly or cost-effectively, especially while also building vehicles and chasing market share. The company presents this as the foundation for its strategy to serve as the distribution layer. First in the U.S., and then worldwide.

“Now I think that you're going to see lots of experimentation and AV players going direct, working with us, et cetera. But especially, we're looking forward to our launches in Austin, Atlanta, where I think we're going to demonstrate pretty clearly that a combination of a great AV provider like Waymo and Uber is the best combination out there. And I think this is going to apply in the U.S., it's going to apply all over the world.”

– Dara Khosrowshahi, CEO of Uber, at its Q4 2024 earnings call.

That autonomous vehicles are coming is not in doubt. The real debate is whether the future belongs to many players – or just one.

For companies like Alphabet (through Waymo) or Volkswagen, the prevailing belief is that experienced marketplaces will play an important role in bringing AVs to market. However, one player stands apart with a starkly different stance: Tesla. Known as one of the great disruptors of our time, Tesla has advanced a vision bold enough to challenge the prevailing consensus. On its Q1 2025 earnings call, Elon Musk stated:

“ … I don't see anyone being able to compete with Tesla at present. I'm sure that will change eventually. But at least as far as I'm aware, Tesla will have, I don't know, 99% market share or something ridiculous.”

So far, Tesla has shown no inclination to rely on third-party marketplace networks. Instead, its strategy is to activate the millions of vehicles it has already sold, turning them into an on-demand fleet once autonomy reaches scale. The company is already running pilot programs of its robotaxi service, though these remain in very early testing phases. Its plan is that when Tesla owners eventually send out their cars to earn income, they will do so exclusively on a Tesla-operated platform:

“But this will all be a Tesla network. And there's an important clause we've put in every Tesla purchase, which is that the Tesla vehicles can only be used in the Tesla fleet. They cannot be used by a third party for autonomy.”

– Elon Musk, at Tesla's Q2 2024 earnings call.

This position marks a sharp divide from most other players and has fueled debate across the industry. Many companies, echoing Dara Khosrowshahi's view, argue the market is vast and inherently fragmented: “And again, we said it before, this is a very, very big market. There will be no winner take all.” Musk's projection, however, implies a very different outcome, one in which Tesla dominates the entire space. That vision has raised the stakes and turned the rollout into what some describe as an AV race.

Uber, for its part, sees itself as central in that race. As Dara explained in its Q1 2024 earnings call:

“And if you're an AV fleet owner or you are an individual owner of a car, whether that's a Tesla or another kind of car, you're just going to make more money and make a higher kind of return on your investment if you plug in your AVs into the Uber ecosystem and into Uber demand. So we think we bring lots to the table. We're looking to partner with the AV industry.”

Looking at this through the lens of valuations, it is clear that the market also sees the stakes. As Volkswagen CEO Oliver Blume half-jokingly pointed out in its Q2 2025 earnings call:

“We have the first external customer with Uber starting in '26 in Los Angeles. And so we are ready to compete. And you know around 50% of the market cap of Tesla is counting on this. And so I think there's still also a potential for Volkswagen Group and the market cap for Volkswagen.”

The stakes are big, to say the least. Tesla's robotaxi vision is ambitious, though whether Musk can deliver remains to be seen. His timelines have often slipped, but he is still Elon Musk, and when he speaks, people listen. That contrast was exactly what Pershing Square Capital Management CEO Bill Ackman laid out in his investment thesis for Uber, posted in Pershing Square Holdings (the publicly traded closed-end fund managed by Pershing Square Capital Management) annual report of 2024:

“We believe Uber's current valuation represents a significant discount to intrinsic value because some investors are myopically focused on the risk of AVs, without proper consideration for Uber's strong value proposition and the potential for AVs to benefit the ecosystem.”

The point here is not to make an investment case in either direction, but to highlight the starkly contrasting visions. Some see AVs as a disruptive threat to Uber, others as a major opportunity. Full commercialization may still be years away, but the race will be fascinating to follow, and its outcome will carry significant consequences for mobility markets worldwide.

Under Dara Khosrowshahi, Uber has become a disciplined and profitable company, while still delivering strong growth.

Uber's roughly $47 billion in trailing twelve-month revenue remains anchored in Mobility, which represents about 57% of the total and has compounded at nearly 19% annually since the 2019 IPO. Delivery contributes roughly a third of revenue, growing at a steadier pace after its pandemic surge, while Freight accounts for just over 10%. A smaller stream comes from its high-margin advertising business, which sells sponsored placements within its apps to restaurants and brands and is reported within Delivery. This fast-growing side of its business surpassed $1 billion in 2024.

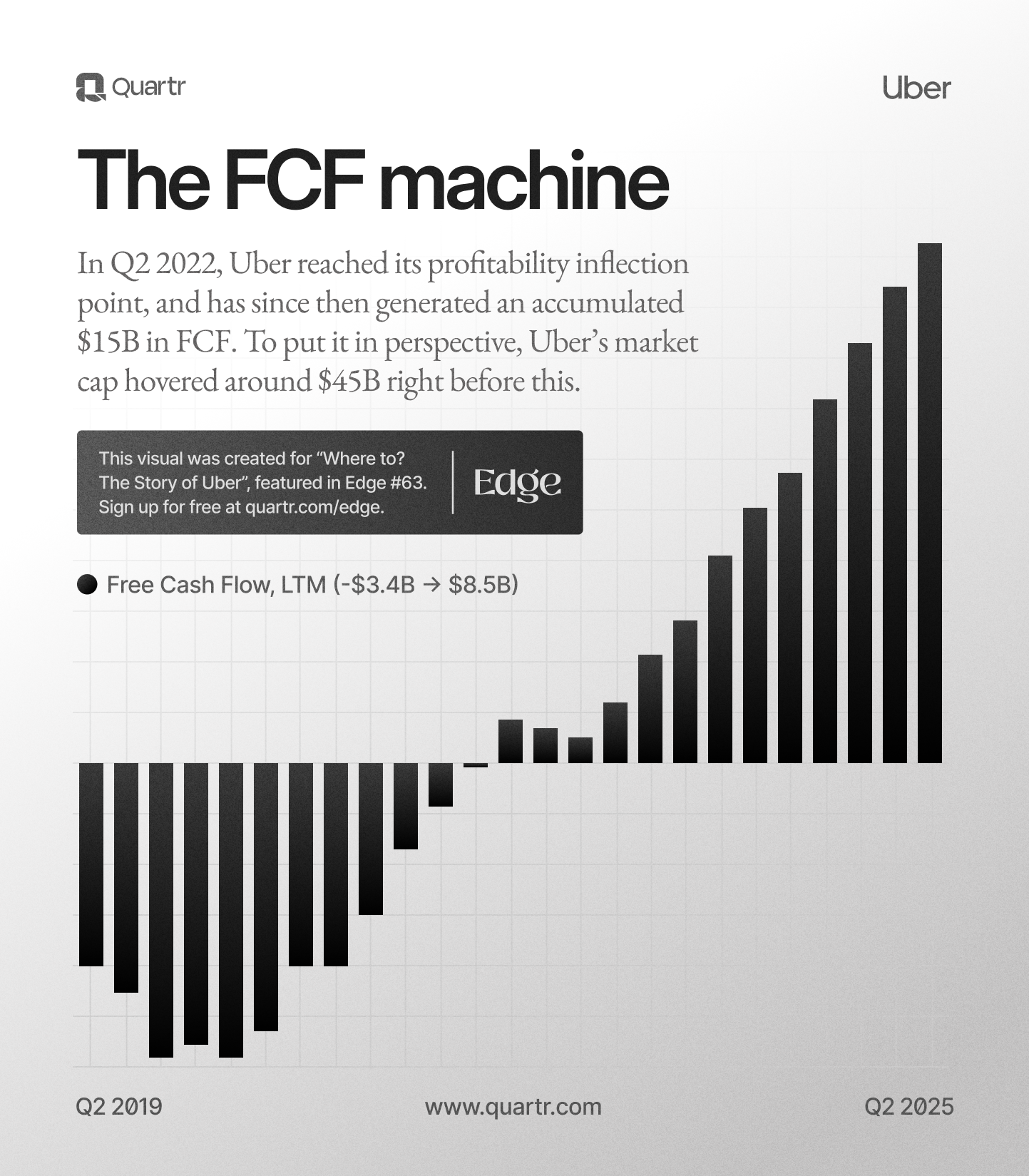

The company has shifted from “growth at any cost” to disciplined expansion, with operating leverage now a defining feature of its model. Scale and market maturity have reduced the need for costly subsidies and allowed Uber to sustain healthier take-rates. Additionally, its shared infrastructure spreads costs across its segments, while automation and scale have steadily lowered support, payment, and overhead costs. Together, these forces pushed Uber into profitability in 2023 and have continued to drive steady bottom-line improvement since.

At its Investor Update in early 2024, the company projected gross bookings to grow with a CAGR of mid to high teens, while improving its adjusted EBITDA (Uber's preferred measure of operating performance, which excludes items like stock-based compensation and legal charges) with a CAGR of high 30s to 40%. These gains were expected to drive free cash flow conversion of 90%. Halfway through that outlook, the company is right on track.

What makes Uber particularly distinctive is this ability to convert profitability into free cash flow, as the aforementioned goal hinted at. Few large-scale platforms generate cash as directly as Uber. The take-rate from gross bookings (from riders and eaters) is paid upfront, leaving the company with virtually no accounts receivable. And with an asset-light model, capital expenditure requirements are minimal compared to traditional transportation companies. This combination means adjusted EBITDA flows extremely efficiently into free cash flow, exceeding 100% conversion over the past year while growing by roughly 80%.

As told, Uber has reached an inflection point in terms of its profitability. Its global expansion is continuing on a wide scale, and while many of these new markets have not reached maturity, the company's scale offsets the drag as those regions move closer to the break-even point.

The transformation is striking: in less than a decade, Uber has gone from a company defined by breakneck growth and heavy losses to one that generates billions in free cash flow each year. The question now is how it chooses to deploy that cash.

“We do the right thing. Period.” Once a slogan of cultural reform, it now captures Uber's broader transformation. From Kalanick's fast-moving, cash-burning disruptor to a profitable company deploying billions in free cash flow. The fact that capital allocation is now a topic in its own right is a testament to how far the company has come.

When it comes to fulfilling our mission and building a generational company, profitability is a means and not merely an end.— Dara Khosrowshahi, CEO of Uber, Q2 2023 earnings call.

From the cash flow it generates, Uber's first priority is investing in future growth opportunities. These span both vertical and horizontal initiatives, such as entering new markets and cities, expanding Delivery into adjacent categories like groceries and retail, forging partnerships, and enhancing the company's technology and platform infrastructure. These priorities also extend into AVs, as discussed earlier. Uber's then-CFO, Prashanth Mahendra-Rajah, reflected on this and its broader investment approach in the Q2 2025 earnings call:

“And then lastly is obviously AVs today are not profitable. That has been a pretty consistent investment approach for Uber as we go into markets and go into products starting at a loss, we build scale, we build our experience. And then over time, we know exactly the levers that are necessary to turn to get that to profitability.”

Beyond growth investments, Uber is fully committed to returning capital to shareholders. Mahendra-Rajah continued:

“And I think from our standpoint, the good news is that, as you've seen with our cash flow and our capital allocation, we can afford to invest aggressively in the autonomous space and at the same time, to return plenty of capital to our shareholders. So it's not either/or.”

After reporting its first profitable full year in 2023, Uber authorized its initial buyback program in early 2024, beginning execution later that year. Like many tech companies, Uber has long relied on stock-based compensation, and while this was more dilutive in the early years, buybacks have begun to offset that dilution. Going forward, this is set to do much more.

In its Q2 2025 earnings release, Uber announced a new $20 billion buyback authorization, on top of the $7 billion approved in 2024, of which roughly $3 billion remains. This brings its total mandate to $23 billion over the coming years. As Mahendra-Rajah put it:

“That represents about 12% of our market cap and really is a reflection of how great we feel about the cash flow generation that's in front of us. So if you look at our history now, we've been allocating around 50% of our free cash flow to buybacks. I think that's a fair sort of way for you to think about how we will execute the capital return over the coming years. … So you should expect this to be sort of a multiyear plan. We will be active every quarter. But of course, we always reserve the opportunity that if there is a meaningful dislocation, we're going to get very opportunistic in the market.”

It's impossible to describe Uber's position without constantly returning to scale. Its dual marketplace completes tens of billions of trips each year, moving people and goods across more than 15,000 cities worldwide. But beneath the app, it's the algorithms, data, and shared infrastructure that turn local liquidity into a global advantage. Period.

)

)

)